The Value of Tax-Deferred Capital Gains

There has been public angst over the recent Capital Gains Tax changes. While the PAYG CGT discount has gone, the higher tax rate does not change the optimal strategy. Growth wins over income.

It is said that:

Only two things in life are certain: death and taxes.

I cannot defeat either, but I can describe the optimal strategy for investment, to achieve a higher after-tax rate of return, via growth or income.

What I am about to explain is standard in finance.

Any qualified financial advisor, anywhere on the planet, will agree with me that the deferral of tax to achieve long-term capital growth is the optimal investment strategy. It is elementary compounding mathematics.

Of course, you need to make assumptions to prove this, but they are simple.

Assume the tax rate on annual income is the same as that on capital gains.

With these assumptions, I will show you how to prove this result.

It is both simple and sound.

I will offer the most important piece of general financial advice you will hear.

If your financial advisor says otherwise, show them this note.

Ask them a simple question:

Please explain?

If they still do not understand, send them my way, and I will explain it to them.

That is all there is to it.

Taxation on Income versus Growth

To simplify analysis, consider this investment scenario.

You have two investment options, each offering the same pre-tax return of R% per annum and your marginal tax rate is T, applied equally to both.

Which should you choose?

Naively, you would be indifferent.

After you have paid tax at rate T, the post-tax return is R (1-T).

How could it matter which option you choose?

The post-tax annual rate of return looks the same, doesn’t it?

Well, in the real world, the after-tax rates of return are NOT the same.

This is not a social media narrative complete with viral video.

It is simply a mathematical fact that is true for all R >0 and Tax rates in the full range of T = 0 to T < 100%. If T >= 100% then you should move your tax residency.

The reason may be traced to compounding when you defer capital gains.

The Option to Defer Capital Gains Tax

Those who pay attention to the mathematics will do better in the long run.

The full Einstein quote reads:

Compound interest is the eighth wonder of the world. He who understands it, earns it... he who doesn’t... pays it. - Albert Einstein

Income and capital gains are not treated the same by the taxation office.

You pay tax on income in the year you earn it.

You pay tax on capital gains in the year you choose to realize them.

This looks like a minor difference to those who do not grasp compounding.

However, it is a massive difference in practice.

The entire period you amass unrealized capital gains you have a zero-interest tax free loan from the government to finance your future tax liability.

It gets even better with inflation indexed capital gains.

Under inflation indexing your future capital gains tax liability is financed by the tax office at an effective nominal interest rate equal to minus the CPI.

That is the mathematical reality of tax defered capital gains with indexation.

Note that I have been comparatively silent on the impact of the recent CGT changes. The rest of the industry ran around like chooks in a barnyard.

Once you read on, you will see why I did not join this foolish public melee.

Those who did can read this and make their excuses to their clients.

Their clients pay them for good advice.

If they got bad advice they may want their money back.

The After-Tax Return of Income versus Growth

What I am about to show you is a standard result in every financial advice curriculum.

If your financial adviser does not know this result you should ask them why.

Normally the result I will show you is stated in words without proof.

I am a mathematician so I will go one step further and prove the result.

The result in question is this:

For any rate of return R >0 and tax rate T that is in the full range of 0% to 100%, the after-tax return of growth investment is better than or equal to that of income over any period.

The jargon used by the industry is to say that growth dominates income.

Notice a few caveats of no great importance.

Income investments can come with tax credits, like franked dividends. This means that you should compare rates of return pre-tax with credits added back.

Australian investors know the rule for our tax system.

If you receive dividends franked at 100%, the gross-up for the tax credit is obtained by adding back the franking credit amount. This means your franked dividend yield of Y% has a tax-credit driven gross-up of 1/(1-t) where t is the company tax rate.

For large companies in Australia, that rate t = 30%, so the gross-up factor is 1.4286 which is 1/(1- 0.3). In effect, a 5% fully franked yield of 5% is adjusted to 7.14%.

With this caveat in mind, we will set R = 7.14% for comparison purposes.

In practice, this complicates decisions slightly, because many growth investments can also spin off some income. The tools I describe here can cater for that case.

This is free general advice so I will not do the warts and all calculation.

I would need to analyze the underlying investment to declare which is best.

With those caveats out of the way, let us do the calculation with no indexing of capital gains to properly emphasize the effects of compounding.

