EOFY 2026 US 20 Model Portfolio

It was an okay year in absolute terms, with the model up 20.26%, but lagging the S&P 500 at 22.05%. This was all down to the last quarter, where we lagged 9.49%.

This has been a year of exceptions to the rule.

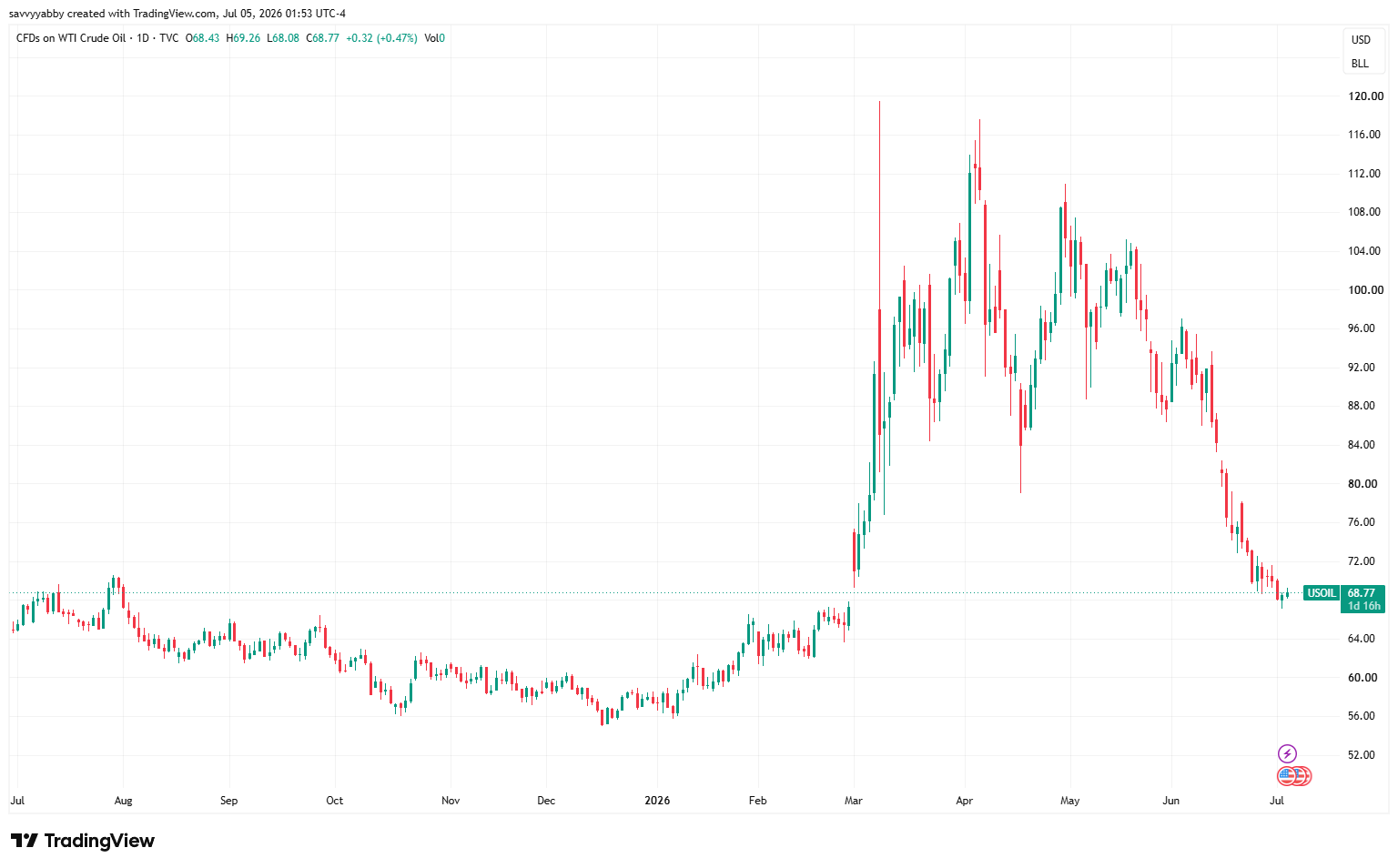

West Texas Intermediate WTI crude oil closed at $64.92 USD on 30-Jun-2025.

It closed at $70.02 USD on 30-Jun-2026.

This is after a one-billion-barrel draw on global inventory and strategic reserves.

The Israel-USA-Iran war is supposedly over except for the occasional airstrikes.

Gold was a more positive story.

It opened the account on 30-Jun-2025 at $3303.09 USD/oz.

It closed the year on 30-Jun-2026 at $4007.26 USD/oz.

Normally, we would toast such a result!

The return of gold, the barbarous relic was +21.32%.

