Who was bought and by whom?

There has been a notable conspiracy of silence about the true nature and extent of US Critical Minerals demand. I illustrate with Rare Earths. This story is disturbing.

To anybody who follows the minerals industry over time, there has been a persistent and perplexing torrent of interest in Critical Minerals, which is backed by very little evidence regarding the true nature of the Supply and Demand equation.

To save readers trouble, I will state my conclusion at the outset.

Western demand for Rare Earths, in material form, is de minimis.

That is some fancy Latin to fool journalists that you are not publicly dissing them :-)

It is therefore fitting that, absent any knowledge of their subject, and armed with righteous indignation at “What China just did.” or “What China didn’t do.” the journalist community will reach for the obligatory Wikipedia money shot.

{kind=link}

There will follow a long meandering discussion about how the USA “used to be” the leader in global Rare Earths mining, separation, and downstream value-added.

This was a long time ago.

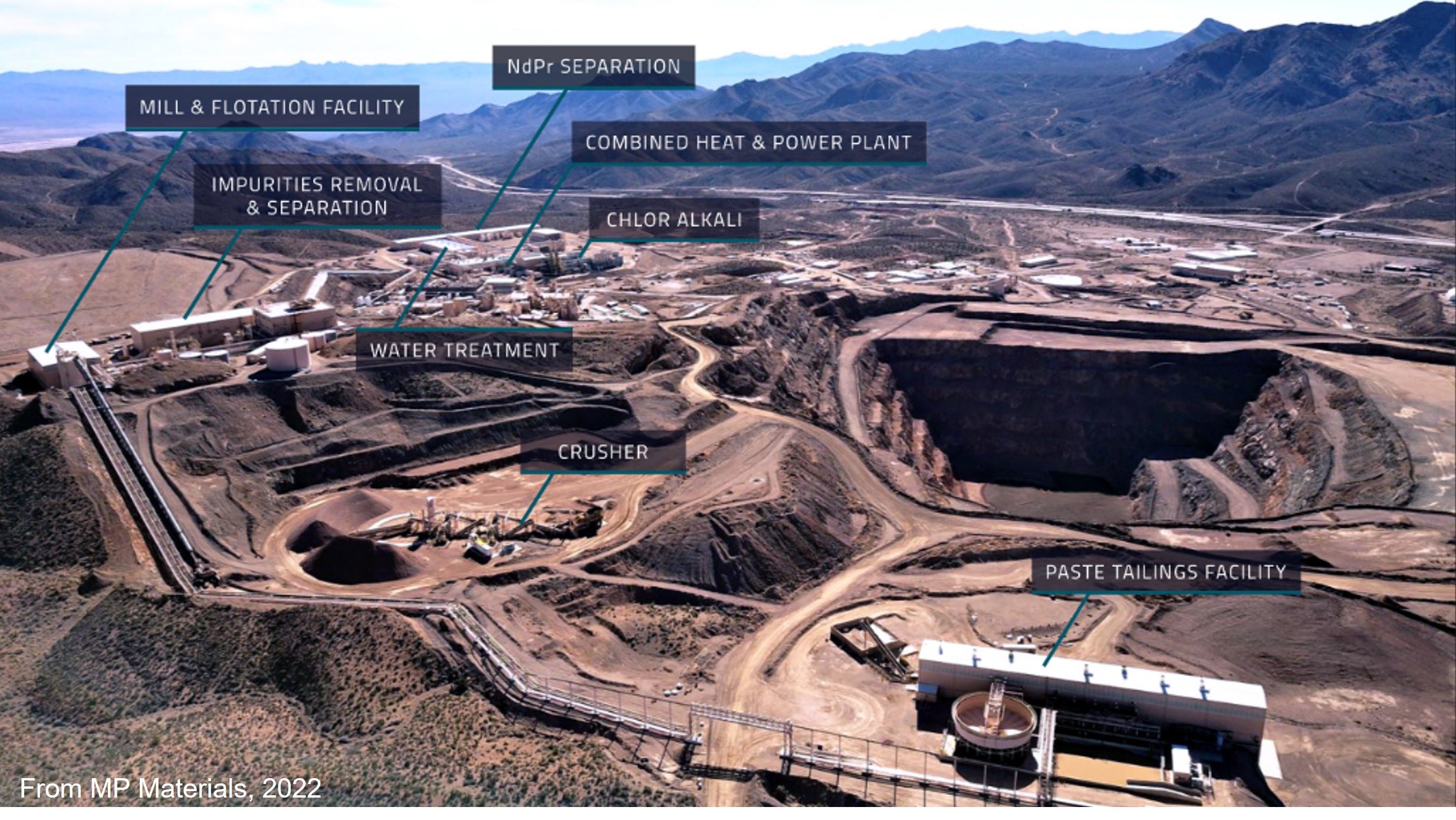

The story of Mountain Pass, the US Rare Earths mine in California will be told and retold with great emphasis on “What China did.” to hamper its progress.

Throughout these diatribes, no mention will be made that the Chinese firm Shenghe Resources helped fund the mine restart when the US Department of Defense (DoD) was invited by the Administrators of that, the third bankruptcy, to help fund it.