Indexing of the investment cost basis by any CPI>0 improves the result.

For clarity, it will also help to state a standard result:

After Tax Proceeds = (Pre Tax Proceeds) x (1 -Tax Rate)

This is clear, the money you wind up with is that with tax liability deducted.

That is the basis of the comparison we will run over N whole years.

I choose whole year tax periods to keep it simple.

You invest on 30th June of year Zero and realize gains on 30th June of year N.

The income investment pays an annual income, the tax due on that is paid, and the rest is assumed to be reinvested at the same comparison rate R% per annum.

This scenario is idealized, but not in a way that defeats the principle.

I want to make the tax deferral principle as clear as I can.

The Income versus Growth Sack Race

Let us now run the sack race.

Cue wild and whacky music…

After-Tax N-period Return on Income

Off goes Drooper the Lion, out of the blocks with the pure income strategy.

At the end of every tax year, the after-tax rate of return in that year is.

If you compound that over N full periods you get the post-tax gain:

You multiply your starting capital by that uplift factor.

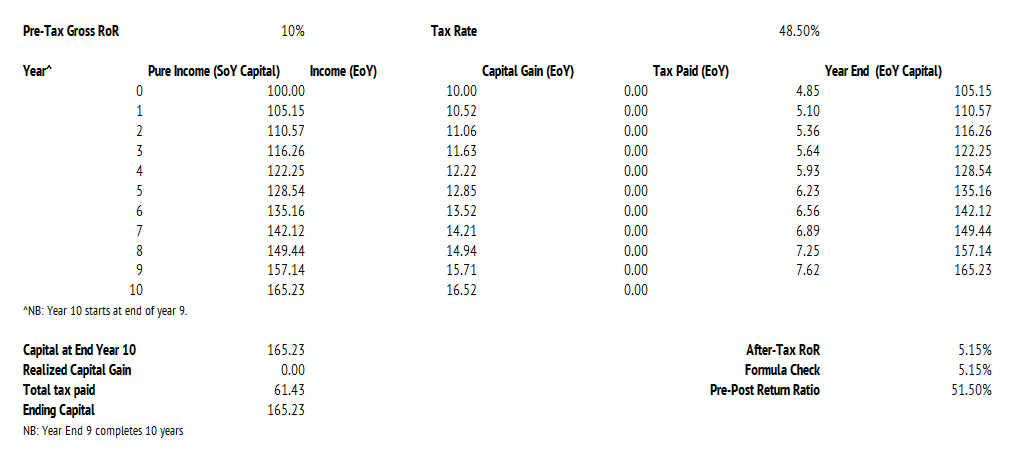

Let us do a simple example:

Starting Capital = $100

Pre-Tax Gross Rate of Return = 10%

Marginal Tax Rate = 48.5%

We run the race for 10 years and get this result:

You can see that the after-tax analysis is pretty simple for income.

You are compounding at the rate R(1-T) which is 51.5% of the headline rate.

For 10% RoR and 48.5% Tax you are compounding at 5.15% per annum.

After-Tax N-period Return on Growth

Off goes Bingo the Gorilla, out of the blocks with the pure growth strategy.

This is pretty simple to calculate, but we need to recognize that no capital gains tax is paid until the investment is sold at the end of N years, and then only on the gains.

The formula is easiest to understand if you first compute the gain factor pre-tax.

You do not pay tax on all of this capital, only the gain over N years. This is the above result minus one, the starting capital. You apply tax at the rate T and keep (1-T).

With a little notepad scribble you will get this result for the post-tax gain factor.

The above form is the most useful for later, but a little confusing to interpret. It looks like the effect of tax was to reduce your starting capital. This form is the same:

This makes it clearer what is going on. You compound starting capital at annual rate R for N years, subtract the starting capital to get the gain, and keep (1-T) of that.

We will use the first form later to prove dominance.

