The Market Schwerpunkt (Gold vs. Bonds)

The geopolitical contest between the USA and China is taking on the complexion of open economic warfare. We do not think the USA will win. Here we explain why.

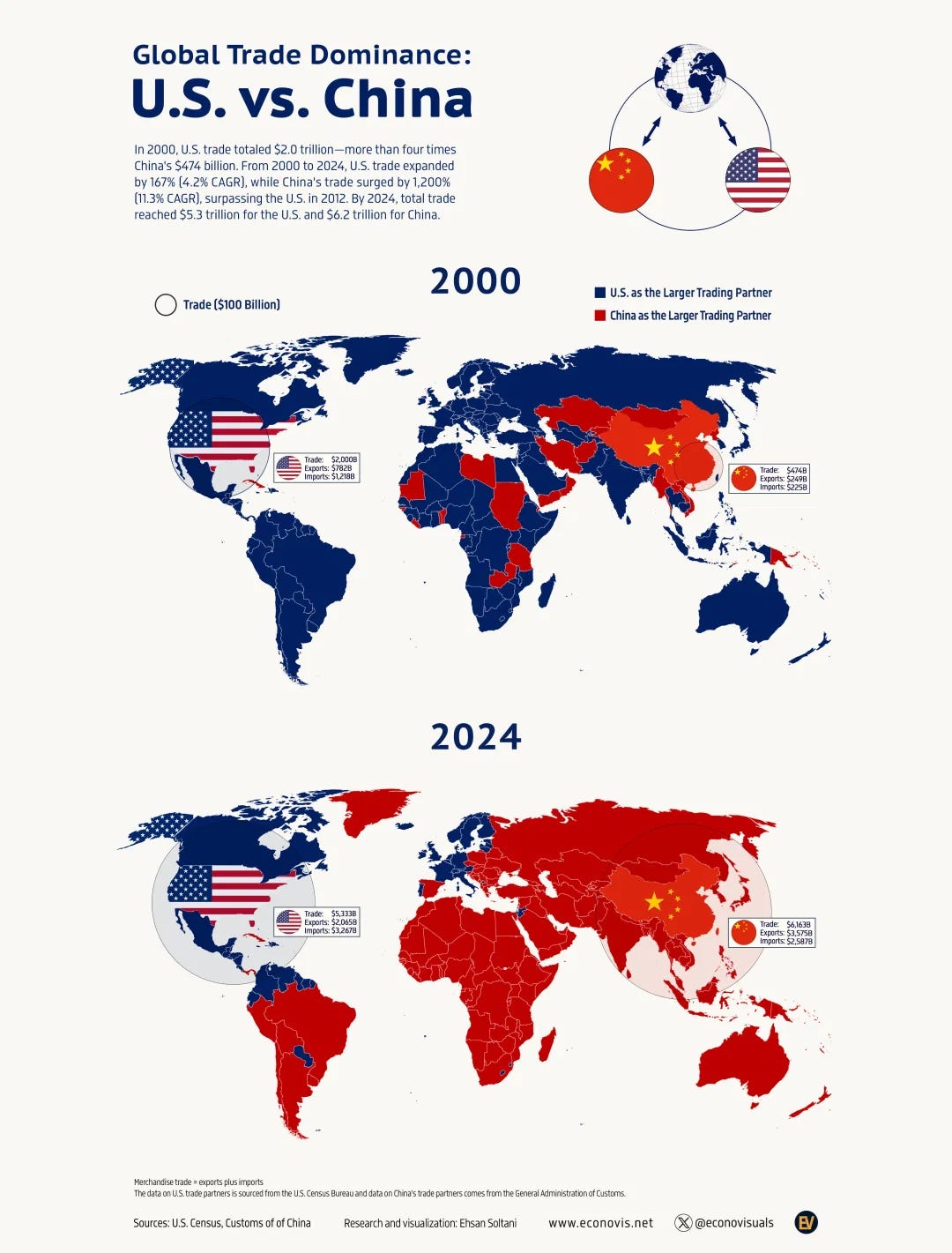

This world is big, but apparently not large enough to contain the USA and China.

I have no desire to play favorites, but the tenor of this geopolitical contest seems to involve the USA imposing yet more sanctions or restrictions on its adversaries which are met by countermoves to oppose them, or occasion reciprocal harm.

I have stated many times before that I think it is sensible to bet on the long-term success of both nations, the USA and China, because they each have merit.

However, in the short-term my purpose is to make a simple market call:

I do not think the USA can win any kind of war against China.

Let us leave aside the question of whether any kind of war is necessary. The thrust of this note is to state clearly that I do not think a “War of Choice” is a good outcome.

Furthermore, I think that were the USA to escalate current efforts to economically or militarily contain China, I think the probability of failure is close to 100%.

I do not believe that the hostility of the USA towards China can end well.

