Model Performance Updates Apr-2026

The markets continue to swing wildly for the on-again-off-again Gulf War Infinity.

This month our performance updates will be brief, as no new changes are planned to any of the model strategies. Our last rebalance was effective 31-Mar-2026 across all strategies. We reprise that update here, to keep folks informed, and give month to date performance for all four strategies.

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

This omnibus report aims to be more succinct.

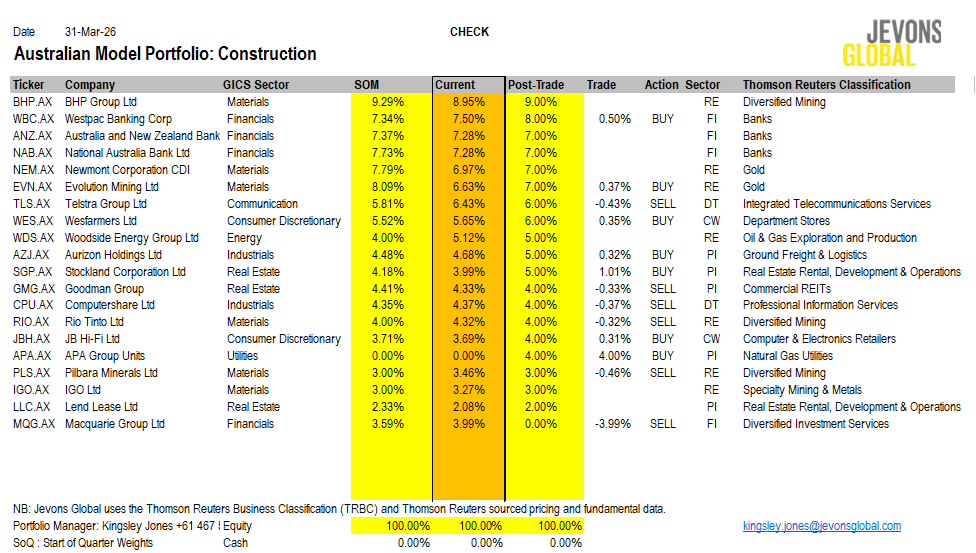

Australian 20 Stock Model Portfolio

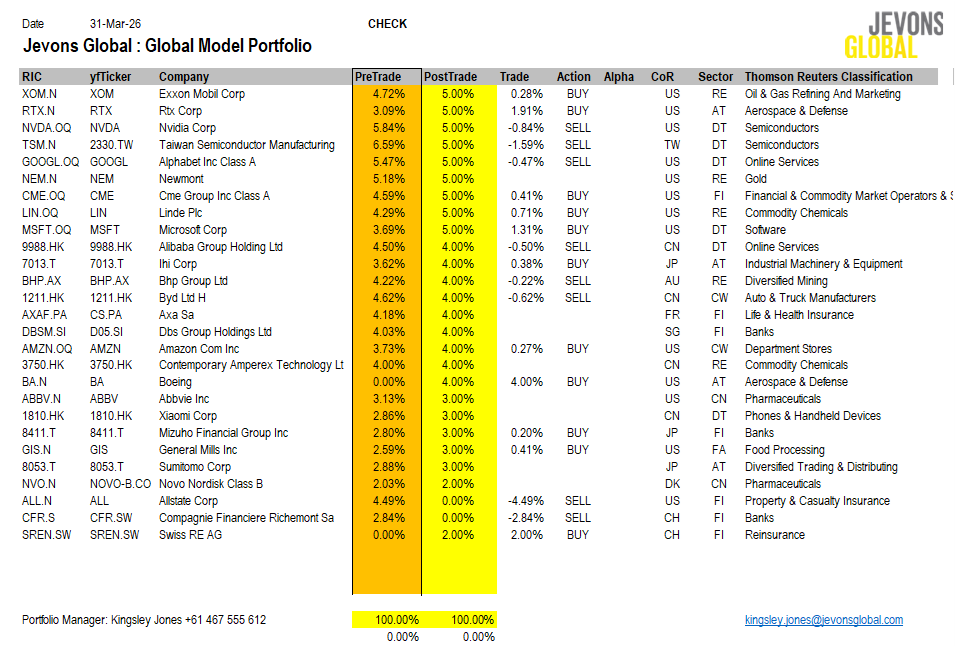

The last rebalance involved an exit in Macquarie Group XASX: MQG and an addition of the gas pipeline company APA Group XASX: APA. There were other minor adjustments to stock weights to adjust them up and down to round numbers for quarter end.

No further changes are contemplated at this stage. The markets are too volatile for any high conviction moves other than the increased weight to energy stocks via the addition of Woodside Energy XASX: WDS, on 3-Mar-2026, and APA Group.