This year, more than eight years later, the US Department of Defense decided to spend far more than it would have at the bankruptcy auction to buy a stake in the operating company, MP Materials, that now owns and operates Mountain Pass.

I know all of this because I was a shareholder in Molycorp, the forerunner of the new entity MP Materials, before, up to, and including the third bankruptcy.

I was an institutional shareholder who had first bought stock in the IPO, and then later bought stock in the after-market, on my own account. I believed in the story, because Rare Earths are important in the global economy. I still believe in Rare Earths.

However, the other thing I believed in was the power of then management, who were from North America, to properly manage and execute their plans for that mine.

Molycorp management failed in this endeavor and the company went broke.

Contrary to the popular wisdom about China and Rare Earths, and how evil the place may be, the Molycorp mine failed because overly high rare earth prices crashed.

How do I know that?

I was invested in the market, professionally, during the 2010-2011 “Rare Earth Crisis”.

Since I was working as a global portfolio manager for an Australian investment bank my team was in close contact with the Japanese institutional investor market.

I got the call to go develop a Rare Metals Investment Strategy back in 2010-2011 when the Japanese were very concerned about a Rare Earth embargo.

Not knowing what the Japanese intended with the phrase “Rare Metals” I looked it up and then bought the industry Bible the Rare Metals Handbook (1961).

It had been so long that any investor had looked at this sector that I could pick up a remaindered as new copy in original shrink warp for $20 USD.

I still have that copy but might sell it now for $250 USD.

That is the going rate.

The book is old, and I read it.

Looking around me, and reading the newspaper, it is clear that very few have.

The Rare Earth Market

How can I state with abandon that Molycorp went broke because prices crashed?

Simple, I and every other investor in the name had bought into the story when prices had skyrocketed due to the Chinese embargo of Rare Earth exports. The effect on the market was immediate outside of China, and actually bad within China also.

Export quotas were imposed by China to limit legal exports from Chinese ports. This placed a premium on any material that had cleared Chinese customs, which could be sold into global markets at a Free-on-Board (FOB) price. The price of that material went Moonshot, while non-cleared material sold at lower Ex-Works (ExW) prices.

Whereas the normal price differential within China is small between FOB and ExW, the quota system saw the price blow out. The normal price spread would be insurance and freight, which are paid to bring material ExW to the port as FOB. However, as is evident with US trade sanctions on NVIDIA GPU exports, arbitrary rules on who can and who cannot buy a product will soon destroy the law of one price.

Market interference of this kind destroys the normal equilibration mechanism for supply and demand in the marketplace. The result was a flourishing black market sending cheaper ExW material for illicit export from Hong Kong, sold as FOB.

The same thing happens now with NVIDIA GPUs headed for China.

While this produced boom times outside of China, being particularly good for any rare earth mineral explorer that wanted to raise capital, it was not healthy for the market. While you may read a lot about what China did, with the embargo, you will not read much about why they stopped, aside from a 2014 WTO ruling. The World Trade Organization found against China and ordered the embargo stopped.

China obliged, and reopened trade for good reason.

The exercise was a failure because the high prices killed market demand.

The resulting normalization of prices, to restimulate market demand, then killed the Molycorp mine, in that incarnation, because it could not serve growing demand at lower prices once the demand destruction of higher prices abated.

These may seem like confident assertions on a complex topic.

They are because I can lay claim to knowing something about my subject matter.

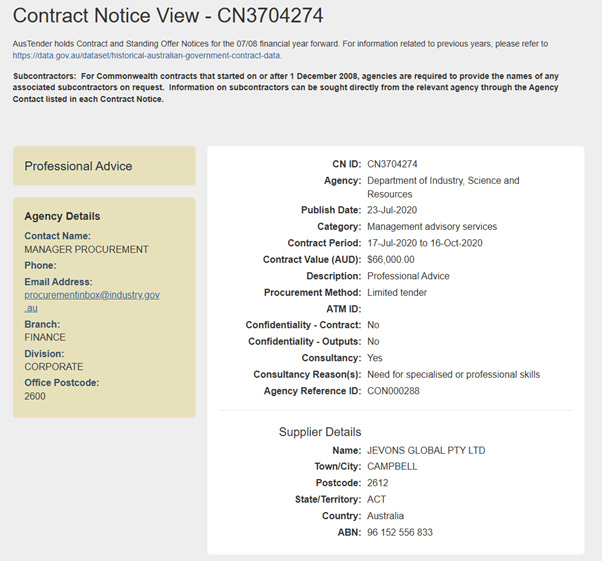

In mid-2020, my firm won a limited tender to advise the Australian Government.

This is a matter of public record.

The report on the Rare Earth Supply Chain which I prepared in fulfillment of that tender is not publicly available. However, I know it because I wrote it :-)

In fairness to the Australian Government the whole report was never publicly released because it contained both recommendations on policy and company discussion.

It is appropriate that some advice to government be kept in camera.

However, the bulk of the material in my report was market and supply chain analysis which is neither commercial-in-confidence nor policy sensitive.

I secured agreement to release a redacted version with any sensitive material removed.

You can read that redacted report below.