It cannot end well for either party, but it will be especially bad for the USA.

Why do I say that, even though it is contrary to Western rhetoric?

I am a realist, meaning I pay attention to the world as I find it.

I have no interest in populist fantasy, no matter how it is packaged and sold.

The USA is the largest economy in the world with the most powerful military.

It is also an innovative economy with attractive productivity growth.

The USA is the least dirty shirt among all Western economies.

The bulk of my personal capital is invested in US companies.

However, the USA cannot possibly win against China, in any contest, if it should choose to match its areas of weakness against Chinese areas of strength.

The basic principle of strategic competition is to deploy strength against weakness. The wrong thing to do is to attack where the line is strong.

Under the Trump Administration, the USA has chosen to undermine its own areas of institutional strength, by degrading the rule of law, weakening social cohesion, through a deliberate attempt to isolate and denigrate minorities, and to alienate its own allies with an ever-changing kaleidoscope of punishments and humiliation.

Given the parlous state of our Fourth Estate, few pundits acknowledge this.

Know this for a fact:

Professional investors pay attention to the facts as they find them.

They do not gild the lily, because that is how you lose the investment game.

Our aim is to win the investment game, so let us assess the game play.

We are in the middle of this game; we need to know how it ends.

This leads us to introduce a new concept:

The Market Schwerpunkt is that critical point of weakness where it cracks.

The term “Schwerpunkt” is now associated with military affairs though the writings of German strategist Carl von Clausewitz, his 19th Century classic “On War”, and the reinvention and deepening of that concept by Heinz Guderian, in WWII.

Was ist der “Schwerpunkt”?

The entire point of Blitzkrieg, during German armored operations, in the early part of World War II, was to deploy superior tactics on mobile divisions to go around any point of strength, like the French Maginot Line, penetrate weakness, and sow confusion and chaos in the enemy rear, until the line collapsed.

The Schwerpunkt is the main focus of attack upon a point of weakness.

If you simply read the bolded text, you can divine my argument and conclusion.

President Donald J. Trump is doing everything right to collapse his own line.

You may think this churlish, but I am a professional investor, and a realist.

I have no truck with fools who seem intent on self-destruction.

The best thing to do in life is to avoid fools; the best market action is to short fools.

The point of weakness in the contest between the USA and China is Trump.

This may sound peculiar, since he positions himself as a strong man.

However, victory in military affairs is rarely about brute strength.

The Yamato, and her sister ship, the Musashi, were the most heavily armed battleships ever constructed. The growth of naval airpower, from American carrier groups in the Pacific War, eventually finished off the mightiest of battleships.

This is why we now regard the carrier strike group as the symbol of real strength.

The USA operates eleven nuclear-powered fleet aircraft carriers, which are unmatched for power-projection anywhere on the seven seas of this planet.

With force like that how could the USA possibly lose?

The easy way is to assume you are in a military conflict when you are not.

The rhetoric from Washington is that China is an expansionary power whose intention is to militarily dominate its sphere of influence to become a new hegemonic power.

Whether the American strategy to combat that Chinese strategy works will depend entirely on whether the assessment of intention was correct.

If China has no intention to initiate a war, then the US strategy will fail.

The point of any long-term strategy in a Great Power Competition, is to play to your strengths, and minimize your exposure to attacks on your own weakness.

As we aim to show, China is prosecuting this strategy very well.

In contrast, the USA appears to have misread the game play entirely.

Defeat will follow to those who cannot read intention and respond appropriately.

The US Geopolitical Strategy of Containment

The Achilles Heel of any Great Power is the arrogance that comes with great power.

In the Greek mythology, the Goddess Thetis was said to have dipped her son Achilles in the River Styx, which divides Hades, to grant him invincibility in battle. He was so, except for one spot on the heel she held. The arrow of Paris found that spot.

The USA is definitely the most powerful nation, in a military sense. The key areas of this strength are force projection by the US navy, and trans-continental airpower.

The global network of bases provides the means for force projection.

The actual number of US bases is around 700, but it is hard to pin that down. The above map seems recent, but I note that it excludes RAAF Base Darwin.

Nuclear capable B-52H Stratofortress bombers are regular visitors to RAAF Darwin, on training exercises, meaning recall and repositioning from Guam in event of war.

When you have an empire to run, the business of maintaining the military network to hit any place on the planet, in the blink of a Presidential Eye, is business as usual.

Among the local cognoscenti, for all things US Alliance, Elbridge Colby, is considered the rising star of US Geopolitical Strategy with his grand vision of “Blocking China”.

In the Trump Administration, Elbridge Colby is now Under Secretary of War for Policy. Colby is considered the architect of the new National Defense Strategy of the USA, which calls for homeland defense and the Western Hemisphere as priorities.

The recent commentary downplays the focus on China, but that is misdirection.

