Practical Superintelligence

Consensus is forming that the Artificial Intelligence boom is now morphing into a bubble. The strategy for bubble investing is different. In this case, follow the money in capex.

There is an emerging consensus that the Artificial Intelligence boom is morphing into a bubble. In this stack, we ask: What kind of bubble? and: How durable the result?

The Savvy Yabby Report is pleased to announce the return of our mascot.

Our data source was replaced mid-year because it had proven too expensive.

The one-button-press operation of our sentiment indicator took a while to rebuild on a new data source due to its dependence on the availability of shares outstanding.

It may surprise some readers to know this, but the historical market capitalization of any listed security is not a common data item. You can create it, but it takes work.

Enough of that, as we are back now.

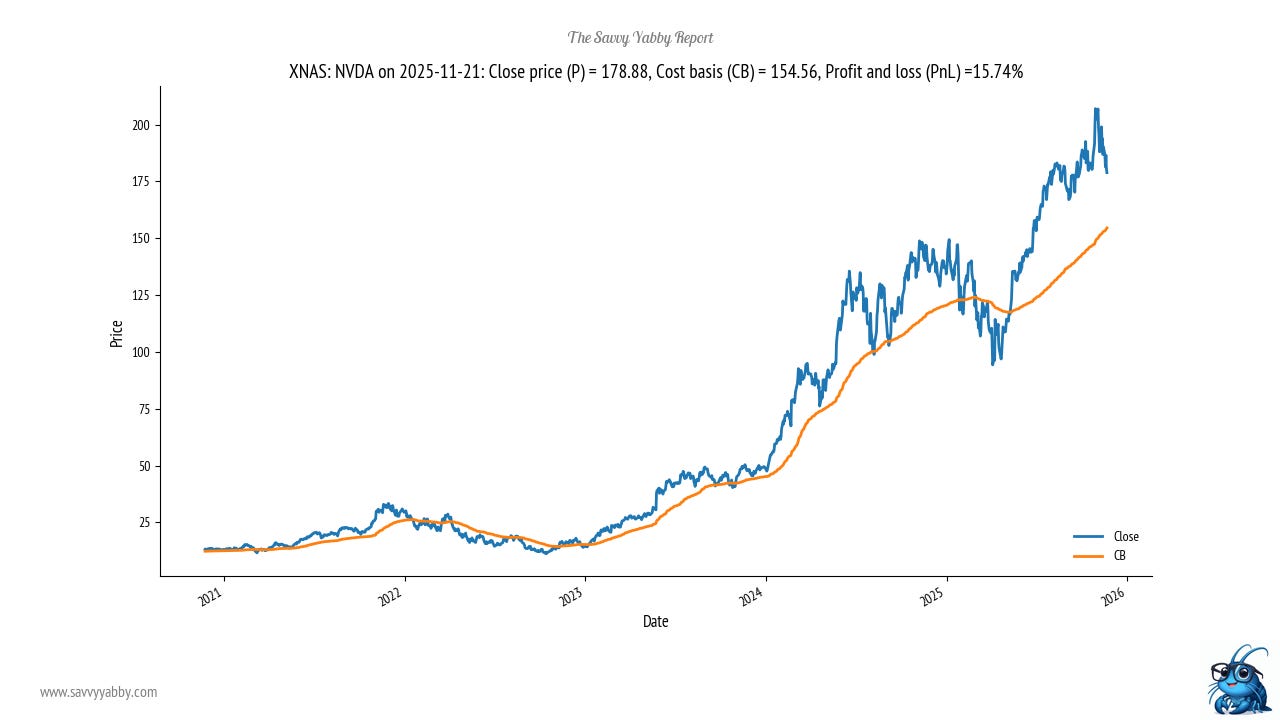

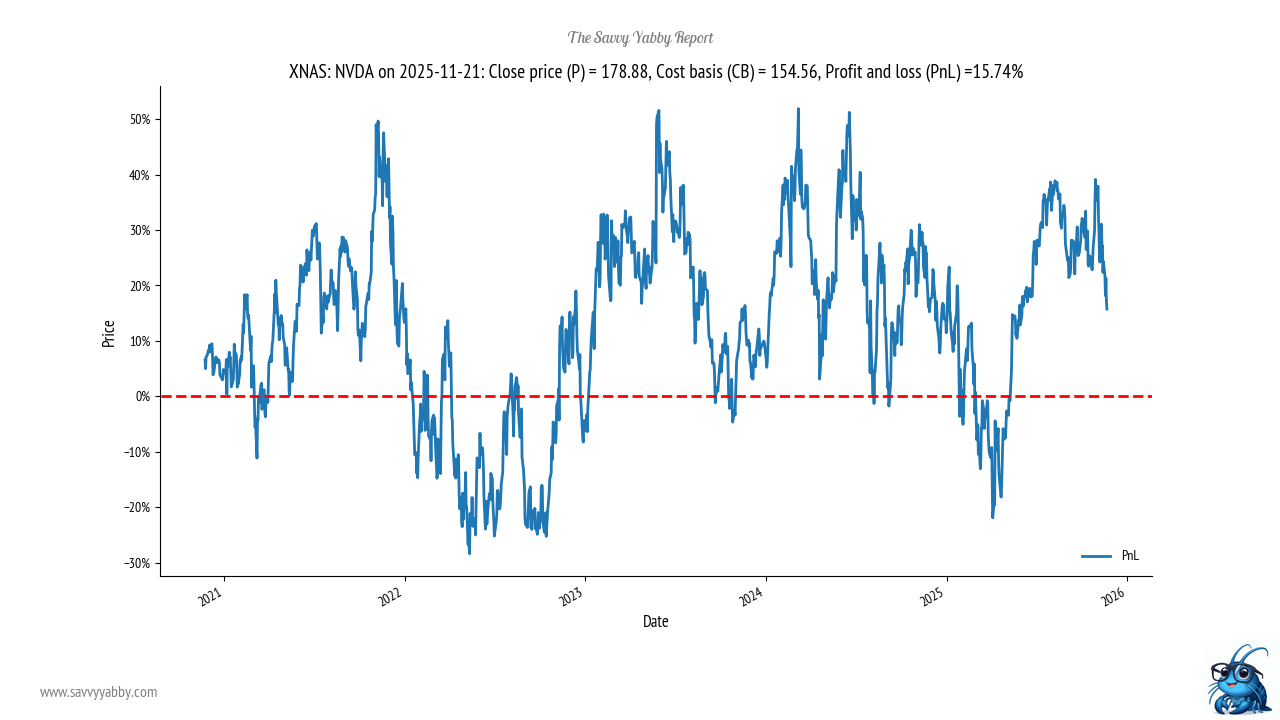

Investor Sentiment in NVIDIA

I start with this observation about investor sentiment in the flagship stock of the current boom in hyperscale expenditures on chips for the AI boom.

The history of the unrealized profit and loss of investors shows nothing unusual about this time. There is not any blowoff peak positive sentiment that would make one view the current positioning as shaky. It looks like a healthy correction.

Nvidia just reported impressive quarterly results that saw an acceleration in the rate of revenue growth of the prior quarter. The actual spend on chips is growing faster.

The year-over-year revenue growth rates of a hardware business will fluctuate due to changing patterns of demand, and the timing of new product releases.

However, the latest Q3’25 result was incredibly strong for a firm of this size. The print was 57.01B of quarterly revenue for the latest result, compared with 35.08B for the one-year prior quarter of Q3’24. Sequentially, the revenue growth was strong.

The largest company in the world, by market capitalization, is still growing revenues at a rate of 60% per annum and holding net profit margins north of 50%.

It is true that trees cannot grow to the sky, but this remains a pretty special story.

With a Price to Earnings (PER) ratio of 44.7x trailing this is not expensive.

The correction should be bought at these levels.

It isn’t over yet, so we need to dig into what will kill the trend.