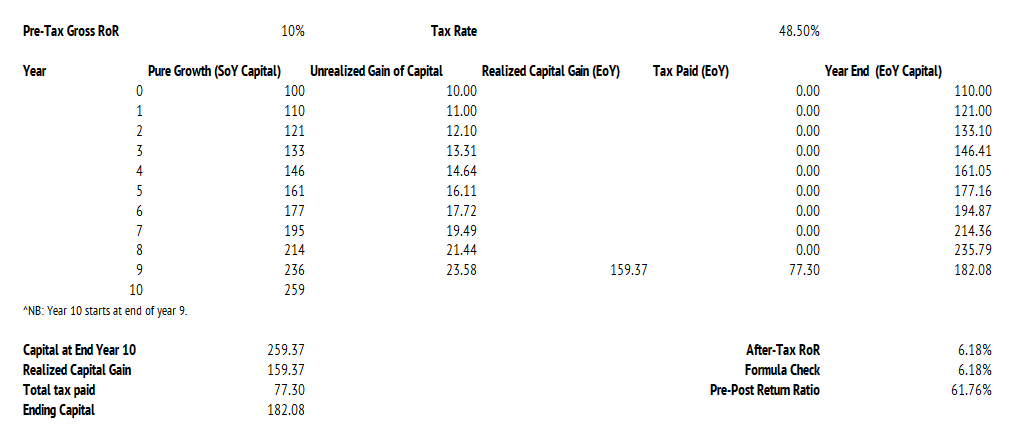

Let us repeat the former example.

Starting Capital = $100

Pre-Tax Gross Rate of Return = 10%

Marginal Tax Rate = 48.5%

We run the race for 10 years and get this result:

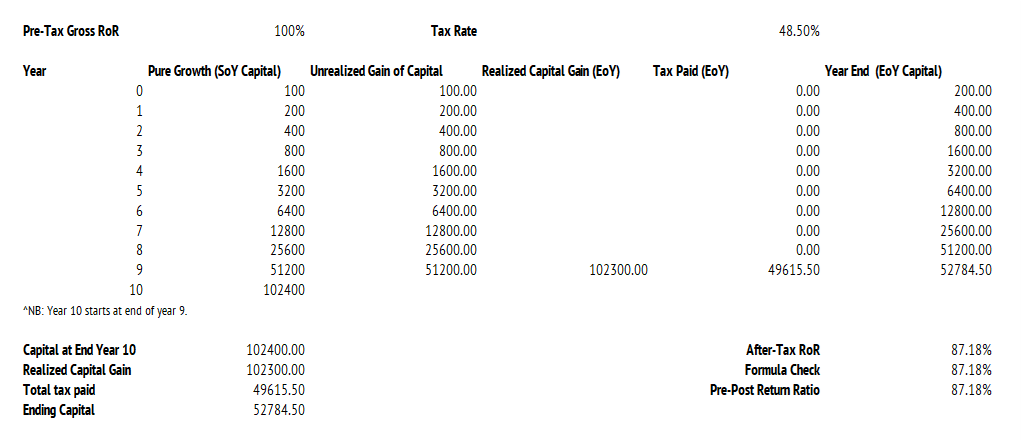

Okay, so the growth strategy won in this example over income.

Note that more tax was paid to the government in the growth strategy:

Income: total tax paid $61.43

Growth: total tax paid $77.30

If your objective was to pay less tax to the government, you would choose income.

If your objective was to be personally richer, you would choose growth.

If you accept that the purpose of progressive income tax policy is to make both you and the government richer, at the same time, you will both choose growth.

If you sell tax minimization advice you will tell clients to choose income.

If you want to be personally poorer after N years you will take that advice.

I am a portfolio manager of a wealth management business.

I take my own advice and choose growth over income.

Call me self-interested, but I am richer for it.

What about high growth investments?

I read the press like anybody else. Following the CGT changes I saw a lot of news reports by unlicensed financial journalists claiming that the tax policy changes would harm investors and the Australian economy by preferencing income.

I am a licensed financial advisor: I would go to jail for dispensing that advice.

The problem with this advice is that it is materially wrong and misleading.

If you tell your clients that you are dispensing unreasonable general advice.

It is objectively and demonstrably a false and misleading claim.

Any financial advisor, licensed by ASIC, has a duty of care to their clients to present any general financial advice on a best effort basis with a reasonable basis.

The term “reasonable basis” means well-argued and factually grounded advice. This is the professional standard to which we hold advisors.

If you do otherwise, namely allow your political persuasion to cloud your professional judgement to form and propagate unreasonable hearsay, that is a financial crime.

If you continue to dispense misleading advice with no firm and reasonable basis for that advice, then you are likely to receive the attention of our financial regulator.

The purpose of financial advice is to serve the client interest.

With that sermon of my chest, let us look at the high-growth investment case.