Too bad the S&P 500 returned +22.05%.

Our twenty-stock best ideas US portfolio returned +20.26%.

I guess our best ideas were not good enough this year, and that is the simple truth.

Among the better ideas out there was High-Bandwidth Memory (HMB) chips, now in high demand in data center build outs, such as are made by Micron XNAS: MU.

I am no fan of hair shirts, but a minimum 3% allocation to Micron would have helped.

For those who have been around markets a while, this sh*t happens!

Hindsight will beat the market every single time. We have to move on and deal with the road that lies ahead of us. This is not made any easier by the suspicion that all is not right in the world of energy. Something about this oil price looks fake.

Two of the most cyclical industries on the planet look to have distorted pricing.

Memory chips are the most cyclical sub-industry in semiconductors.

Oil is the most cyclical of growth sensitive commodities.

For what it is worth, here is my “insight” such as it is.

High prices are generally cured by high prices, that is to say lower demand.

Low prices are generally cured by low prices, that is to say higher demand.

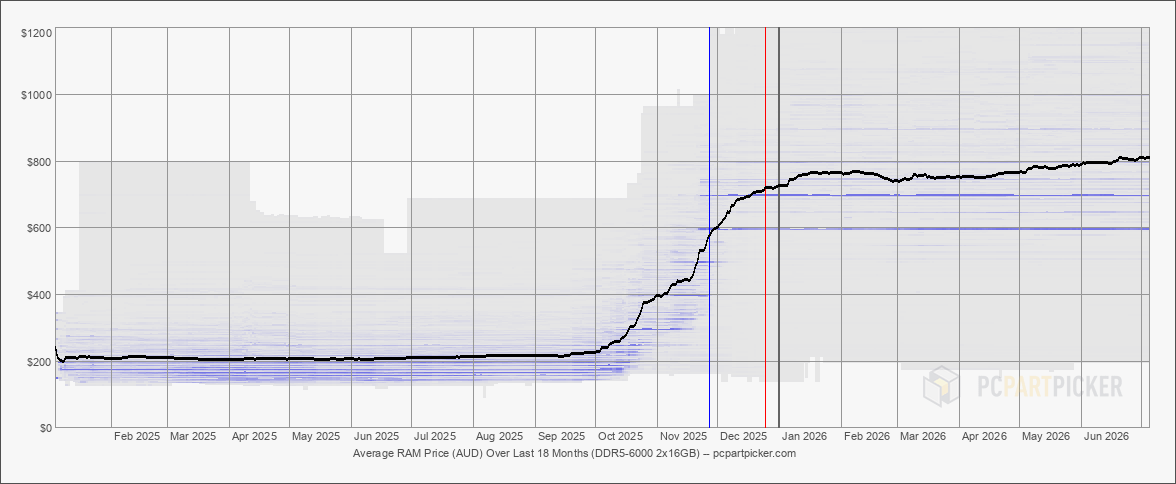

The boom in AI spend is real, but the memory price trends are worrying.

Local outfit Pc Part Picker has tracked a four-fold increase in the price of DDR5 6000 RAM (2 x 16GB) from a stable $200 AUD/module to $800 AUD/module.

The result will be price rises across the board in memory using consumer electronics.

Smart phones

Cameras

Laptops

Servers

Smart televisions

Electric vehicles

The frenzy of artificial intelligence spending is leading to an inflationary spike.

The flip side of this is that some stocks we hold and like are really hurting.

The obvious solution to this problem is to buy memory makers.

This is not a terrible idea when price targets on stocks like Micron are raised to $2000.

For those who are happy to trade this wild market let us pray with Saint Augustine:

Give me chastity and continence, but not yet! - Saint Augustine

I emphasize the word trade, since you should rightly run a wide trailing stop about 20% lower than the current price to salvage any profit when it cracks.

That is easy advice to give and almost impossible advice to carry out.

Failing any saintly hotline to a higher authority, we will stick to the brief for this model portfolio and try and patience our way through this hot mess of wildness.

Afore doing that, here is the year in review.

FY2026 in Review

If you happen to live outside Australia, you have a different financial year. Last night I went and sank a few mulled wines at the Canberra Christmas in July, with a chaser of Berlin Banger - The Foot Long Kransky Chilli Dog. We are weird here. Get used to it!