You can also read my earlier analysis of FOB versus ExW pricing here:

These are dry topics.

The reason I share this detail is to back up a simple case I have made for years.

The problem for the West is a lack of Rare Earth demand not a lack of supply.

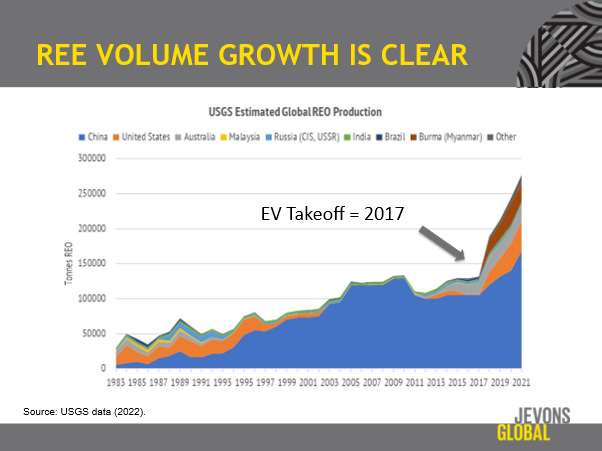

Let us deal with supply first. Growth of Rare Earth Supply has been ample.

Some complain about Chinese control of Rare Earth mines.

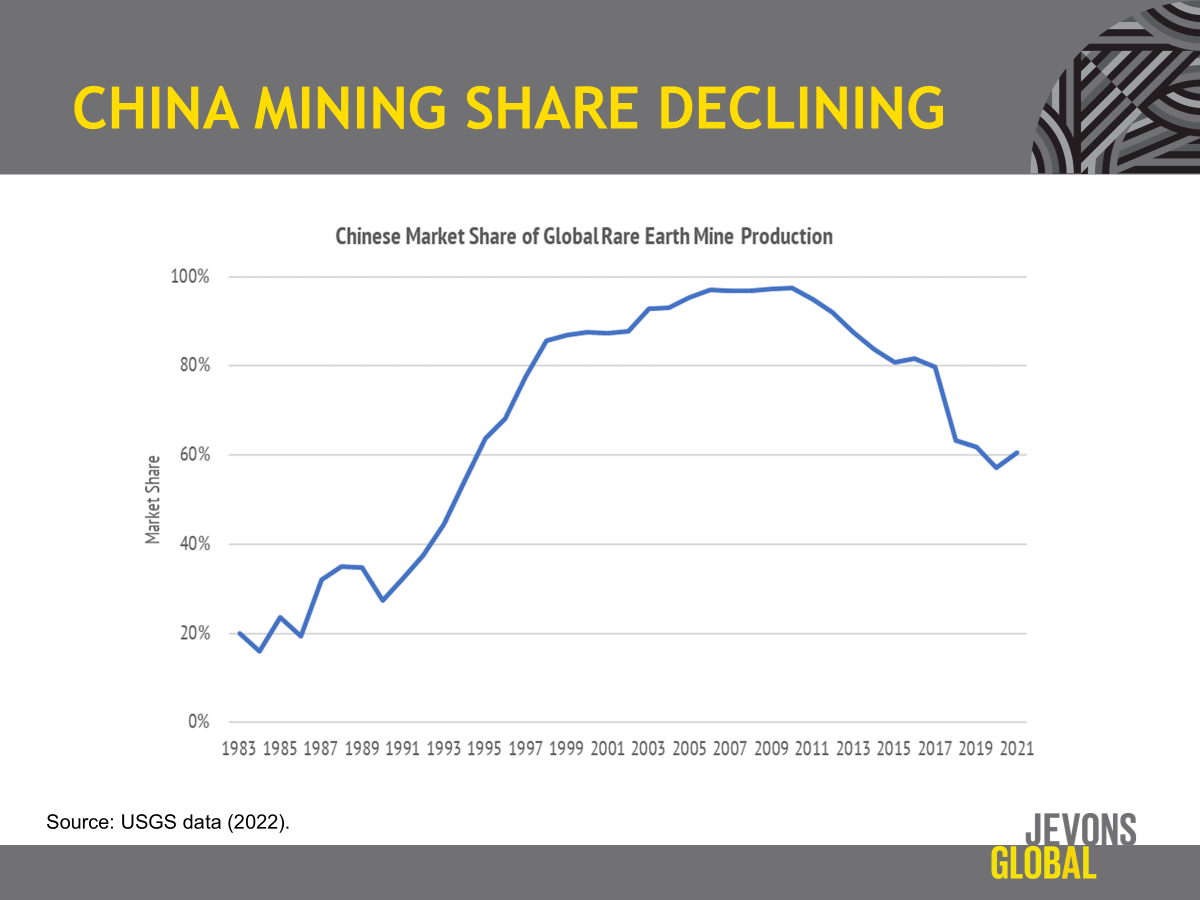

This may have been a fair criticism in the period 2000 to 2011, but not so now. Mining in China has lost share over the past fifteen years to about 60%. The gainers in share were originally places like Australia and Myanmar but are now the USA and Africa.

It may surprise you to know that the USA is the largest exporter to China!

You read that correctly.