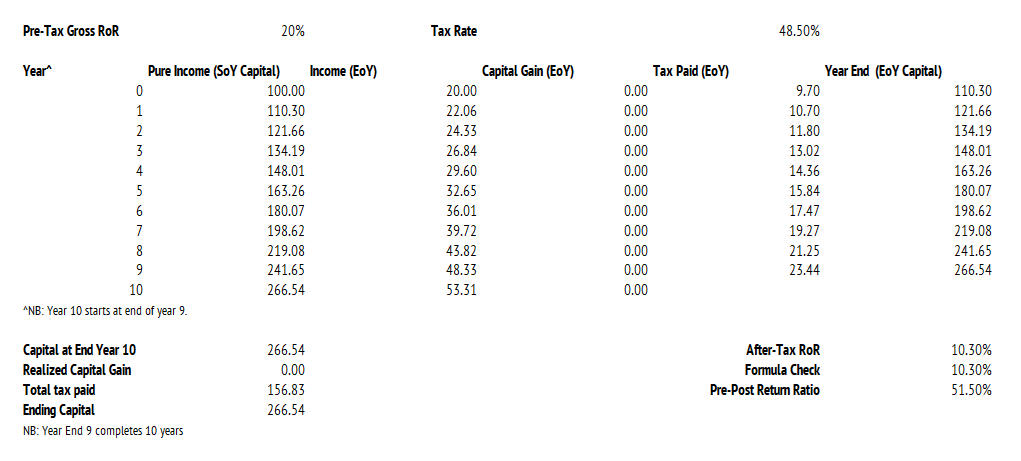

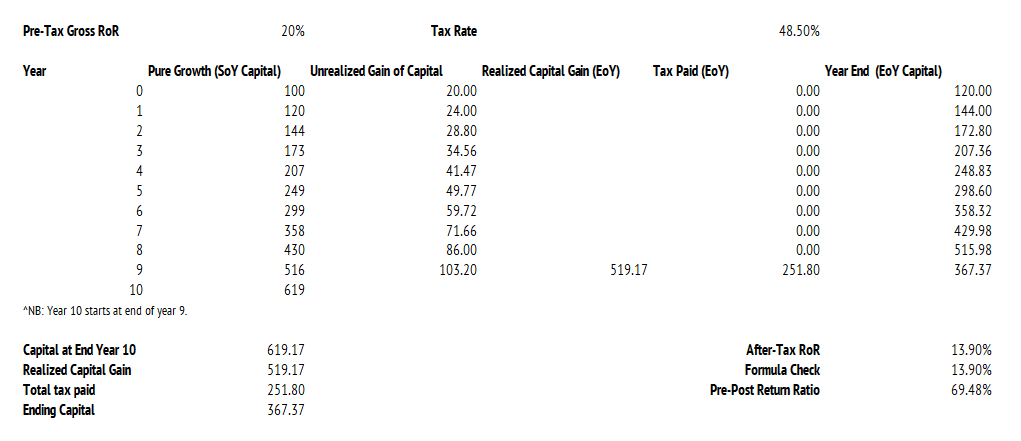

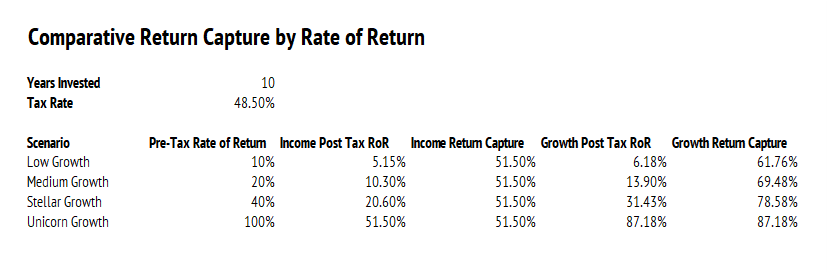

The Case R =20% T=48.5% N =10 years

Let us explore a higher growth example with R = 20%

Your professional tax advisor will point out that you saved tax choosing income.

Your professional wealth advisor will point out that you were richer choosing growth.