The central thrust of US defense policy towards China is a “strategy of denial” that is focused on the First Island Chain. The present effort is to rope in allies.

If you search “First Island Chain” you will soon piece the story together. This is overt and explicit, as all US strategy has forever been. The strong tell you they are so.

The essential strategic logic of the First Island Chain, and the Strategy of Denial, is a classic case of generals who fight the last war, because that is easier than thinking.

Supposedly, the PLA Navy (PLAN) must be stopped at the first island chain, lest it go forth and conquer the Indo-Pacific. This is what it takes to be a US strategist.

Of course, the strategy of denial makes perfect sense if it is your intention to hold China at risk of a Western naval blockade of its commercial shipping lanes.

The best way to bring China to its knees is to stop anything getting into or out of China by sea. This strategy has been tried before and was successful (sort of).

During the Opium Wars of the 19th Century, the British Empire, and the Chinese, fought numerous battles over trade concessions, and maritime corridors.

You can read history how you wish, but the use of British Naval Force prevailed in forcing the will of the British Empire on the Chinese nation, in the 19th Century.

In the lead up to the Second World War, Imperial Japan was fighting a war in China to acquire territory and found itself blockaded by the USA. The specific target of that blockade, the Export Control Act (1940), was trade in war materiel.

That was successful, up to a point, but Japan then decided to attack the USA, in the infamous surprise attack on Pearl Harbor on December 7th 1941.

Blockades of commercial trade can cause serious harm to adversaries.

In some cases, they cause sufficient harm to change the calculus for war.

They might cause so much harm as to make War look like the cheapest option.

To close out this discussion, it is worth noting Colby’s contribution.

If you like military affairs, this all seems very cute, and many love it.

What better way to defend America than to bottle China up?

The problem is that for every action to telegraph strategic intent, there is likely to be a considered counterreaction. If China believes that your ultimate purpose is to limit any freedom of navigation in its own nearshore waters, it is likely to respond.

If your mindset is to “get China” and “hit them where it hurts” this sounds great.

The problem is that you have set in motion a chain of events which is likely difficult to control. The earlier essay, by Colby, A Strategy of Denial for the Western Pacific, makes the hinge-point of the strategy crystal clear:

Contrary to some commentary that suggests the military dimension in this dynamic is not that important, the U.S. military’s role in this strategy is central. This is because Beijing will likely not be able to dominate Asia without resorting to military force. While China has enormous and growing economic and other nonmilitary forms of influence, it is finding it difficult to use its leverage to get neighboring countries to accept what would essentially be a tributary relationship. - Elbridge Colby (2023).

There are several assumptions behind this statement that are worth highlighting:

Beijing wants to dominate Asia in a coercive fashion

Chinese dominance likely involves the use of military force

China has little leverage with other nations except the use of force

There are presumptions here that are not subjected to any detailed analysis.

China has enormous leverage through commercial trade, because it is the second largest market on the planet, and by far the largest for commodities.

The Chinese automobile market is larger than that of the USA, Japan, Europe and India combined. There are more cars made and sold there than anywhere else.

Despite such facts, the assumption of US Strategists is that China must inevitably go to war in order to realize its ambition to be a global hegemon.

Excuse me? Is this not the pot calling the kettle black?

The problem for the Strategy of Denial is that it makes war more likely not less so.

The issue for the USA is China may choose a different form of warfare.

The warfare of choice, for China, may not be military at all.

What could that form of warfare be?

Where is the Achilles Heel for the USA as a Great Power?

The Chinese Geopolitical Strategy of Commerce

In my view, the best strategy in life is to be competitive, but to avoid open conflict.

Sledging is fine. It is not cricket, but it is okay within the rules of cricket.

It is not too hard to divine the Chinese long-game.

The USA has military bases all over the planet. China has trading subsidiaries.

As far as I know, the Chinese did not bomb too many places to get there.

There are many allegations that they conducted trade unfairly and did horrible things like finance public infrastructure with loans. This is considered evil by our banks.

I am not going to dwell on this because it is obvious.

China knows how to trade more widely and effectively than the USA.

In American business, it is accepted that the business of America is business

The business of China is more business than America knows how to do.

It is that simple, and you can save the rhetorical outcry for the think tank circuit.

How Does this End?

If you know little about the areal distortion created by the Mercator projection, the best way to turn some red to blue is to invade, or annex, Greenland.

Fortunately, for Australia, we look small compared to Greenland, but I do think we should worry about the Australian Antarctic Territory, as that looks big.

China probably thought it was winning, and winning big, when it bagged Greenland as a trading partner, to service all 56,500 residents, some of whom need cars.

The USA plans to win the place over by making it a nuclear target.

This plan can work; the USA won our former PM Scott Morrison over by making Perth a nuclear target with an agreement to host American nuclear submarines there.