In spite of the many column inches spent lambasting China for their control of the global Rare Earth industry, that nation imports almost all output from the USA!

Given this fact you can appreciate why the subject is so sensitive.

The USA would have us believe that China is withholding vital Rare Earths from them when the country is the largest global exporter of rare earth concentrate to China.

It is the same mine as before, Mountain Pass, now under better management.

The reason for this odd situation is that the USA has only a nascent magnet industry but a significant, albeit shrinking, catalytic cracking industry. The high value Rare Earth elements, like Neodymium, Praseodymium, Dysprosium and Terbium supply manufacture of Rare Earth Iron Boron (NdFeB) magnets.

These are the items in demand for Electric Vehicles, robots and industrial motors.

The low value Rare Earths are Lanthanum and Cerium. These are more abundant and produced in greater quantity by rare earth mining operations. Their prices are around $2USD/kg versus $40-80/kg for Neodymium and Praseodymium, $400/kg for the Dysprosium products, and upwards of $1000/kg for Terbium.

It is the magnets that are valuable, and the USA hardly produces any.

The original Molycorp operations at Mountain Pass failed around 2014 because the high prices of the 2010-2011 Rare Earth Crisis normalized. The company had spent money trying to develop a Mine-to-Magnet Strategy but invested too much in an obsolete magnet process known as bonded magnets. The real market was in the higher performing sintered magnets.

The global sintered magnet market is centered in China (90%) and Japan (10%).

Fast forward until today, and the Mountain Pass operation is back in business, better run and selling most all of the product to China. Unlike before, the new entity has a more developed plan to make sintered magnets at their recently constructed Texas facility named “Independence” at Fort Worth, in Texas.

This is a small factory by world standards.

It will be producing around 1,000 tonnes annually of magnets, which is the equivalent of perhaps 300 tonnes per annum of Neodymium and Praseodymium demand.

The global market for magnets is estimated to be 200,000+ tonnes per annum.

US magnet imports, mostly from China and Japan, are about 9,000 tonnes per annum.

Contrary to popular belief, almost none of that is military demand.

What about Military Demand?

The role of Rare Earths in weapons system has been oft repeated, but it is not a very good thing to focus on if you want to build an industry. The numbers are too small.

US Military demand is probably less than 500 tonnes per annum.

Nobody will say exactly how much, but I have a fair idea based on my own analysis of public sources, and my understanding of modern weapons systems.