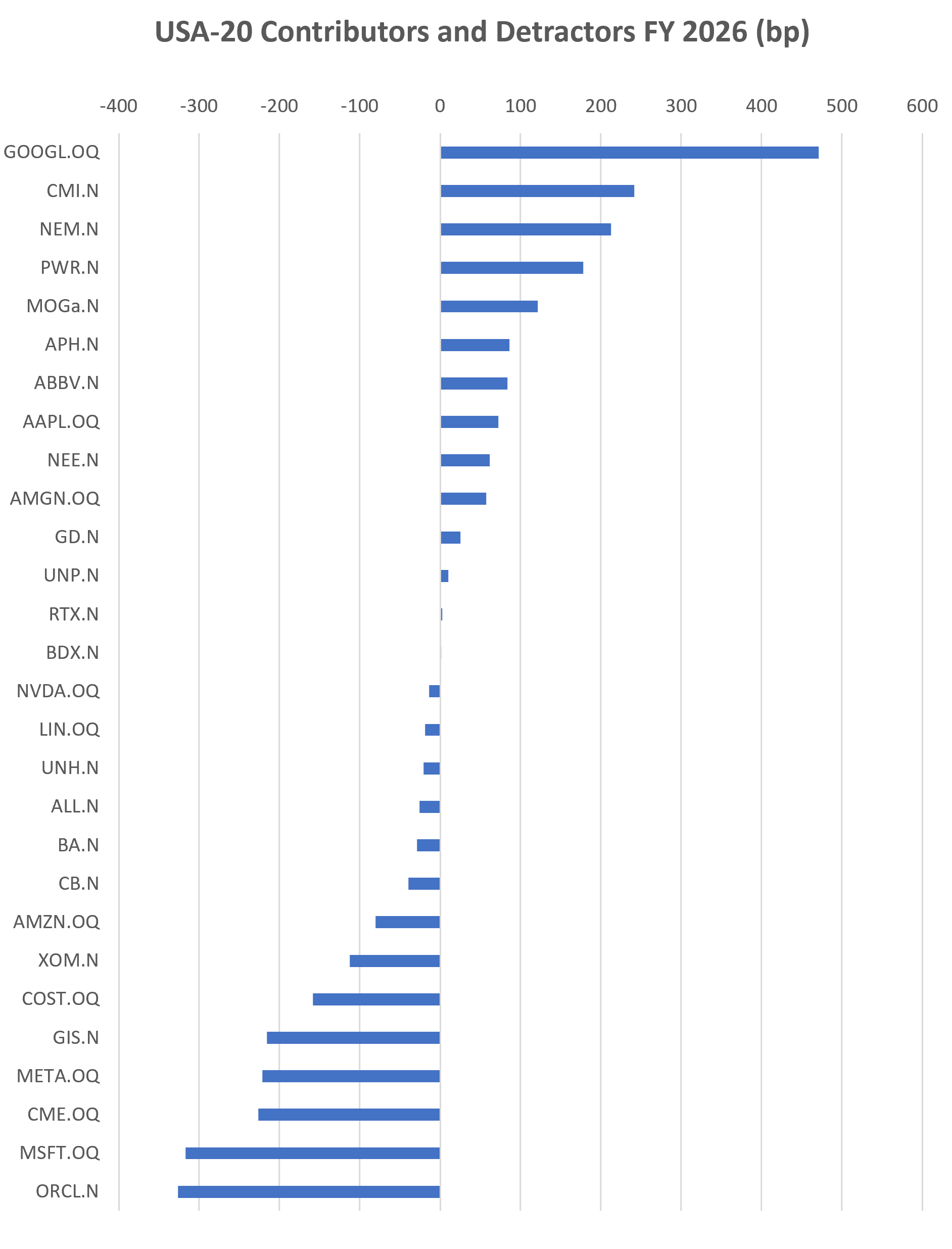

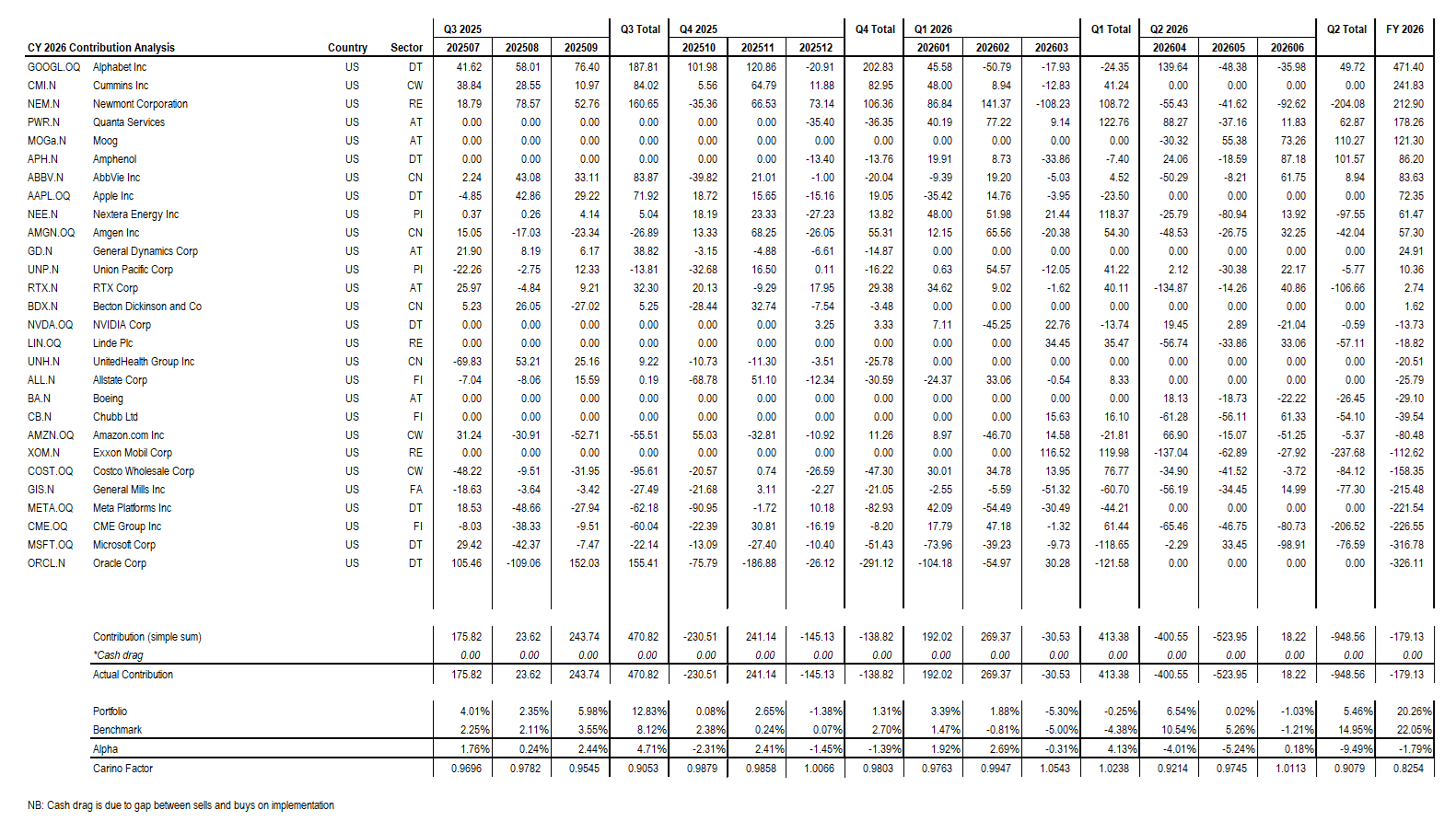

Here is the annual roster of offenders and defenders.

I am flippant here, because this is a wash. You can see that there is no real skew either way. This was a middle of the road, track the benchmark year. Not good. Not bad.

Apologies for the tiny image, but it is the whole year compressed into one snapshot.

The best way to understand the story of last year is to look at quarterly alpha:

Q3 2025: +4.71%

Q4 2025: -1.39%

Q1 2026: +4.13%

Q2 2026: -9.49%

Notice that the relative return was really bad in the last quarter.

For completeness, the numbers were:

Q2 2026 Portfolio: +5.46%

Q2 2026 S&P 500: +14.95%

That last comparison is crucial for what we do or do not do next.

In a quarter where we lagged by 9.49%, we were actually up 5.46%, which is a better than 20% annualized rate of return. However, the market was up 14.95%, which is an annualized rate of return of +74.6% per annum! That is what happened.

Can this go on?

With the level of enthusiasm for all things artificial, including oil prices, yes, it can.

For how long, we cannot be sure, certainly another quarter or so.

During the late 1990s technology boom, I recall averaging portfolio rates of return of around 75% per annum over three straight years, until it stopped, and I didn’t.

The markets then dropped about 80%, and I got back to where I started.

This is what happens in an investment mania.

Personally, I do not think we are in full manic mode yet, so I expect more frantic chasing after whatever moves up and to the right.

The other lesson from the contribution analysis is to note that hyperscale stocks like Amazon XNAS: AMZN, Meta XNAS: META and Microsoft XNAS: MSFT undershot.

A boring railroad like Union Pacific XNYS: UNP did better than that bunch.

Notice also that, while Alphabet XNAS: GOOGL was our top contributor, we had a very good showing from diesel engine maker Cummins XNYSE: CMI and mega-cap gold miner Newmont Corporation XNYS: NEM. The last in spite of the retreat in gold.

Did we make mistakes last year?

You bet, the two I would single out was our exit of Apple XNAS: AAPL, and the brief dalliance with Oracle XNAS: ORCL where we timed everything badly.

You can surely find others.

We held no Micron.

Onwards to a minor rebalance.