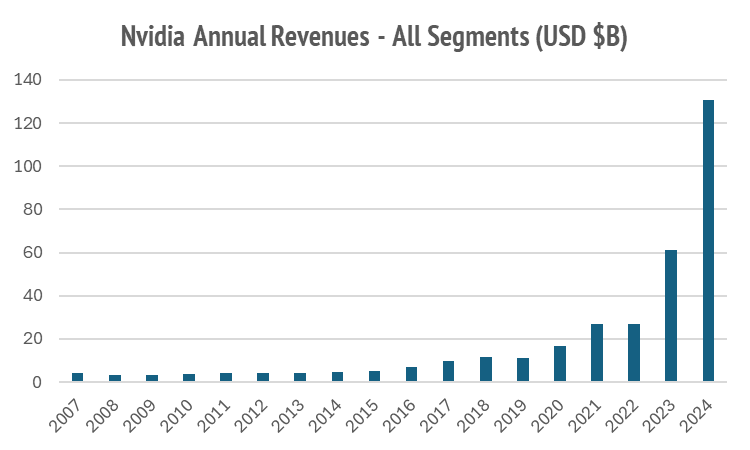

The Changing face of Computing

What produces corrections like we see now is the rational fear of heights.

It is very easy to see why when you look at the annual revenue chart for Nvidia.

What is important to understand about this change is the subtle shift of emphasis in the purpose to which Nvidia chips are applied. For many years, it was known as the premier computer graphics company for applications like computer gaming.

A top line graphics processor from Nvidia for gaming now costs $6,163 AUD when bought online at JB HiFi. I recall a time when an expensive card cost $500 AUD.

")

These cards are no slouches in computing. The TechPowerup specification for an Nvidia GeForce RTX 5090 comes in at 92.2B transistors for 1.637 TFLOPS.

The launch price for that product on 30-Jan-2025 was 1,999 USD.

For comparison, using the same website, an NVIDIA GeForce RTX 3090, which was the top of line offering five years ago, had 28.3B transistors for 556 GFLOPS, and came to market at a price point of 1,499 USD, on 24-Sep-2020.

The story of progress over those two examples looks like this.

This is a version of Moore’s Law at work.

Eventually, the rate of performance improvement will slow down, and hit a cost wall, a power and energy wall, or both. Perhaps we are closer to the end now.

It is a huge ask for gamers to spend $6,000 on a graphics card!

However, the Nvidia business started changing around five years ago.

There are many landmark events in the growth of Artificial Intelligence stretching back into the very early history of computing. However, the advent of Deep Learning marks the modern wave of innovation, which has greatly expanded the application.

You can think of the transformation in the business of Nvidia as a consequence of the wide applicability of Graphics Processing Units (GPU) to neural network computation.