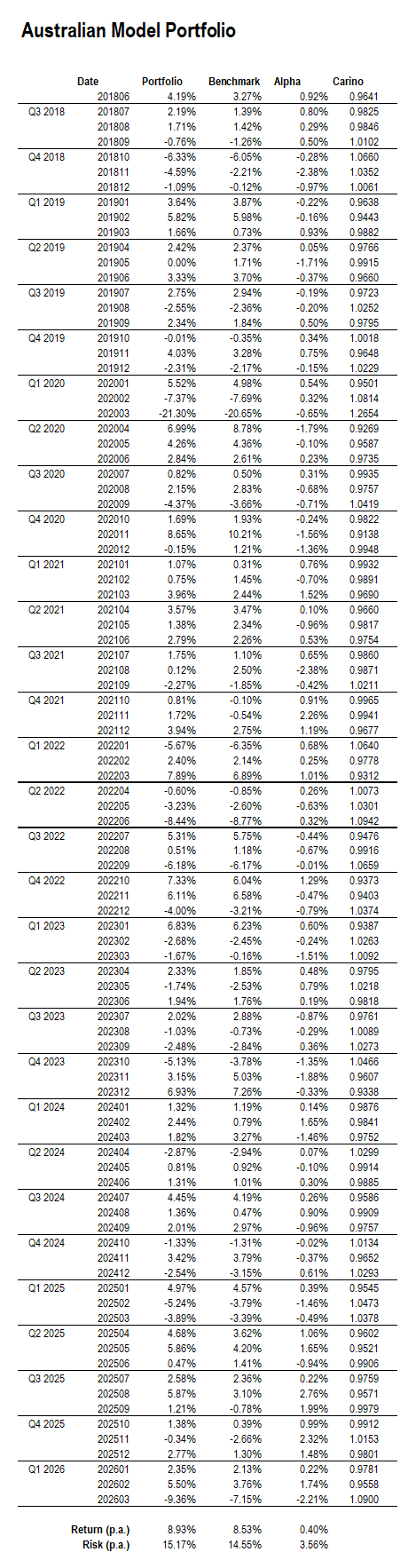

The first quarter to 31-Mar-2026 was negative, due to a large drawdown in March, for both the model portfolio and the benchmark S&P/ASX 200. The Q1 numbers saw our model down -2.13% and the market -1.61% for a net lag of -0.52%. This is down to a string open to the year, followed by a pullback in March.

The month of March was ugly, due to the uncertainty created by the war on Iran and the high exposure Australia has to rising diesel fuel costs. This nation, with its long distances between cities, and fuel intensive mining and agriculture is at risk.

The US markets have been more sanguine, due to the perceived self-sufficiency of that economy on domestic crude oil and natural gas supplies.

The jury remains out on whether it will stay that way, because US diesel prices are rising, as are gasoline, and US sourced West Texas Intermediate.

On a month to date basis, the Australian portfolio rebounded 2.40% to the market close 24-Apr-2026, lagging 1.20% behind the S&P/ASX 200, which was up 3.60%.