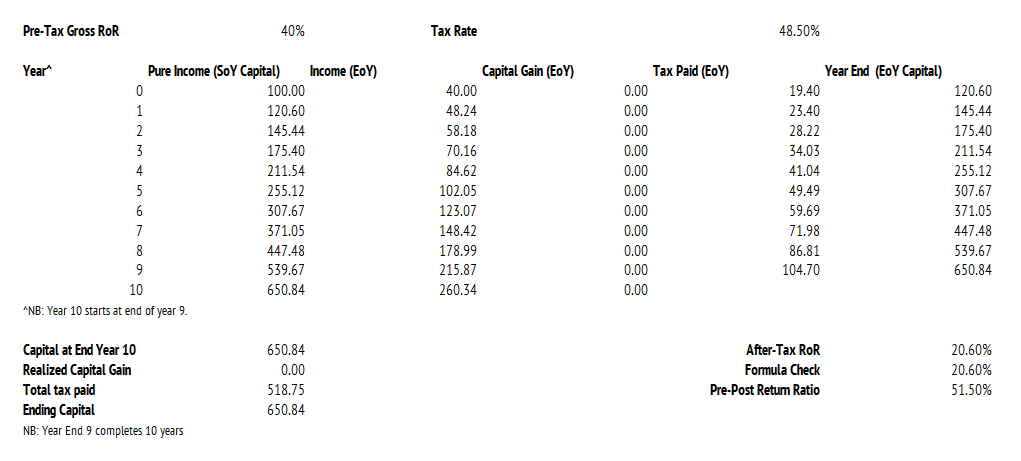

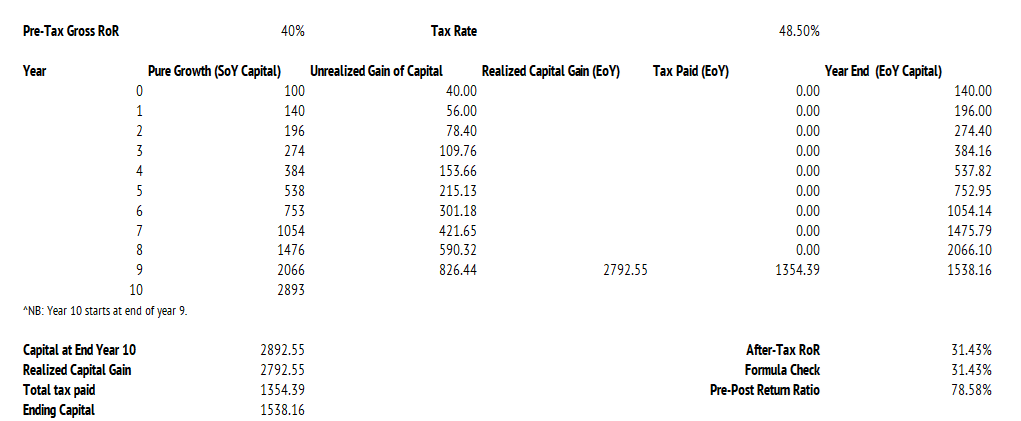

The Case R =40% T=48.5% N =10 years

Let us explore a higher growth example with R = 40%

Your professional tax advisor will point out that you saved tax choosing income.

Your professional wealth advisor will point out that you were richer choosing growth.

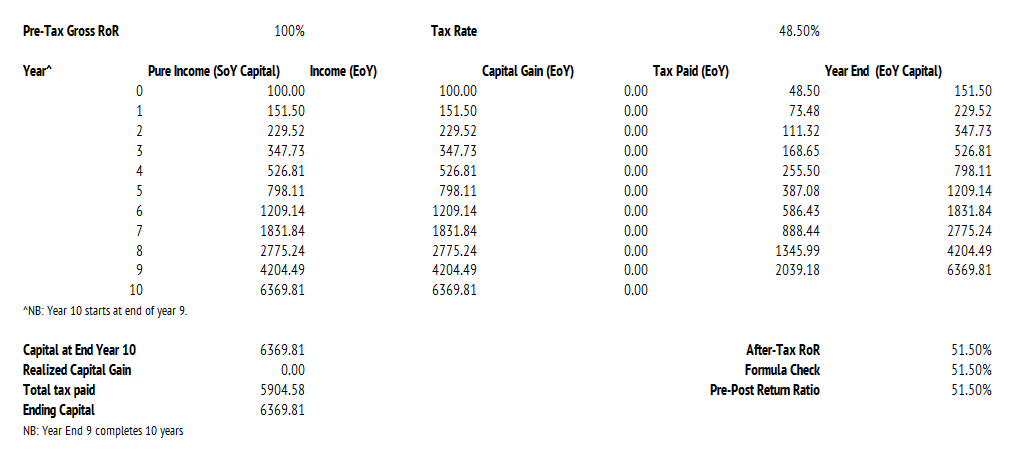

The Case R =100% T=48.5% N =10 years

Let us explore a higher growth example with R = 100%

Your professional tax advisor will point out that you saved tax choosing income.