China countered by insulting us publicly, blocking wine exports, and then walking it all back by attacking Toyota for domestic market share shipping automobiles to us.

The bill from the USA, for their help with defense will be $368B AUD for some Virginia class nuclear submarines, that are second-hand and help from the UK to design the SSN AUKUS nuclear submarine. This will keep defense auditors in work for decades.

The bill from China, for trading with Australia, was a $110B trade surplus in favor of Australia in the year of 2023 alone. Ten years of that might pay for AUKUS, and the help we received from the USA, once the auditors complete the adjustments.

You can see how this (undiscussed) narrative is playing to the strengths of the USA and the weaknesses of China. Australia wins from China and loses from the USA.

That is the way it should be and the reason the public narrative runs this way.

I am not foolish; I expect this public narrative to continue. Elbridge Colby has told us all that China cannot possibly prevail with its Asian dominance plan without some future military conflict. That way we recycle our China surplus back to the USA.

Australia will buy submarines in USD and earn USD selling iron ore to China.

This way the Australian trade surplus in iron ore can be recycled back into a dollar denominated export market for the USA. That math works, why fight it?

In the same 2023, trade figures, Australia ran a $31B trade deficit with the USA.

Clearly, this number is all wrong.

If we added another $50B a year of US defense equipment purchases to that number, that would leave another $30B a year of US imports to find. Follow this logic through and it is not too difficult to see how trade tariff coercion is designed to work.

Australia does not have a functional press so this plan will definitely work.

For the plan not to work, you would need some Australians to be thinking.

Fortunately, there are many, but none of them are Members of Parliament.

Labor Minister for Resources, the Hon Madeline King, seems to think it is a good idea to sell Australian Critical Minerals into the USA, and not China.

The idea is that we should not sell Critical Minerals to China, which is far and away the largest raw materials market on the planet, but to sell them to the USA instead.