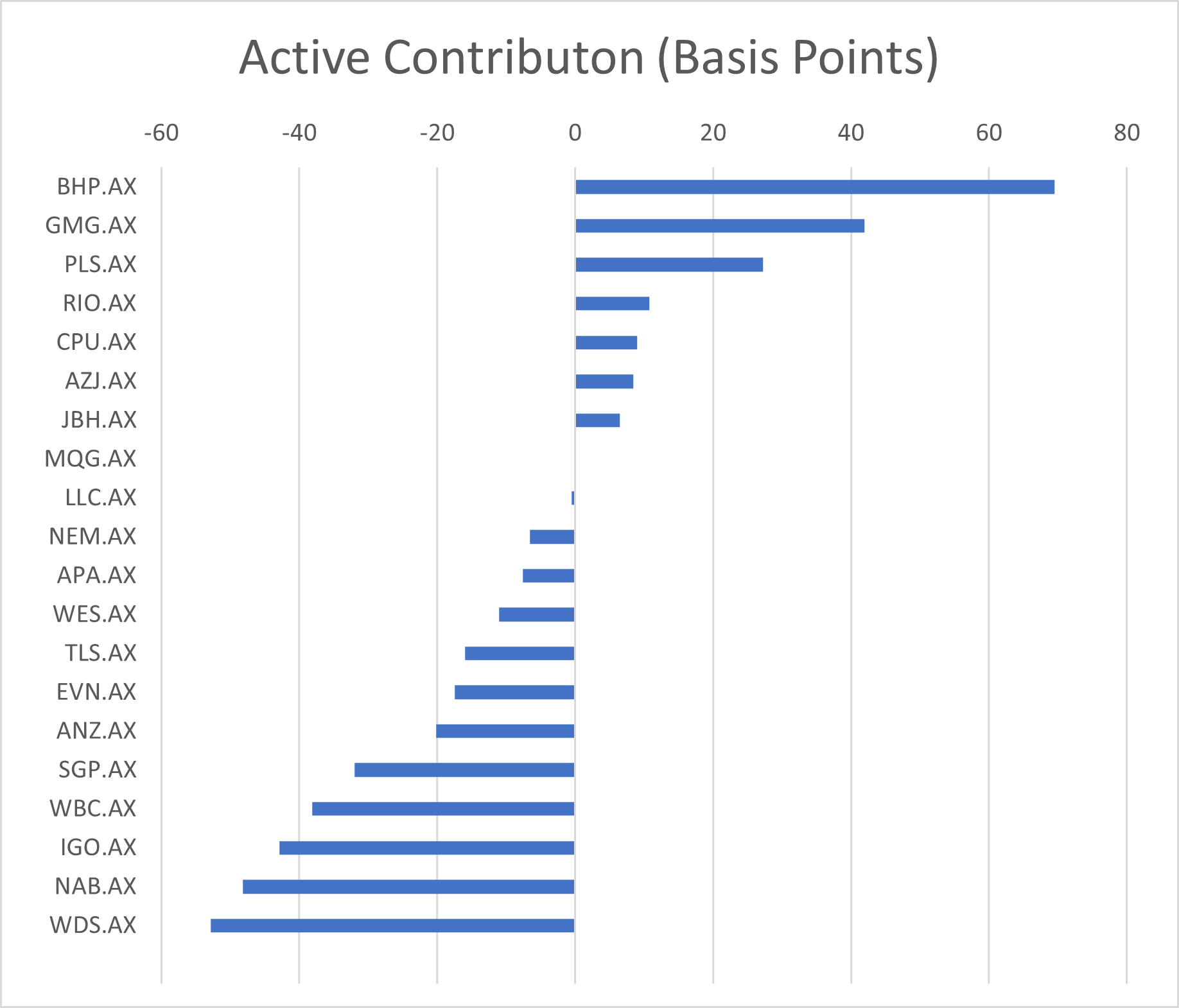

The fiscal year is still very positive, with our model up 11.70% since 30-Jun-2025, while the S&P/ASX 200 is only up 1.98%, for a lead of 9.72%. Not as great as before, but the model portfolio is still doing well. The bets we have on commodities are balanced to bulk miners like BHP and RIO, energy via Woodside and APA, gold via NEM and EVN, and lithium via PLS and IGO. Presently, we are underweight Australian technology, which has rebounded somewhat from a deep correction over the past year.

In summary, there is no compelling reason to adjust the portfolio as we see tightness ahead in both monetary conditions and commodity prices. The status of the cycle in China will determine if we lighten exposures in the industrial metals market.

While gold has not performed as most people expected in this wartime environment, we remain constructive on holding these stocks in Australian portfolios. Traditionally, the USD tends to strengthen on weakening global conditions. The Australian dollar remains firm, for now, due to the expectation of higher interest rates. However, we think the Australian economy will struggle with the cost-of-living pressures.

Locally, the Australian banks are expensive, especially the Commonwealth Bank, and there are signs of weakness in retail. Our tilt to yield plays, inflation hedged utilities, like rail haulage in Aurizon, and gas transport in APA Group, plus commodities, is a bet on tricky times ahead for mainstream Australian businesses.

Let us see what the Federal Budget brings, and whether the Iran war is brought to a timely close or metastasizes into a global stagflationary supply shock.

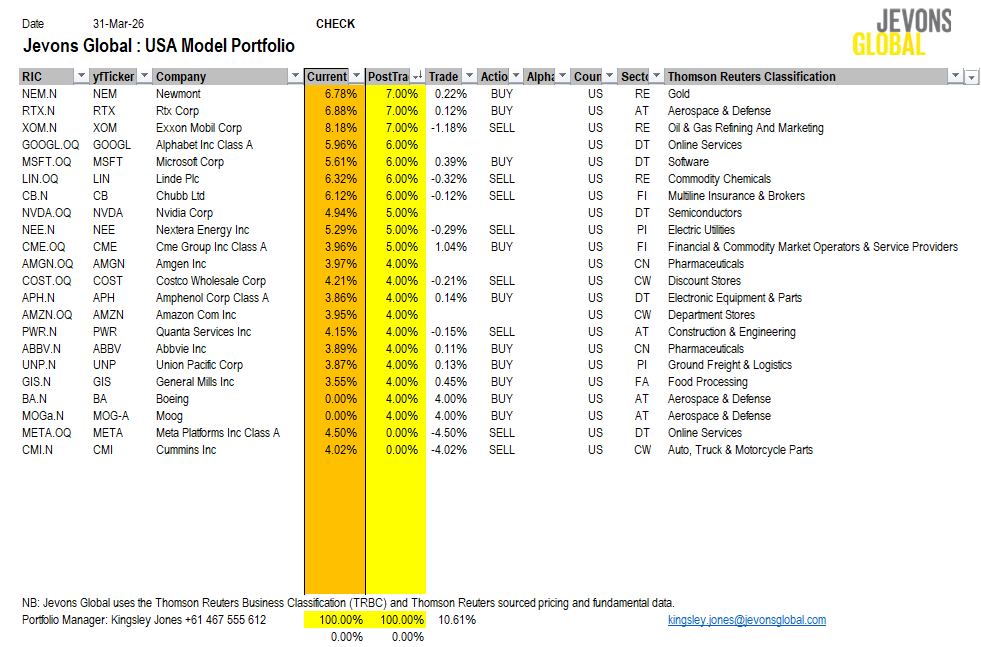

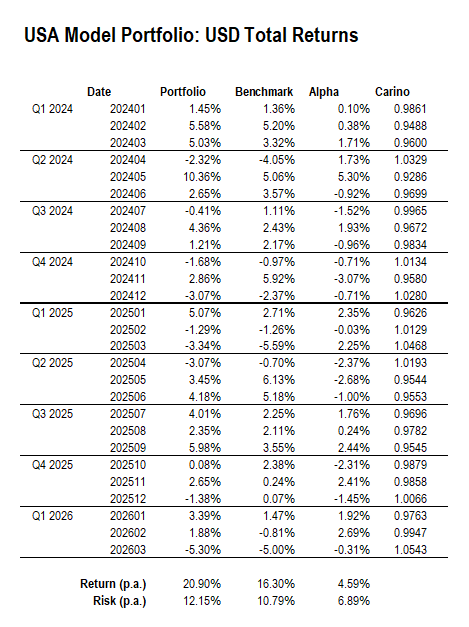

USA 20 Stock Model Portfolio

The 31-Mar-2026 rebalance saw us exit positions in Meta Platforms XNAS: META and Cummins XNYS: CMI, to add Boeing XNYS: BA, and Moog XNYS: MOG.A. The capital expenditure boom in the USA is likely to widen into defense aerospace, due to the planned 50% increase in the Pentagon forward budget for 2027.

