EOFY 2026 Global 25 Model Portfolio

The Global 25 Stock Model finished midway between our US model and our non-US International Model. It returned 10.83%, against a benchmark return of 24.70%.

This is our last of four reports for the Australian FY2026 performance on:

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

It was a great year for the Australian portfolio, a so-so result for the USA, and a poor result for the International 20 and Global 25. The last was driven by underperforming selections across all sectors except resources, in which we had good wins.

The annual returns in USD were:

Portfolio: +10.83%

FTSE Global All Cap: +24.70%

Alpha: -13.87%

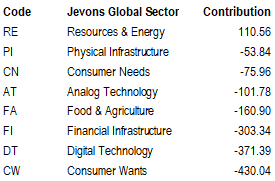

The sector report provides the cleanest read on what happened.

The only sector to show a positive contribution was resources. This explains the disparity in performance between the Australian and Global strategies.

We got the home story right in gold, battery minerals, and iron ore.

Everything else was not so great, and not down to one country.

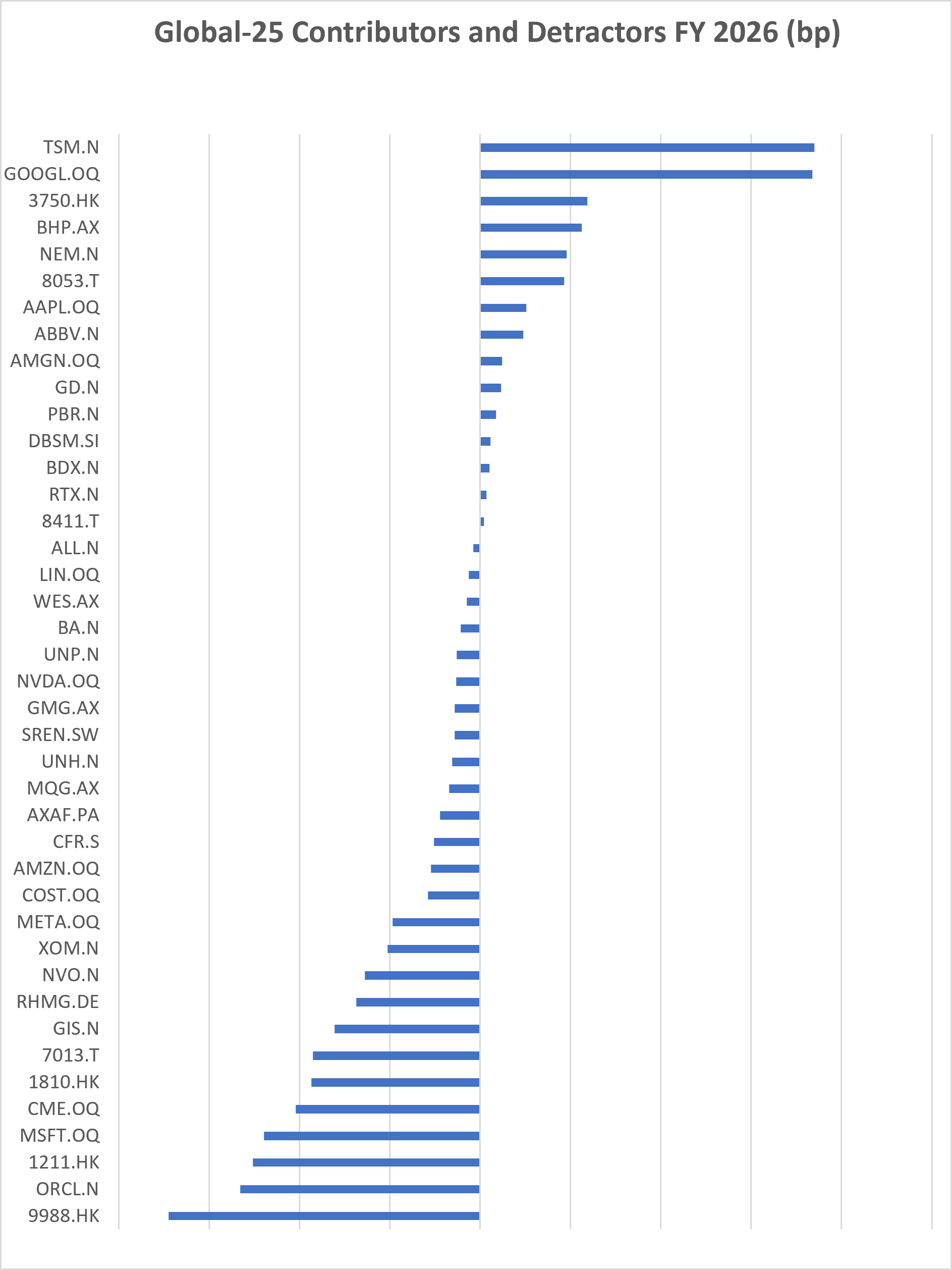

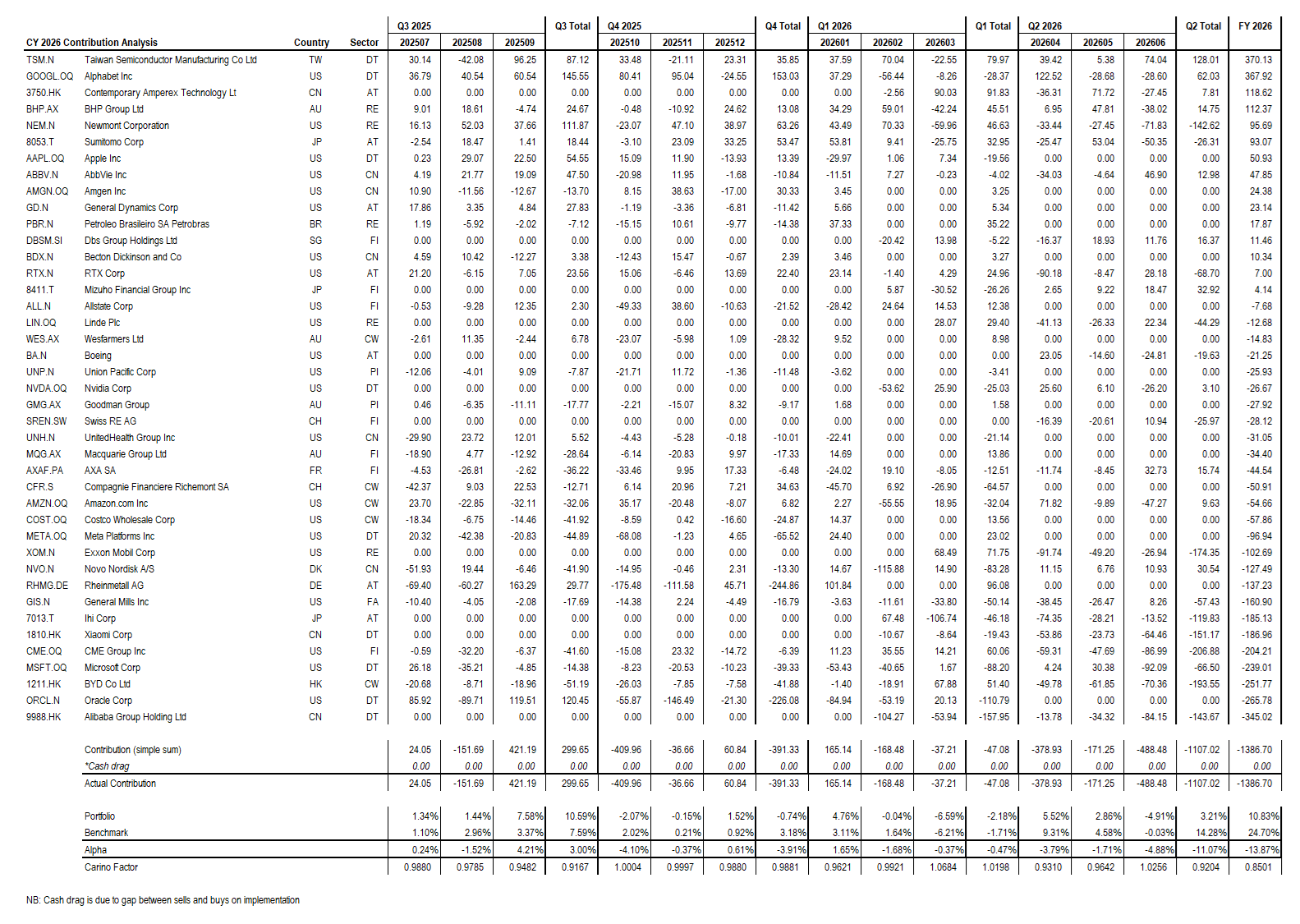

These were conditions where most of what we picked did not work. The detail of this negative skew for stock selection shows up clearly in the contribution analysis.

Portfolio diagnostics are important when deciding what to do, if anything. The above chart shows that we had very significant negative skew holding many sensible stocks. This matters a lot if the absolute return of the strategy is negative. In the year we just ruled off the return was +10.83%, which was a large -13.87% lag to benchmark.

The results of global managers are not out yet, but many will be bad, like us.

The markets were narrow.

South Korea, ARCA: EWY, was up around 170% thanks to High Bandwidth Memory (HBM) makers Hynix and Samsung. The USA version, Micron, XNAS: MU, was up around 800%, while Nvidia XNAS: NVDA, finished up a mere 25%.

When you have a very narrow market like this the performance will naturally divide between those on the hot trade, and those left behind everywhere else.

The important thing is that our absolute returns were positive.

Some areas of the portfolio, like China technology listed in Hong Kong, and the main technology stakes we hold in US hyperscalers, like Microsoft XNAS: MSFT, had a poor showing as investors sold those to chase performance in memory and storage.

You can see the full breakout of performance here.

Narrow markets can persist for some time, but we think this is a frothy market that will reward patience. The rational thing to do is to modestly play mean reversion.

In the changes this month, we trim some winners and upweight some value laggards.