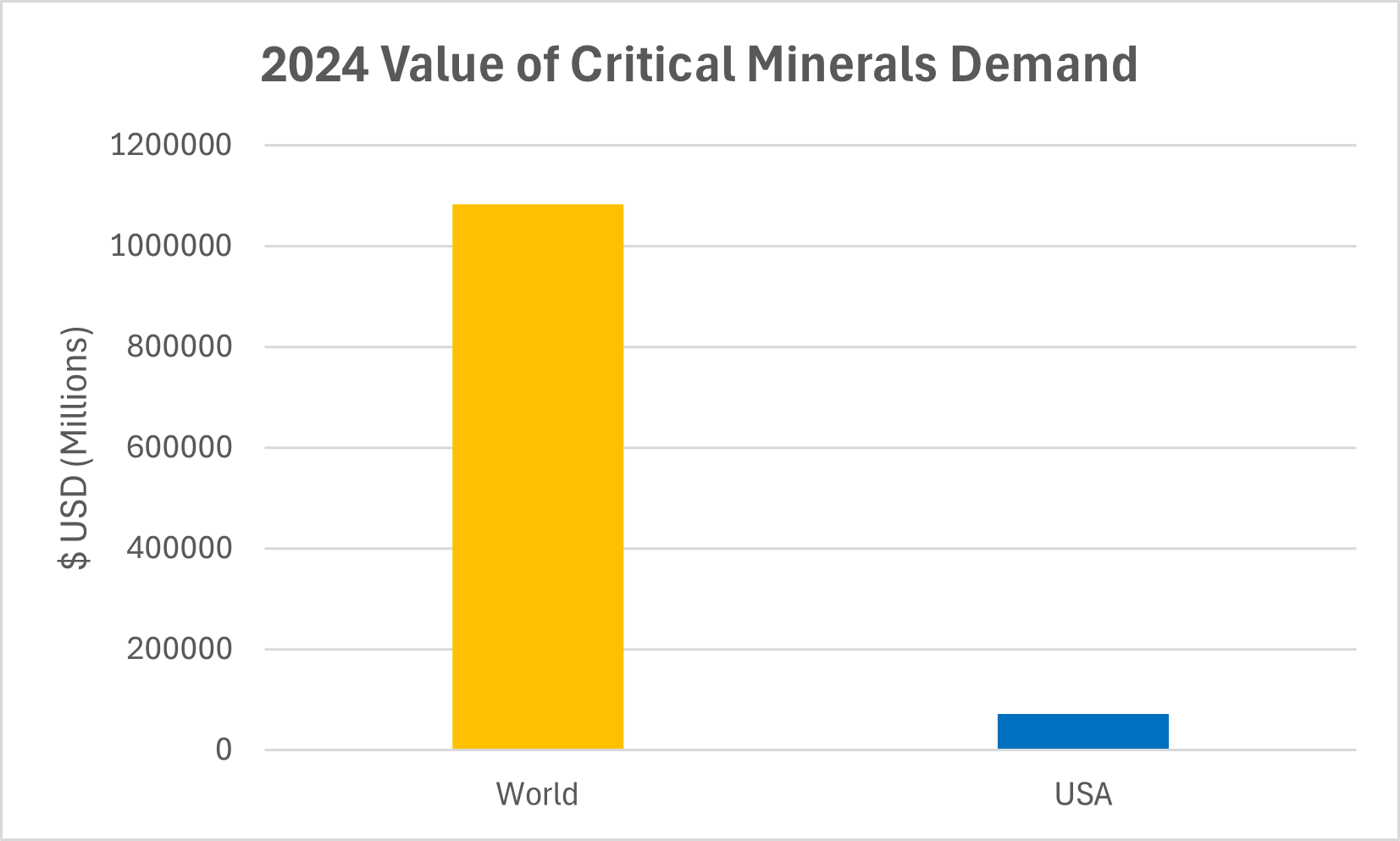

Let us look at the aggregate market value of all minerals classed as Critical Minerals by the US Geological Survey using their public data release for the year 2024.

If Australia had an effective industry policy community, astute politicians that worked in the national interest, a functional press, and a sentient finance community, there is a slim chance somebody might have noticed the above comparison.

The USA is about 6.7% of estimated Global Critical Minerals demand, by value.

This is across all 60 Critical Minerals, which includes Copper and Aluminum.

If you look at the Rare Earths, the position is worse.

The actual demand estimates - from official US data - for the year 2024, put US Rare Earth demand at $231M USD, and the total World demand at $13.65B USD.

Translating that to percentage terms: the USA was 1.69% of World demand for the Rare Earth complex in 2024. Furthermore, they were the low value Lanthanum and Cerium compounds used in the manufacture of Oil and Gas Industry catalysts.

They were not the high value Neodymium, Praseodymium, Dysprosium and Terbium that are used in high-performance Neodymium-Ferro-Boron (NdFeB) magnets.

There were no F-35s involved.

That all got shipped in as finished product from China!

If we look at Rare Earths in the context of US Critical Minerals it is small.

This is perplexing, is it not?

Why all the fuss about rare earths when they barely matter?

There is a natural corollary:

Why is Australia expending policy energy on the USA and Rare Earths?

The ultimate reason for that conundrum will only be found in Washington D.C.

However, I can hazard a guess based on Colby’s strategy of denial:

The likely strategy of the USA is to contain China by restricting Chinese access to raw materials. What matters is that China does not get them. It does not matter that the USA has no meaningful market to absorb the surplus.

The shrill warnings about Chinese military expansion are simply the bait.

Nations like Australia are likely to swallow that bait, which is why we are increasingly bearish on the long-term outlook for Australian mining.

Unless the Australian Government makes a clear policy course correction, it seems clear that Australia will be forced into a system of military tribute.

Australian trade surpluses from mineral exports to China will be tolerated by the USA so long as we dutifully recycle those into imports from the USA.

The chief large ticket item will be defense and military industrial complex goods.

The message from Elbridge Colby to Australia is crystal clear:

Accept a tributary relationship to the US Imperium as a happy vassal.

My family ancestors, my grandad, and his brothers, fought their way up the beach at ANZAC Cove, Gallipoli, on April 25th, 1915, fighting for King and Country.

My family history makes me patriotic enough to reject the Colby Bargain.

If you will forgive the emotion: he can stick that bargain where the sun don’t shine.

Domestically, this charade ends when the nation wakes up to the game.

What is the right trade?

The Gold vs. Bonds Trade

Elbridge Colby, and others, have correctly identified that China is intensely vulnerable to a naval blockade of the First Island Chain to choke off raw materials supply.

RAND Corporation has already gamed out the background theory.

President Donald J. Trump is asking for a 50% increase in the US Defense Budget for 2027, to the gleeful approval of many in the US press.

The 2026 National Defense Strategy demurred that the main challenge was not China but the Western Hemisphere. Then President Trump asked for a $1.5T 2027 budget.

Call me a cynic but I am an investment professional of three decades standing.

When I add up the signals, I arrive at one obvious high probability inference:

The strategy now active in Washington is to get Western allies to sign up to a policy of restricting raw materials and equipment exports to China.

The price of being viewed as a worthy ally is tribute: dollars, investment in the USA, and orders for US defense equipment, oil, natural gas and other items.

This is a naked strategy for the Imperium to extract rents through tribute.

The obvious way to play this strategy, in the markets, is to buy the US beneficiaries of the strategy, which are chiefly defense companies, oil companies, and cyber firms.

Just buy a bouquet of US listed beneficiaries of Imperial Tribute.

That is a sound strategy, and who could blame any American for doing so.

Indeed, if you are a global investor this cynical policy makes perfect sense.

That is why the stocks will go up this year and especially going into 2027.