There are already high levels of capital expenditure on the data center build for AI, but we think this is largely priced by the market. Moreover, much of the electrical, chips, and cooling systems are sourced overseas. The trade is real but seems crowded.

The defense focus of the Trump Administration has been made clear by the war on Iran, and initiatives like the Golden Dome missile defense, and Golden Fleet.

We already own a position in Raytheon Technologies XNYS: RTX, which has a key role in naval defense missile systems and antiballistic missiles. However, we see a possible multi-year turnaround underway at Boeing XNYS: BA, off the back of their platforms for military transport, airborne refueling, and early-warning radar aircraft.

Boeing has struggled for years with the aftermath of the 737-MAX debacle, which was a failed design exercise in cutting corners to meet civilian aerospace demand.

The cheque book now seems open for new design work, like the F-47 Next Generation Air Dominance (NGAD) fighter, plus the renewal of the US manned space program.

Space-X is coming to market, via IPO, and we see renewed interest in space.

One little known area of aerospace that is also set to benefit is motion control. This is the field of electromechanical and hydraulic actuators to control motion in flight.

The field has good margins, from technical knowhow, and the high degree of trust that manufacturers place in the performance of these vital subsystems.

Here we added Moog XNYS: MOG.A, the premier US firm in this area.

The name Moog may sound familiar; the company was founded by the brother of the inventor of the Moog synthesizer, the one that shaped electronic music in the 1970s.

Invention runs in the family!

The model performance to 31-Mar-2026 was down. The market fell -5.00%, with the portfolio down -5.31%, for a net lag of -0.31%. This has been followed by a rebound of 10% for the S&P 500 through to 27-Apr-2026. This was concentrated in the large capitalization technology companies. We hold these at 21% below the market 45.5%. Consequently, we were up a lesser 5.34%, squaring the prior month fall, but a huge -4.66% behind the market. This highlights the large risk investors are running now being so concentrated in the single theme of AI. This is why we are diversified.

Note that the largest negative contributors MTD have been Exxon XNYS: XOM and the defense contractor Raytheon XNYS: RTX. Wall Street has taken the view that this war in the Persian Gulf will soon be over, there will be no lasting consequences, and we can return to putting all of our capital into the AI basket. Perhaps. Perhaps not.

Trading single month volatility is mug’s game, we will wait this one out.