Your professional wealth advisor will point out that you were richer choosing growth.

The Pattern and the Reason for that Pattern

Those who prefer to look at examples to infer patterns will have noticed this one:

Let me state this clearly in words so that there can be zero doubt:

The share of the pre-tax rate of return left in the hands of the investor after paying capital gains tax increases with the rate of return.

Contrary to widespread assertions in the popular press, the rate of return, after tax, increases with the rate of return, on a like-for-like comparison basis.

Comparatively speaking, you get a greater share of the returns on offer if you defer tax by seeking long-term capital growth and you seek higher rates of return.

That is the reality not the sensational headline.

Journalists do not risk regulatory action against any misleading statements. Licensed wealth advisors, like me, are obligated to be truthful.

Some journalists have claimed that these measures are harmful to start-ups.

Evidently, an investor will make more money if the tax rate is lower. However, they would also be wise to consider society to be their fellow traveler. Taxation funds government activity of all kinds, including pro-growth economic policy.

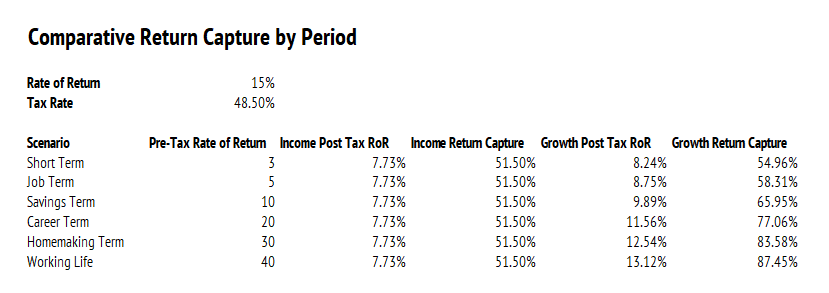

Wise entrepreneurs will consider the following pattern of post-tax rate of return:

The pre-tax rate of return assumption of 15% used to be the benchmark for Venture Capital. This is a four-fold increase of pre-tax capital over a ten-year period.

I will use that assumption as it has stood the test of time.

If you think I am unambitious, choose a higher rate and get a better result.

I have run scenarios at a top marginal tax rate of 48.5%, a pre-tax rate of return of 15%, and several holding periods stretching out to forty years.

Notice that the winning strategy is to hold investments for the long haul.

I am a professional wealth advisor, and I am licensed to dispense general advice.

Here is my general financial advice to anybody who pays attention:

Cut your losses when it is tax advantageous to do so and let your winners run.

I know that sounds like motherhood, but it is the truth of investment compounding.

Deferred tax payments on unrealized compounding gains are the winner.

This is so whenever you face a choice between equal prospective return. The caveat to that statement is comparable pre-tax return with all tax credits impounded.

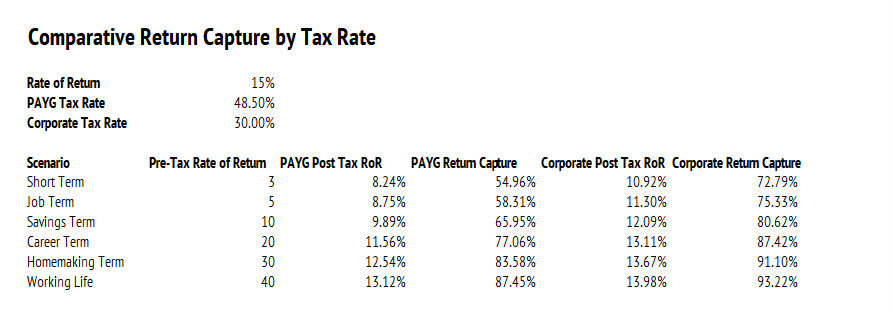

The Choice of Holding Structure Matters

I am not going to enter the field of personal and corporate structuring nor any advice on personal tax affairs. However, I can make one strong statement.