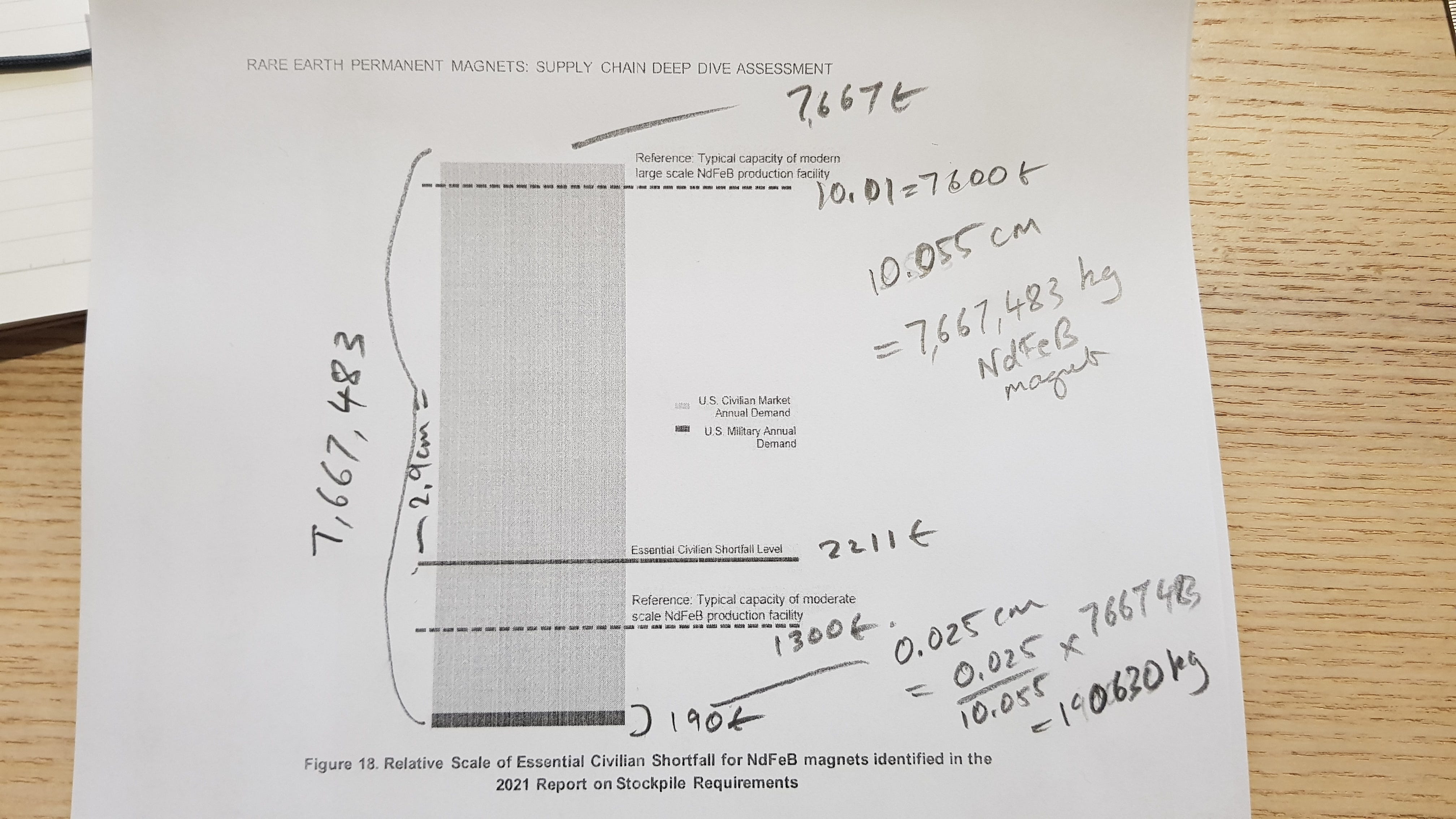

The best estimate of US Military demand that I could come by was 190Mt per annum.

I used a steel ruler on a diagram of the US Department of Energy (DoE) public report: Rare Earth Permanent Magnet Factory Supply Chain Deep Dive. This is from Figure 18 on p. 38 of the report, which is introduced with this text (prior p. 37):

NdFeB requirements were assessed in the 2021 Report on Stockpile Requirements. The quantified findings of the assessment are restricted, but Figure 18 helps shed some light on key facts for NdFeB magnets required for essential civilian and military applications. Source: DOE REPM Supply Chain Deep Dive, 24-Feb-2022.

The requirements are restricted, but we can estimate the military demand number.

Using the scale of known demand in the reference year (7667 tonnes), the military number can be estimated at about 190 tonnes. This is 0.1% of global demand.

It does matter to the US DoD, as they keep saying publicly.

The F-35, for instance, requires more than 900 pounds of rare earth elements. Each Arleigh Burke DDG-51 destroyer requires 5,200 pounds, and a Virginia class submarine needs 9,200 pounds. Source: DOD News, 11-Mar-24

Okay, so 9,200 pounds per Virgina Submarine sounds like a lot.

In reality units, that is 4,181 kg.

In a good year, the USA produces two Virginia Class submarines.

That is 8,362 kg of Rare Earths, around 8.3/200,000 x 100 = 0.004% of global demand.

We can now understand why we are wasting so much policy effort on this problem.

Don’t get me started on the Arleigh Burke DDG-51 destroyers. Having read the very entertaining US Government Audit Office GAO Report GAO-27-79R, with the catchy title Observations on the Navy's Hybrid Electric Drive Program, I think that all future think tank slides should contain this text:

Every Arleigh Burke DDG-51 destroyer whose name happens to be USS Truxtun may have required 5,200 pounds of rare earths to make the revolutionary Hybrid Electric-Drive System, but we don’t know.

There only appears to be one such ship because it did not work very well.

The fact of whether any rare earths were used at all remains in doubt because the U.S. Navy will not tell us, and the GAO has established that the early prototype motor was unavailable when needed so they went with a different design.

We do know there is one working system in a ship and as many as thirty others sitting in a warehouse somewhere waiting for the U.S. Navy to find a use for them.

The Growing Share of US Rare Earth Mining

There is nothing wrong with the USA trying to rebuild their rare earth industry. Diverse supply is a good thing. The problem is the approach.

While the USA has been happily selling Rare Earths to China, so as to fund the restart of Mountain Pass, and to seed the domestic supply chain, there has been relentless pressure on Australian miners to stop selling Rare Earths to China.

One is reminded of the famous couplet from George Orwell’s novel Animal Farm.

"Four legs good, two legs bad" - Snowball, Chapter III

"Four legs good, two legs better!" - Squealer, Chapter X

Propaganda is like that.

Australia selling Rare Earths to China is bad.

The USA selling Rare Earths to China is better.

Australians seem to have happily obliged in chanting with the sheep of Animal Farm.

Here is a statement from the MP Materials 10-K Annual Report from 28-Feb-2025.

Sellers are rare earth mining operations producing a mineral concentrate. At present, the only known significant mining operation supplying this market outside of China is MP Materials’ Mountain Pass and, with the exception of emerging byproduct monazite producers, this is not expected to change in the near-term.

Source: MP Materials 10-K 28-Feb-25

The line about monazite producers refers to mineral sand producers. These exist in many countries around the world, the USA, India, Australia and others.

The key statement is this one:

At present, global NdFeB magnet and magnetic alloy production is dominated by China, with emerging growth underway in the U.S. and Europe. Major Chinese magnet producers (and thus buyers of PrNd) include JL-Mag, Beijing Zhong Ke San Huan Hi-Tech, Tianhe Magnets and Ningbo Yunsheng. Collectively, Chinese magnet production makes up approximately 90% of global supply with Japan host to nearly all the rest. Major magnet producers outside of China include Proterial, Shin-Etsu Chemical, TDK, all in Japan, and Vacuumschmelze, located in Germany. Emerging producers in the U.S. and Europe include MP Materials, Noveon, and Neo Performance Materials.