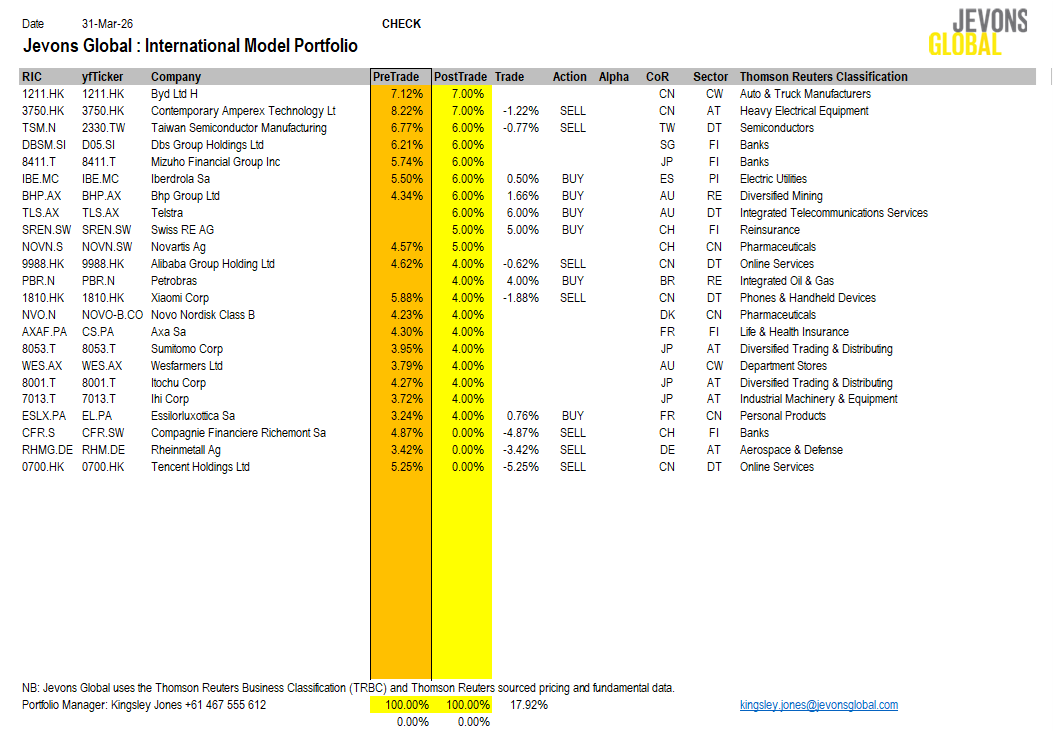

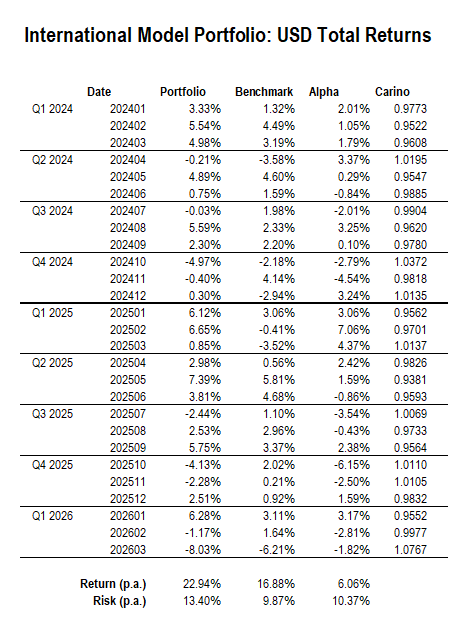

International (non-USA) 20 Stock Model Portfolio

The major changes at 31-Mar-2026 were to exit German defense play Rheinmetall AG XETR: RHMG, Swiss luxury goods firm Richemont XSWX: CFR, and Hong Kong gaming firm Tencent XHKG: 0700. These were replaced by Telstra XASX: TLS, Brazilian oil firm Petrobras XNYS: PBR, and Swiss reinsurance firm Swiss Re XSWX: SREN.

Rheinmetall had performed very well for us since inception, but we have tilted to US and Japanese defense exposures as the German story is fully priced. The other moves are to shore up some yield in strong currencies, like the Swiss Franc, and to fill out an energy tilt in the international model via Petrobras. We already have exposure to the offsetting Electric Vehicle thematic via BYD XHKG: 1211.HK and CATL XKHG: 3750.HK, plus Xiaomi XKHG: 1810.HK. The war on Iran has lifted all boats in alternative energy but also benefits those oil and gas producers outside of the Persian Gulf. Telstra is a likely beneficiary of the multi-year trend for AI-related telco services.