If you choose a structure where the compounding tax rate is lower you are better off. Corporate holding structures often have lower tax rates.

The standard example is the PAYG top marginal rate of 48.5% versus the 30% tax rate on a standard large company corporate tax rates for holding companies.

If you are young, and seek an entrepreneurial career, with numerous possible projects and exits it would be wise to consider holding company structures.

You can see the effect of this by comparing Australian PAYG tax rates at 48.5% versus the standard corporate tax rate of 30%. Holding a project in a company is better.

There are many who might take issue with this statement because money that is held in a company is not the same as money in your bank account. You would have to pay tax on money that you distributed from the company. That is true, but dividends in Australia have attached franking credits for any tax paid. You distribute that.

This is general advice only.

If you make a billion dollars, consider if you need that in your bank account.

Your personal holding company can buy assets and buy you lunch.

When doing your fringe-benefits tax consult a licensed tax adviser.

Australians love trusts and not holding companies.

I do not know why.

Why Trusts may not be Ideal for Entrepreneurs

I defer to the CoPilot AI on why it thinks trusts are sub-optimal.

Trusts are bad for:

raising external capital

issuing equity

retaining earnings

scaling

employee ownership

governance clarity

reinvestment discipline

They are not the structure used by:

US startups

European SMEs

Asian family conglomerates

Venture‑backed firms anywhere

Why? Because a trust is fundamentally a distribution vehicle, not a growth vehicle.

If you are a tax adviser who is paid to put your clients into trusts and you do not like the above statement then sue Microsoft, not me. CoPilot said that.

I am a mathematician and a licensed wealth advisor.

Tax deferral on capital gains is valuable.

Growth vs. Income Dominance

One of the advantages of being a mathematician is my holding a limited license for absolute truth. If the question hinges on pure mathematics, I can be absolute.

You will have spied the pattern, now let me make an absolute statement:

For the same (comparable) pre-tax rate of return R, invested over the same period of N years and subject to the same rate of tax T, on income or gains, the tax-defered investment strategy dominates the income-oriented strategy.

Obviously, the tax rate T has to be between 0% and 100%.

You also need a positive rate of return, or investing makes no sense!

If your tax rate T is greater than 100%, I suggest that you emigrate. If all prospective investments have a return R<0, then work for government.

Otherwise, you are good to go on your investment career!