Source: MP Materials 10-K 28-Feb-25

This statement is reasonably accurate. The Japanese share may be overstated and the Chinese share understated, but between them they dominate the global market.

The demand for Rare Earths to manufacture high-value products is concentrated in the global magnet industry and that is dominated by China and Japan.

The construction of more Rare Earth mines does nothing to change the picture on how and where magnets are made. That is overwhelmingly China and Japan.

Why Australia should stop selling Rare Earths to China to help the USA sell more Rare Earths to China is beyond me. It makes absolutely no policy sense whatsoever.

I have said as much to the Australian Government.

That is what expert advice is for.

The Shrinking Share of Australian Mining

Let us now examine the effect of these policies.

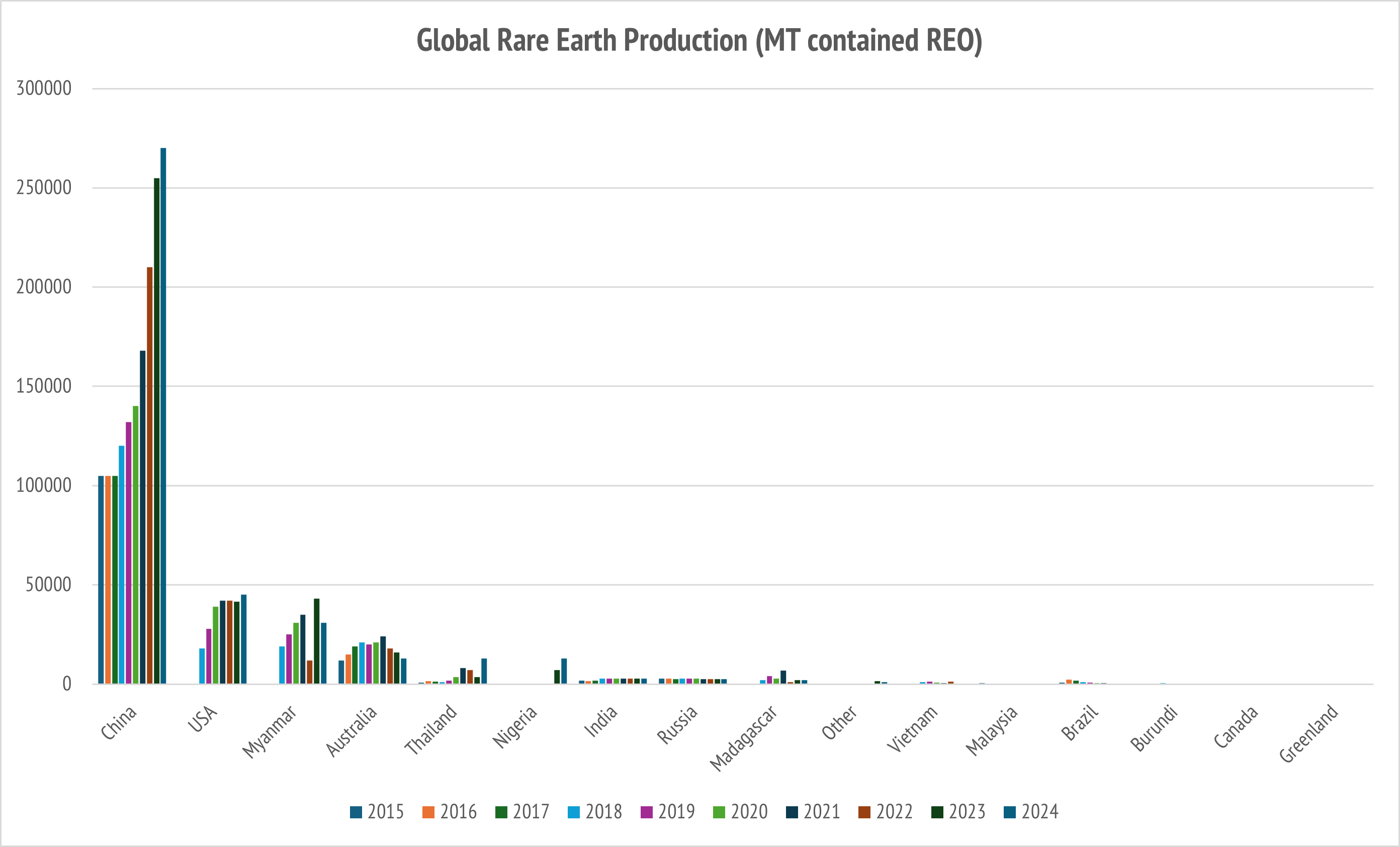

Shown below is ten years of global production data sourced from the US Geological Survey Mineral Commodity Summaries Series. The 2024 production data is here.

Notice that over the last ten years, China has grown consistently, the USA reentered the global market to become number two, Myanmar grew at number three, and Australia grew, then stalled, and has now shrunk to number five after Thailand.

This is Australian Government Rare Earth Policy at work.