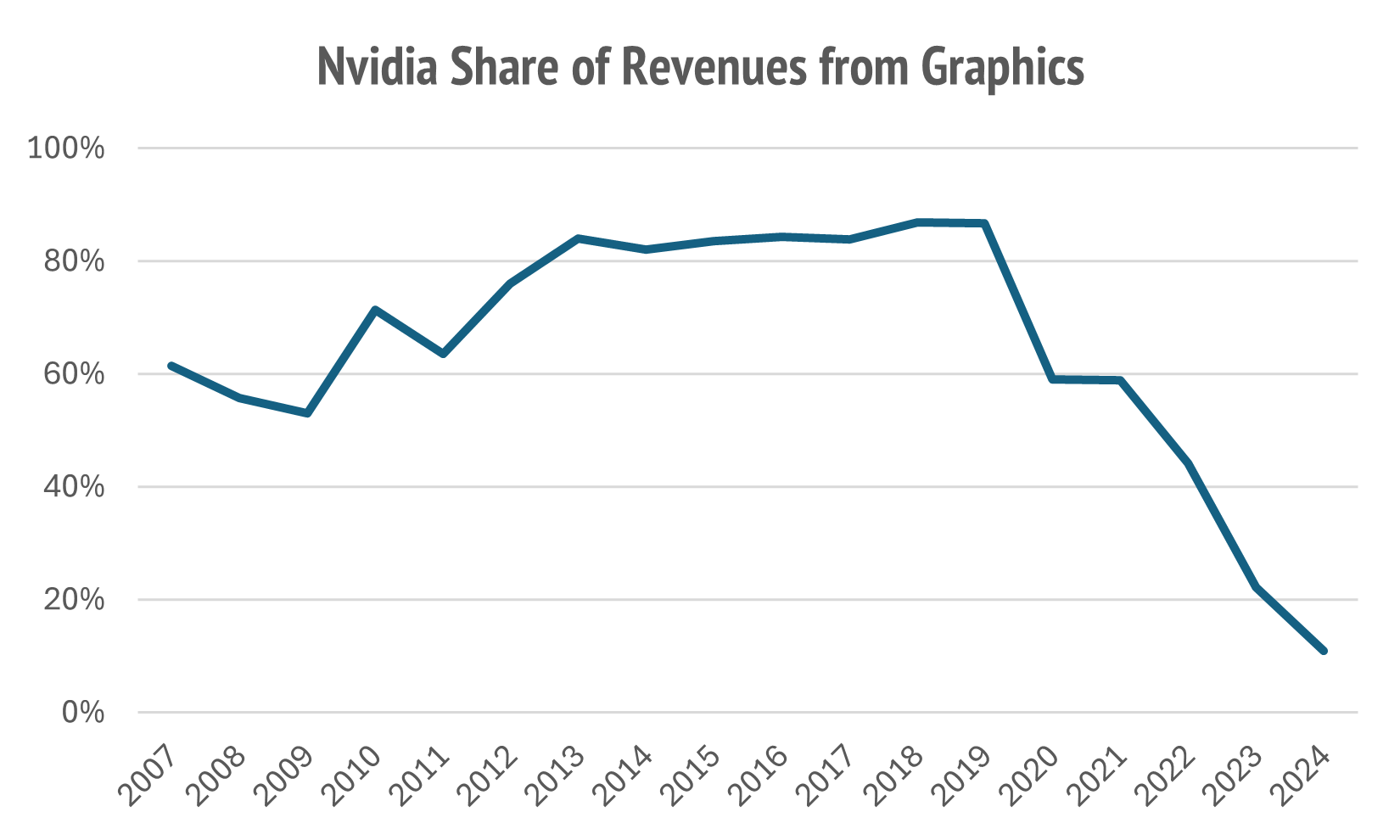

Around 2020, Nvidia really began to notice this change in their business and collapsed five revenue reporting segments: Graphics Processing Unit, Tegra Processor, All Other, Professional Solutions, and Media and Communications Processors to just two. The remaining segments are Compute & Networking, and Graphics.

In FY 2020 the split was 6.84B Compute & Networking and 9.83B Graphics.

In FY 2024 the split was 116.19B Compute & Networking and 14.30B Graphics.

The difference in CAGR is stark…

From FY 2020 to FY 2024 Compute & Networking grew 17x or 103% p.a.

From FY 2020 to FY 2024 Graphics grew 1.45x or 10% p.a.

The Nvidia business of today is completely different from five years ago.

The current YoY growth rate of Nvidia as reported in Q3 2025 is down to 62.5% p.a.

Of course, you would expect this growth rate to come down over time.

Let us imagine a five-year decline path for revenue growth rate.

Year 1: 60%

Year 2: 40%

Year 3: 20%

Year 4: 10%

Year 5: 0%

In revenue uplift terms, that compounds to 1.6 x 1.4 x 1.2 x 1.1 x 1 = 2.96 x.

That is still a sizeable uplift in revenue for a company with this momentum.

From the fundamental perspective, what will stop this is the buyer.

Supercomputing goes Mass-Market

Earlier, we pointed out that the growth in the graphics segment has saturated.

You can readily build a bear case on the upside for Nvidia selling ever more expensive graphics cards to teenagers and perma-children playing computer games.