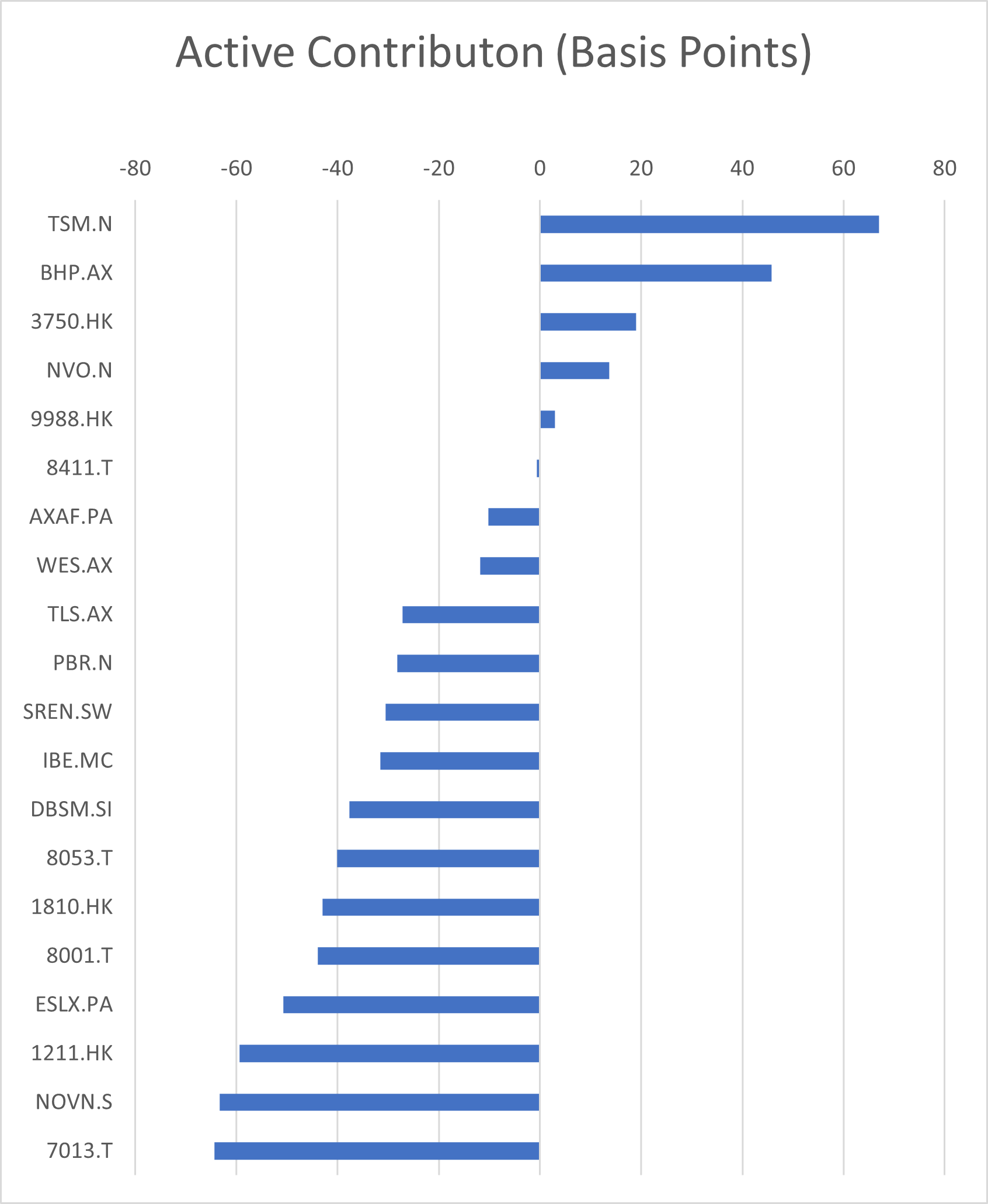

The return in March was -8.03%, behind the FTSE Global All Cap Index at -6.21%, for a lag of -1.82%. Note that the benchmark includes US stocks, which we did not own.

The rebound MTD was modest at +4.74%, behind the FTSE benchmark at +8.68%, for a negative lag of -3.94%. The key driver of this was US technology stocks which we do not own in this non-USA focused strategy. Note that the top performer was Taiwan Semiconductor XNYS: TSM, our second-largest position after CATL XHKG: 3750.HK.

These moves are related to the singular focus of Wall Street on US technology.

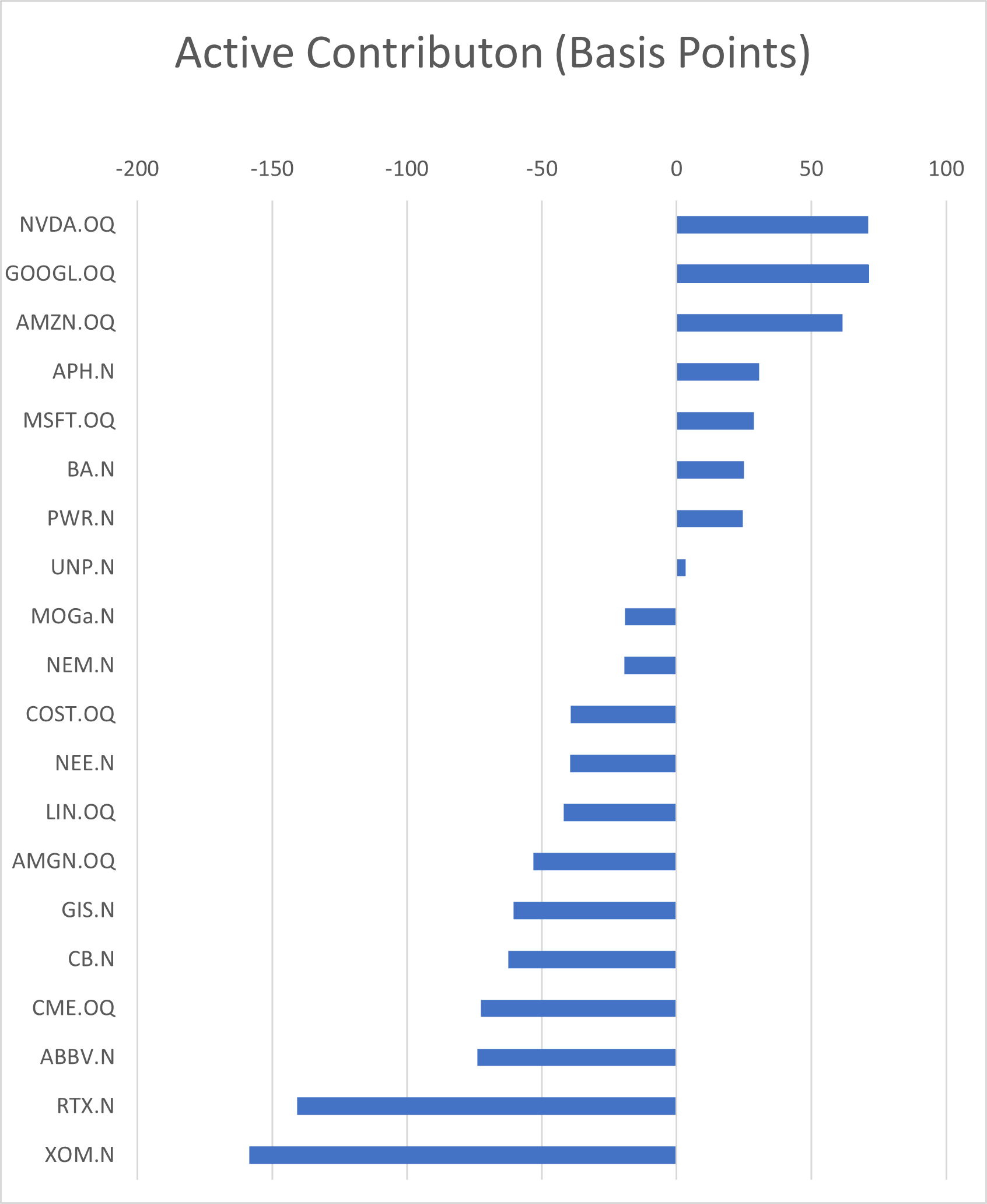

Global Best Ideas 25 Stock Model Portfolio

The Global model is supposed to be our top 25 ideas drawn from the US and non-US models. The changes last month just squared up the holdings for new additions. The global model already holds Exxon, so we did not add Petrobras. However, we added new US position Boeing XNYS: BA, and Swiss firm Swiss Re XSWX: SREN. To make room we exited US insurer Allstate XNYS: ALL and Richemont XSWX: CFR.