However, that feels like submissive surrender to this Australian.

I have the blood and DNA of true ANZACS, so I do not lie down easily.

Equally, there is an inner Barbarian in me that delights at the Sack of Rome!

If Australia is to be forced into the position of a weak submissive vassal to the glory of a foreign imperium, then this Visigoth from Downunder will find a way to get paid.

No Australian can trust their political leadership, that is now crystal clear.

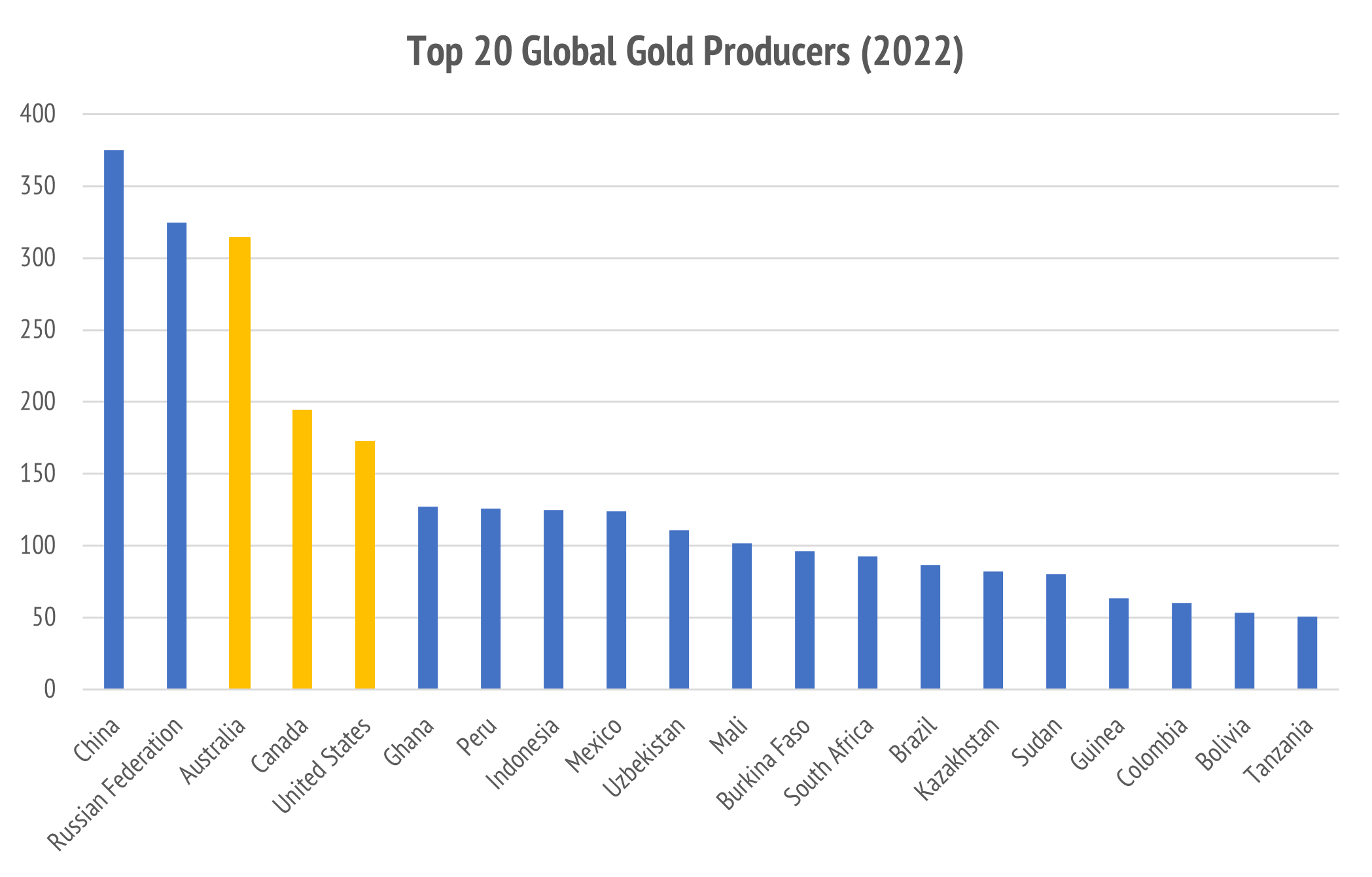

However, Australians can trust their cunning to find a path out. Gold figures strongly in that way out, as the number three position of Australia in production means that this nation benefits greatly from higher gold prices.

The Achilles Heel of the Imperium is hiding in plain sight.

For the tributary phase of the US Imperium to work, three things must happen:

Willing Vassal Puppet leadership must be installed in all allied states.

The export of weapons, oil, and gas, must increase

Extraction of financial rents from foreign subsidiaries must rise

The first measure has been 100% successful in Europe, Japan and Australia.