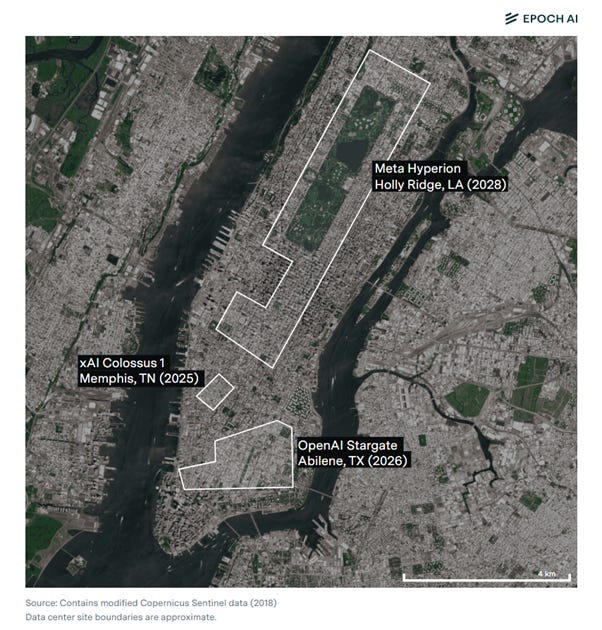

The typical power requirements will soon exceed those of a household socket!

Some version of this script will play out in the future of Manhattan scale data centers.