There have been plenty of eager mining startups that have raised hundreds of millions of dollars in capital and found plenty of new resources. However, essentially no effort went into magnet factories, and so Western demand remains weak.

I correctly anticipated this problem in my advice to Government.

I am just a humble finance guy and investor. The one thing I know about mines is that they are hard to finance if there is no visible buyer for the product.

The process of lining up buyers is called securing offtake.

The Australian Government did listen to some of my advice, concerning the suitability of Eneabba sourced material for an appropriately sized Rare Earth Refinery.

However, they do not appear to have listened closely to my advice about offtake.

Let us see what happens, but there is talk of taxpayers funding a stockpile.

This will help fund the purchase of Rare Earths that nobody else wants. The reason that they don’t want them is because they do not operate magnet factories and therefore have no need for high value Neodymium and Praseodymium.

Japan does want some, but its order book is full of supply from Lynas.

China does want them, and will pay for them, but Australia does not want to sell any to China. This is the job of Americans. They sell to China from Mountain Pass!

Australian policy said no to the buyer which constitutes 90% of the global market, namely China, and sold to the 10% of the global market represented by Japan.

US policy said yes and sold 100% of their production to 90% of the global market, that is China and ignored the 10% of the global market that is Japan.

American policy worked extremely well.

Australians were dumb enough to listen to Americans and follow their earnest advice to not sell any Rare Earths to China. This was the growth market that the USA filled.

Chinese demand grew rapidly because of their adoption of Electric Vehicles.

Japanese demand grew slowly because Toyota preferred Hybrid Vehicles.

The result of this policy difference between Australia and the USA is very clear. The USA has taken the number two spot from Australia, and we slipped to number five. This is your government hard at work for you spending taxpayer dollars!

You cannot really blame America for this outcome.

They worked in their own interest and found many Australians working for them!

The Outcome of Australian Policy

It may seem churlish to openly and publicly criticize the very government that paid your firm to deliver expert advice on the Global Rare Earth Supply Chain.

This is definitely an unusual situation.

Consultants must be cautious in biting the hand that feeds them.

However, I am also an Australian Citizen, and I care greatly when my government chooses to preference the interests of another nation over those of Australia.

This irks me.

It makes me angry.

It makes me want to do something constructive to rectify the evident damage.

In the past, I was content to publish informational research pieces in the (vain) hope that the Australian press might pay attention and put the National Interest first.

Here is the fossil record of such activity:

Where do the separated rare earths by Lynas actually go?

Gross Mineral Product (GMP) as a tool for sizing the global critical minerals economy

The hazards of groupthink in rare earths policy-making

Which country is the largest exporter of unseparated rare earth concentrates to China?

Needless to say, none of that has had any effect at all.

The Australian press continues to be “All the way with the Blessed USA.”

There does not seem to be any serious effort at all to understand this market.

Let us survey the national damage that has resulted from this nonchalant ambivalence.