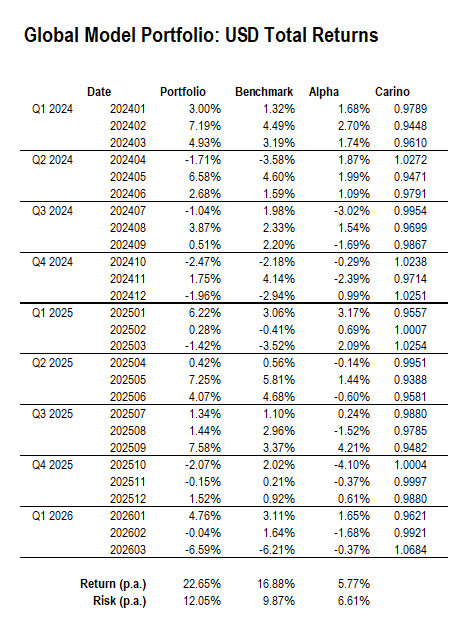

The performance in Mar-2026 mirrored that of the international model. We were down -6.59%, a modest -0.37% behind the FTSE benchmark at -6.21%.

The MTD performance was +6.42%, versus the FTSE at +8.68%, for a lag of -2.25%. The drivers of this result are again the US technology rally off the March lows.

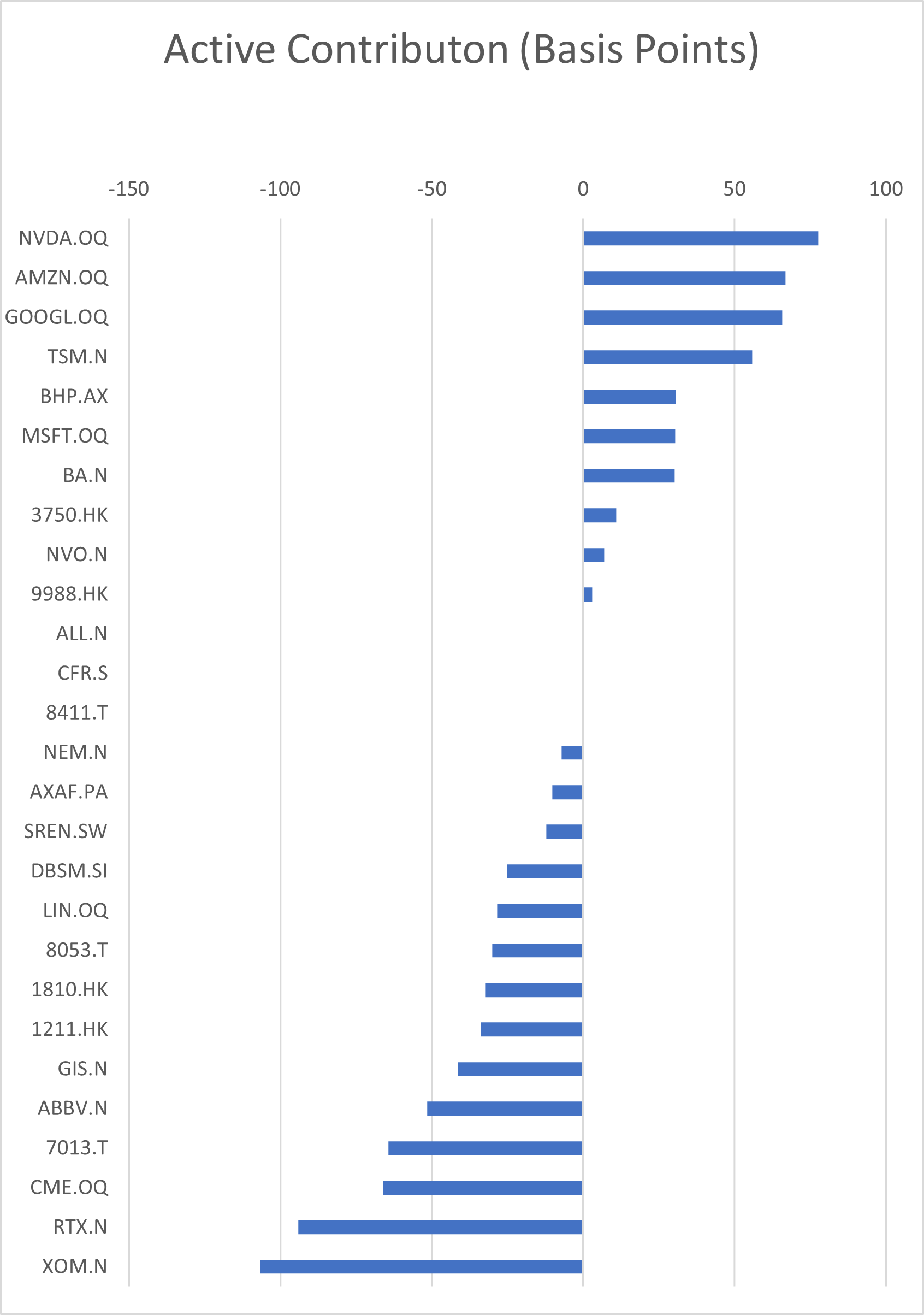

The above contribution chart highlights the swing back to technology names, with the results led by Nvidia XNAS: NVDA, Amazon XNAS: AMZN, Alphabet XNAS: GOOG and Taiwan Semiconductor XNYS: TSM. The key laggards were our geopolitical hedges in Exxon XNYS: XOM and Raytheon XNYS: RTX, along with CME XNYS: CME.