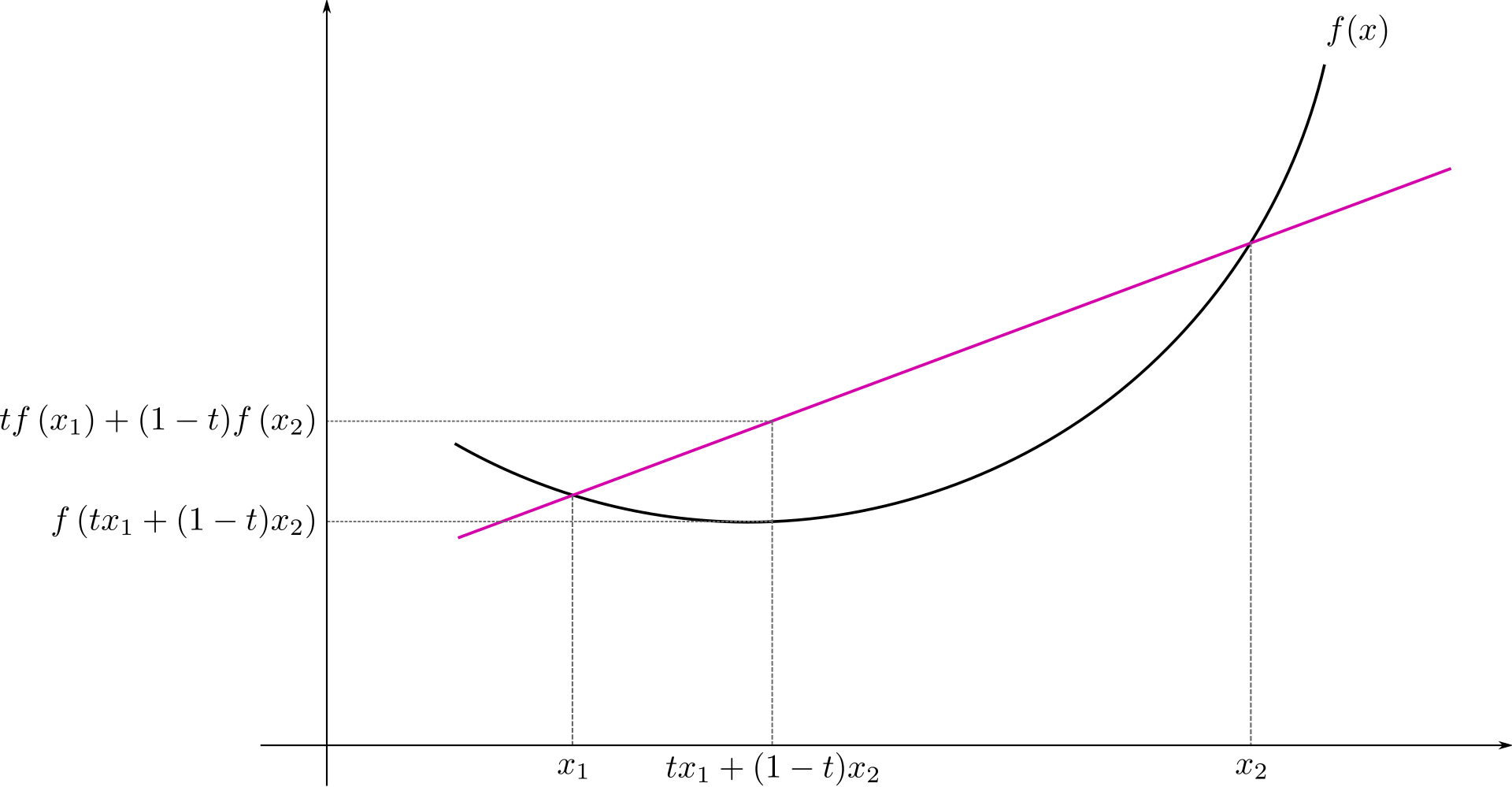

Let us prove the above statement, using my favorite, Jensen’s inequality. This is a very useful mathematical result that hinges on a simple idea. For any curve that is convex, meaning it uniformly bows downward, like that below, you can state that points on the straight line between the curve values at two points, are above that curve.

Specifically, the inequality means this:

The funny upside-down “A” is lazy mathematician speak “for all” and the [0,1] bit means the interval between 0 and 1, which would be 0% and 100% for tax rates.

You have to have a so-called “convex” function f, or it makes no sense, and is not a true statement. The function which is x to a positive power N>0 is convex.

Recall our post-tax growth rate of return:

and our post-tax income rate of return.

Not everybody likes mathematics, but I am not asking you to do it! If you concentrate on the visual pattern, you may spot the trick. Mr Jensen, through his inequality, tells us that the bigger quantity is always the left-hand side pattern, with the t’s outside f, and the smaller one has the t’s inside. The right side is dominated by the left side.

Choose this substitution into the Jensen inequality:

Voila! You did the math! Gorilla stamp. QED.

As long as you state clearly your caveats, ASIC cannot sue you.

What you have just seen for yourself is well-known in the finance industry.

Lots of quality superannuation funds in Australia will say this in words:

For equal pre-tax rate of return R, and tax rate T, the capital growth strategy of tax-deferral will dominate the returns generated by an income strategy.

This is not true of the financial press in Australia.

That is fine.

They are not quality wealth advisors.

Conclusion

To rap on the mad-cap theme of our Banana Splits financial media the race is called:

Bingo (The Gorilla) – 1st Place - pure capital growth with no dividend

Fleegle (The Beagle) – 2nd Place - capital growth with dividends reinvested

Snorky (The Elephant) – 3rd Place - tax-deferred income via discount bonds

Drooper (The Lion) – 4th Place (Last) - pure income with no tax deferred

Notice that is for the exact same pre-tax rate of return R, and tax rate T. There can be differences in tax credits, and even tax rates, so you need to consider that.

Large sections of the Australian finance industry are compensated for advice on tax minimization and the accumulation of debt to reduce personal tax obligations.

They may have different ideas.

I am a licensed wealth advisor who is focused on the best after-tax rate of return.

You may pay more tax, over time, to our government, choosing growth, but you will also be richer. Greater post-tax returns are my area of focus.

That is the general advice on offer today.

Oh, and here is the spreadsheet I used for those case studies.

Happy investing!