The vassal goose will not complain when it is plucked naked.

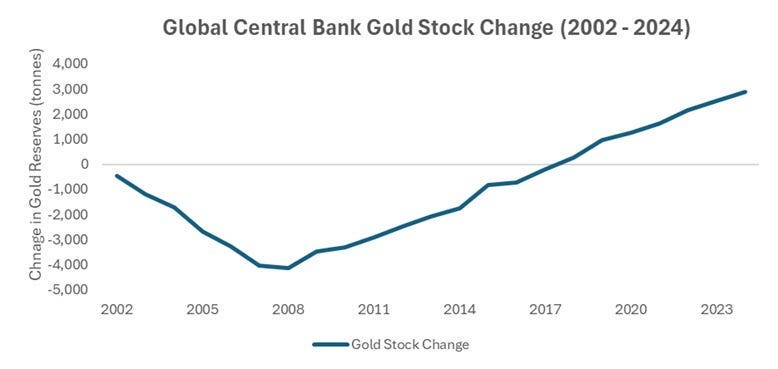

However, there is a background problem with the US Debt. Foreigners are not buying as much, and the Chinese have significantly reduced their holdings.

We can see that the Market Schwerpunkt is the alternative to US Treasuries.

The Central Banks of this planet figured that out in 2008, and switched from net selling to net buying of gold, which has continued ever since.

I wrote about this in April 2025 with: Best Global Idea: ASX Gold Stocks. There you can see this chart of net Central Bank Gold buying since the Global Financial Crisis.

Gold is now in a raging bull market, and the tempo has gotten electric.

When you realize that selling bonds is a confidence game, and you can tell that the USA is desperate to find new buyers for their bonds it is easy to see the setup.