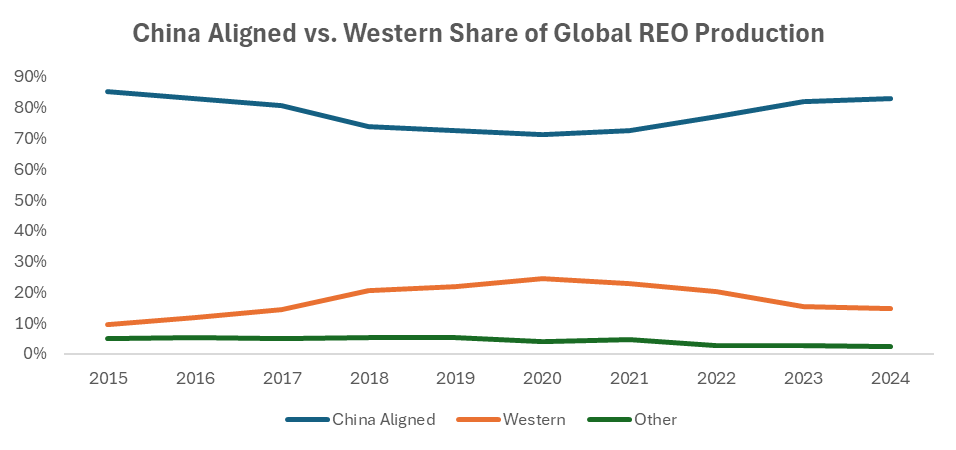

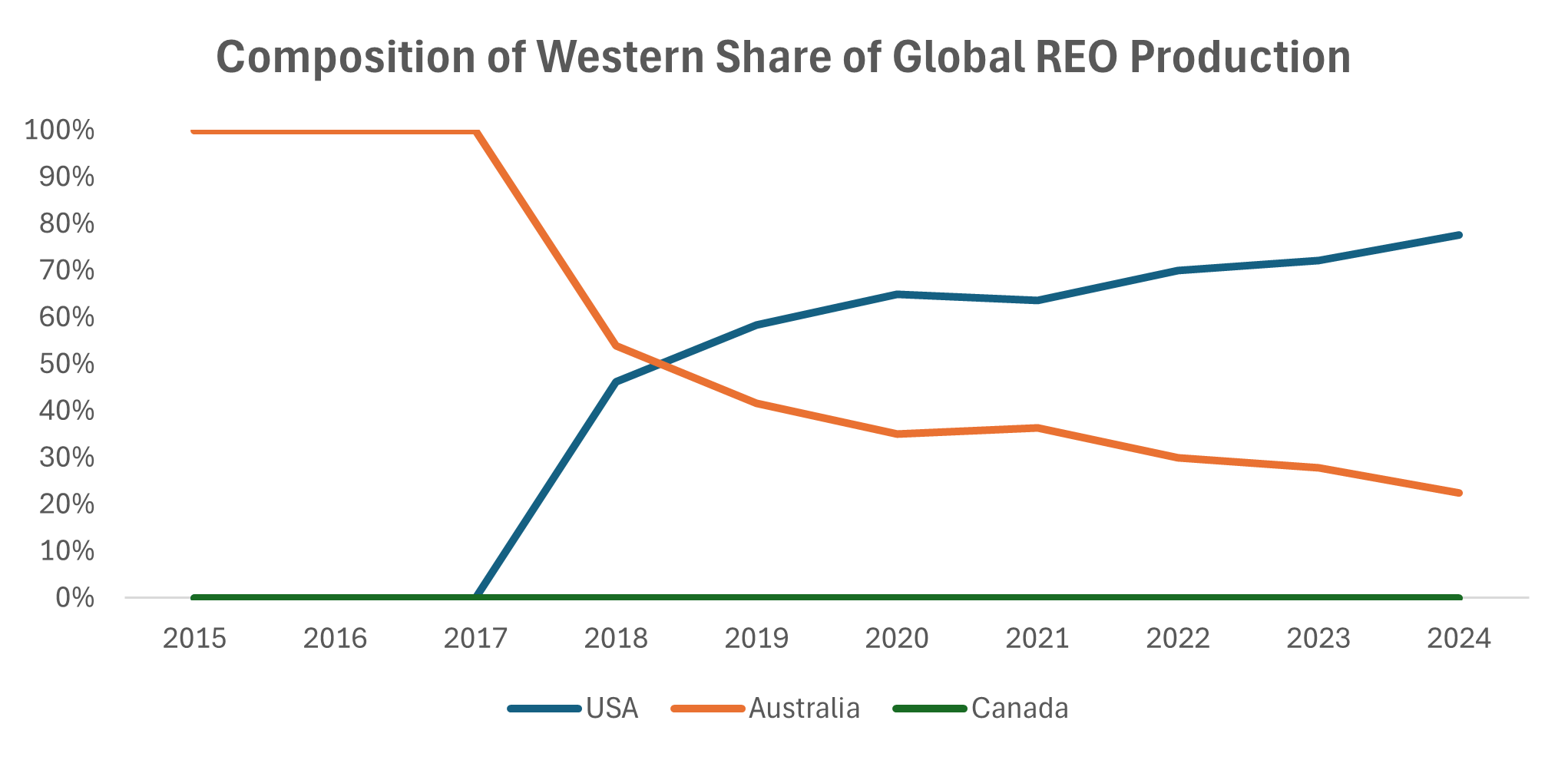

Using USGS data, I have compiled a global market share split on geopolitical lines.

Among global producers, I created a “China Aligned” grouping of China, Myanmar, Thailand and Nigeria. This reflects sources which are mostly going to China.

I do not strictly mean politically aligned with China; I mean supply-chain aligned.

For instance, Thailand is not really politically aligned with China but has shown some rapid growth in Rare Earth production. Some of this is probably from Myanmar.

Then I created a Western group which is the USA, Australia and Canada.

The Other is everybody else, which includes stable producers of modest quantities such as Brazil, India and Russia. This is often used internally.

Whatever your geopolitical orientation it ought to be clear from the above chart that Western policy has not been successful in growing Western market share.

It peaked around the year 2020 when Australia began to get serious about Rare Earths by forming a dedicated Critical Minerals Facilitation Office (CMFO). This initiative began under the Morrison Government, now the CMO under Albanese.

I remember thinking it was rather odd that the CMFO Supply Chain discussions I had in 2020, when doing my report for them, were heavily focused on the USA.

I obliged my client in such discussion but assured them that US demand was small. Why the Australian Government should spend so much policy effort on trying to sell Rare Earths to the USA, when they were our biggest export competitor made little sense to this consultant. However, the customer is always right.

At that time, I did not realize that there was only one working Hybrid-Drive Electric Ship in the US Navy. I suggested they talk to the Americans about electrifying the light combat vehicle fleet with something like an Electric Humvee.

Needless to say, I did not comprehend the real game at work.

Here is the real game that was being played.

With the benefit of hindsight, and recent DoD investment in MP Materials, the game plan has now become clear to anybody with two eyes and a working brain.

The Western global market share of Rare Earth production declined since 2020.

However, the USA won major market share from Australia.

Canada stayed on their own personal road to nowhere.

The Morrison Government establishment of the CMFO was a splendid success!

The (unstated) policy objective was achieved.

Australia was hobbled.