In my view, those risks remain.

There are no changes planned this month, but we may choose to take some profits in the technology names that ran and top up the laggards. This market is treating the war lightly and clearly wants to “return to the prior trend” consensus.

With inventories of oil, gas, refined fuels, petrochemicals, fertilizer, industrial gases, and other vital industrial commodities being drawn down, we do not see a rapid return to normalcy. Worse, the higher cost environment may see a scaling back in planned capital expenditures, outside of defense and energy needs.

Conclusion

These remain turbulent market conditions, and we are unpersuaded that the coast is clear to an imminent end to the Iran war, and attendant geopolitical tension.

Rhetoric from the White House remains detached from reality.

There has been no visible regime change in Iran, apart from a natural hardening of the national resolve in the face of US and Israeli attacks. Strategic bombing campaigns do not end wars, and we do not expect this circumstance to be any different.

Presently, the global model has 54% in US stocks, rather than the benchmark 62% and is underweight global technology by about 10%, and overweight resources by 14%.

Time will tell if this positioning will be rewarded.

Our logic is that present conditions resemble those of the 1973-1974 bear market, the proximate cause for that was the Jan-1973 Arab Oil Embargo of the USA.

This time is different in two ways: the USA and Israel started this war, and so could choose to stop it; and the USA is a net producer of oil and gas.

Superficially, the USA looks invulnerable to major economic damage.

However, wars are costly to finance, and this one is likely to damage the world and thereby cause a blow-back into US multinational profits and confidence.

Due to the valuation disparity between US and non-US markets, we do not see the US market as a durable safe haven for capital. Indeed, the level of animosity displayed towards foreign actors could see conditions ripen for capital flight.

We are not there yet, but I do not see present conditions as stable.

Granted, we have already seen instability, and relative underperformance these past eight weeks from our non-US and non-technology holdings. However, what has propelled that difference is capital-expenditure related growth expectations.

Capital expenditure booms usually die of old age meeting higher costs.

There remains enormous enthusiasm for the AI-related capital expenditure boom, especially in the USA, but the rise in construction-related costs due to diesel and material prices, plus manufacturing interruptions to supply chains, could soon be upon us. There is also the prospect of higher interest rates.

The US economy has run fiscal deficits >5% for some years now.

We have a planned 50% budget increase for the Pentagon, an active war in the Middle East of uncertain aims and duration, and a deteriorating geopolitical environment.

Guns and Butter sank the administration of President Lyndon Baines Johnson.

The US adjustment from the excesses of the late 1960s gave us the 1970s.

Students of market history will note that the Nifty Fifty stock boom of the 1960s fully died in the 1973-1974 Bear Market. It took decades for some names to recover.

This all happened at a time of continued innovation.

While the US Space Program stalled in the mid-1970s, the consumer markets were very active, and the shift to greater fuel economy helped foreign firms.

There are undoubted reasons to keep betting on US innovation, but we think that the present focus of US technology investors is too crowded in those spending money.

We are not fools, and believe that you must spend some money to make money.

However, the set-up today means that young innovators are literally given brand new tools for reshaping entire industries for free. Intelligence is not a new thing, and the belief that this can be controlled through mechanisms of ownership seems naive.

The US mega-tech firms have splendid advantages, but they also seem blinded by the market power they wield. This was built on network effects to aggregate attention.

However, the growth of replicable Large Language Models (LLM) via open source and shortcuts like model distillation could leave the technology majors looking like very expensive telecommunications firms who have put all their cash into infrastructure.

The truth of software economics has not left us. The marginal cost to replicate any software is close to zero, in media terms, but was formerly high in barriers to entry.

Since the process of generating software is now automated, we foresee a widening of opportunity for disruptors to reshape all software dependent process industries.

This does not seem to be a stable environment for massive capital expenditure.

The problem is who will capture the return on AI investment.

I am a believer in the powers of human creativity, which I now see amplified.

The major technology firms have great present businesses, but the future of any and all business now looks uncertain to me. In that world prospect, I prefer to reallocate capital towards the fruits of nature, via commodities, and infrastructure which is unlikely to be disrupted, such as gas pipelines and railroads.

The virtual world seems set for cataclysmic change.

In consequence, I am looking for investment opportunity in the physical world.

It is too early to say, for certain, that these instincts are correct.

We are baby stepping in those directions we think are likely to prove more rewarding over time, and perhaps less exposed to a collapse in sentiment.

These are both disturbing times and exciting times.

1984 came and went…

It was not as bad as the book made out.

I am looking forward to finding new opportunity.

Take care and happy investing!