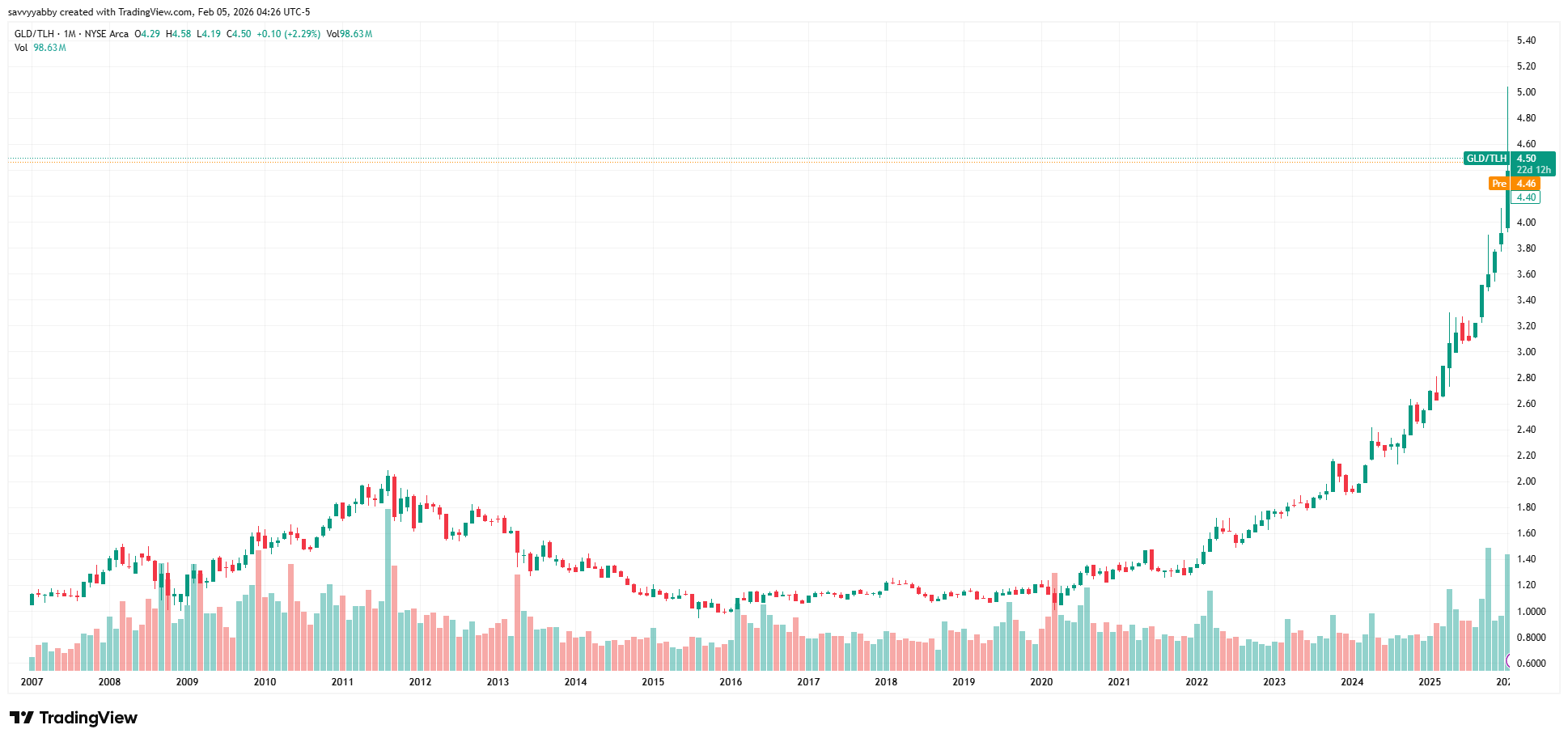

The right thing to do is to compare the total return on holding US Bonds to the total return on holding gold, which pays no interest. You can do this easily enough, using the relative price spread of two ETFs. ARCA: TLH for 10-20 Year Treasury Bonds, with the distributions of incomes reinvested, and ARCA: GLD, the SPDR gold ETF.

I use Trading View, where it is possible to do those adjustments on the chart.

I set this up with Bonds on top, as numerator, and Gold below as divisor. The chart going down says Gold has been winning over Bonds since about 2020.

Coincidentally, that is when US trade and sanctions policy first started ramping up to contain China in high-technology areas like computer chips for AI.

To make it more obvious what is happening let us reverse the chart: Gold vs. Bonds.

The rhetoric in many Western financial newspapers is about “crazy and impulsive” retail investors buying gold in a frenzy of naive trend following.

Retail investors are following the trend set by Central Banks.

Outside of funds management, where you get paid even if you underperform, those who use their own money achieve no compensatory upside if they go lose it.

Work out your own conclusion as to whether it is wise for a BRICS Central Bank to buy Gold or US Treasury Bonds. Work out why the USA wants to control commodities.

Let us turn up the heat now and look at Silver: ARCA: SLV versus ARCA: TLH.

Once you understand this dynamic, it is easier to interpret the trading action. Silver is a thin market, with not a lot of physical liquidity. In tonight’s session it will be down.

The stakes are very high in this game.

The Market Schwerpunkt is Precious Metals vs. Bonds.

Follow that relative spread closely as it is the one Scott Bessent is trading.

Once you understand that this market will be easier to navigate.

Conclusion

This note is unusual in that I have taken a firm view on matters it is considered impolite to talk about in financial markets.

I know that.

However, I am also living in a nation that stands to lose big if it simply rolls over and submits to US demands due to the exceptionally weak leadership class we have.

The best way to protect your financial future is to understand what is going on, and to hedge the risks as best you can. The military dominance of the USA is clear.

Buy a basket of US defense stocks to benefit from the Imperial dice roll.

However, the financial vulnerability of the USA to a bond crisis is also clear.

Buy precious metals to hedge against a US centered financial crisis.

There is no way to tell what happens in any given trading session.

However, the tension in this market is very clear.

Gold vs. Bonds is the Market Schwerpunkt

Pay close attention to that and your chances are improved.

Domestically, the Australian balance sheet is strong.

Continue to hold well-valued Australian banks, miners and industrials.

Happy investing!

Addendum: The View from Hong Kong

Someone asked me for the relevant spread in Hong Kong.

Thus far I have not found an appropriate duration match for TLH.

However, there is a ten-yearish duration (Effective Duration = 5.47 years) CNY PRC Government Bond trading in Hong Kong under the ticker HKEX: 2829.HK.

There is also the Value Gold ETF HKEX: 3801.HK

You can take a Hong-Kong based investor view of this spread via 3801/2829.

It can be difficult for many people to understand that gold does not need to pay any interest to handily compete with an interest-bearing investment in a wide monetary inflation. The Chinese economy has producer price deflation, so it seems odd to see similar effects showing up in China. However, China runs a soft peg for the Yuan, in the form of Renminbi, into Hong Kong, and the HKD is pegged to USD.

The monetary inflation now active in the USA leaks into China via this peg. Were the Chinese currency to adjust upwards, the local price structure in China would stay relatively unchanged, but receipts from exports would fall.

Imports to China would look cheaper, and that is the likely end game.

However, China will resist revaluation to maintain export competitiveness.

This is a tug-of-war between two stubborn mules: the USA and China.

The USA would like to revalue downwards.

China will resist the revaluation upwards.

In this scenario, the global price structure of fiat money is falling relative to measures of real production effort, like copper and gold, but not oil which is oversupplied.

It takes no effort to run a printing press.

It takes effort to find, mine and refine gold.

At some other time, we will look at Knut Wicksell’s theory of the natural rate of interest and how this relates to the commodity production economy.

The Market Schwerpunkt is Ground Zero for a Monetary War.