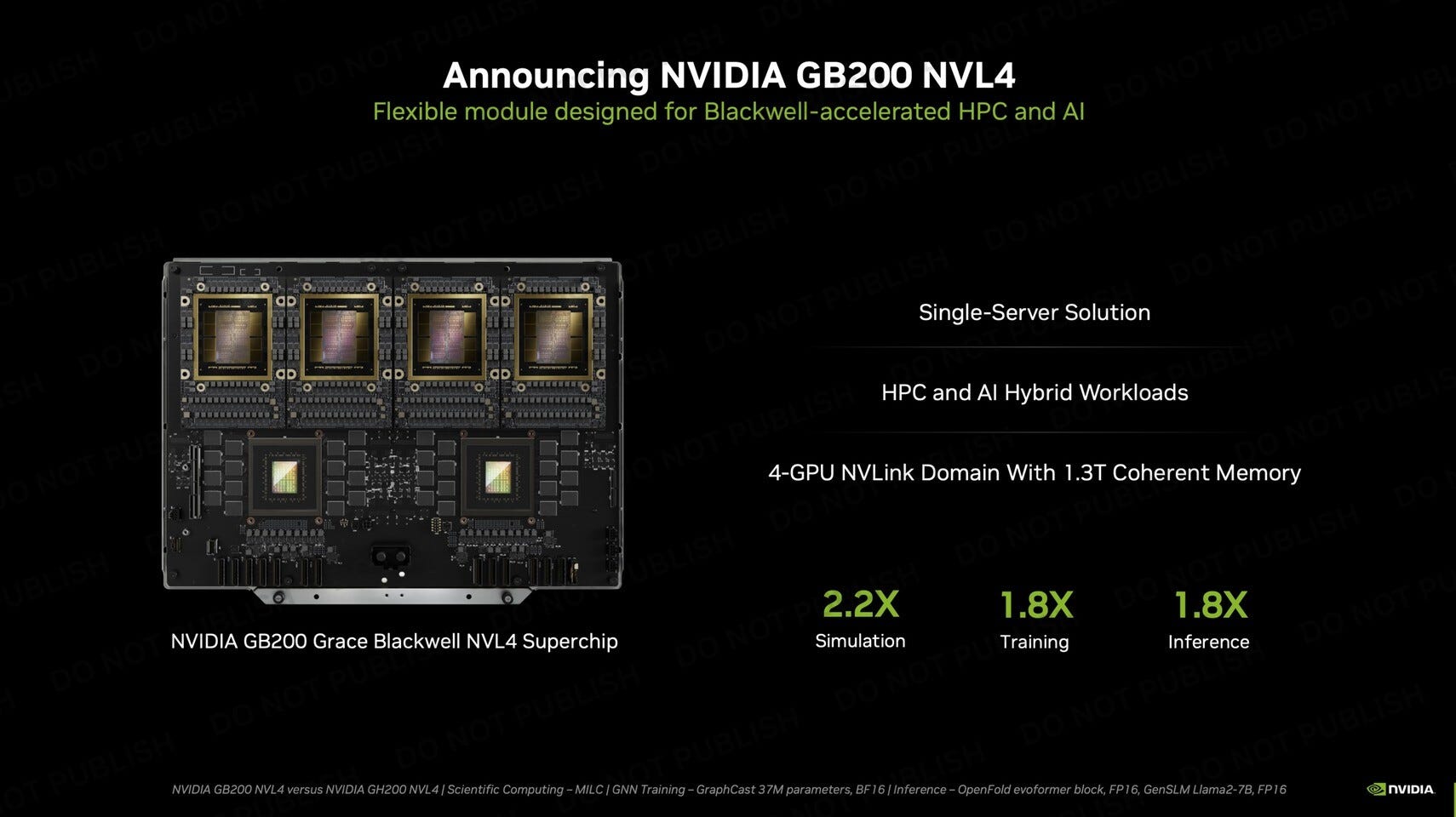

The new chips driving Nvidia revenues are not like the old chips.

The dreams of Jensen Huang, CEO of Nvidia, and the engineering team driving all of this innovation in supercomputing power, were always about this market.

The history of supercomputer development has many heroes.

When you spend a lot of money on a supercomputer, you may as well get a modern design icon in the form of an upholstered sofa as a bonus for the server room.

Seymour Cray conceived of a mass market for supercomputers in the 1970s.

It may have taken a while, but Jensen Huang has made it happen.

I do not mean to diss either gentleman, for their contributions to technology, to the business of computing, or the art of the sale.

If you own Nvidia stock, you should not care either.

This is sales conversion in action, and the revenue line shows it.

This correction saw me buy Nvidia stock after much thumb sucking.

What about Superintelligence Mumbo Jumbo?

If you need to sell a pencil, sell a dream of what you will write with that pencil.

I am a pencil nut, because I like to erase my mistakes and move on.

The Blackwing Pencil is my preferred instrument of notebook destruction.

It comes sold with a dream, that you might be the next Ada Lovelace, Keith Haring, or John Steinbeck. This is a great dream to purvey for the price of one pencil.

The dream being sold by Nvidia is of this character.

This is masterful salesmanship, for all the nerdy touches.

Nvidia is selling something that we all know.

This is the dream of what you could do with the right tool.

Presently, this dream is being sold to the other six of the seven most powerful men in charge of the most valuable, influential, and let us be clear, powerful companies on this planet. They are buying the dream, and they are competing to buy that dream.

This dream is sold as Artificial General Intelligence (AGI), but I do not buy that dream.

These tools are already very powerful in the hands of humans who are rational and know that they are imperfect. It does not matter. They will work with them.

What is Practical Superintelligence?

Humans are creatures of the mind, spirit and purpose.

We make tools to make better things in the real world, and better ideas about anything and everything that matters to us as human beings.

Ask yourself the following simple question.

Which is more powerful?

A: An intelligent human alone?

B: An AI that has been taught useful patterns from human experience?

C: A human using that AI to probe, test and extend their understanding?

Opinions may differ, but I think it is the third option C.

The “super” in superintelligence is not an either-or proposition.

Only humans know what it is to experience this life, and as much intelligence lies in the question as the answer. There is a natural dialectic to discovery.

If the availability of the Large Language Model (LLM) should promote the idea that there is no new question worth asking, then our civilization has indeed ended.

However, I do not believe that to be the case.

On the contrary, I am a believer in the Digital Humanities. When we can query some assembly of human knowledge, to better probe what areas warrant extension, we become more effective at generating new insight and novel understanding.

Like any period of tumultuous change in history, I do not expect plain sailing.

There is many a storm incoming, including the one where there is no power for the Manhattan scale data center that sprung up in the back woods of Louisiana.

The present capex boom will end when the credit spreads on hyperscaler debt blow out and the market refuses to fund any further expansion, in this cycle.

That end, in that manner, is surely coming.

However, I do not think it is here yet.

I am long XNAS: NVDA.

Happy investing.