Will we witness a Petrodollar Liquidation?

The Gulf States depend on oil exports for a slice of government revenue. The challenge is to estimate how much revenue from volume losses can be made up from higher prices.

There is too much uncertainty right now to be a hero and forecast the outcome.

However, following the wild action in precious metals markets we have to ask the obvious question: Why is the US bond market so quiet with this huge shock?

Look at gold, via COMEX futures. It is up 1.97% year to date but has swung like crazy.

The same goes for crude oil, although the direction of trade makes more sense.

While the United States is a net exporter of fossil fuels domestic gasoline is surging.

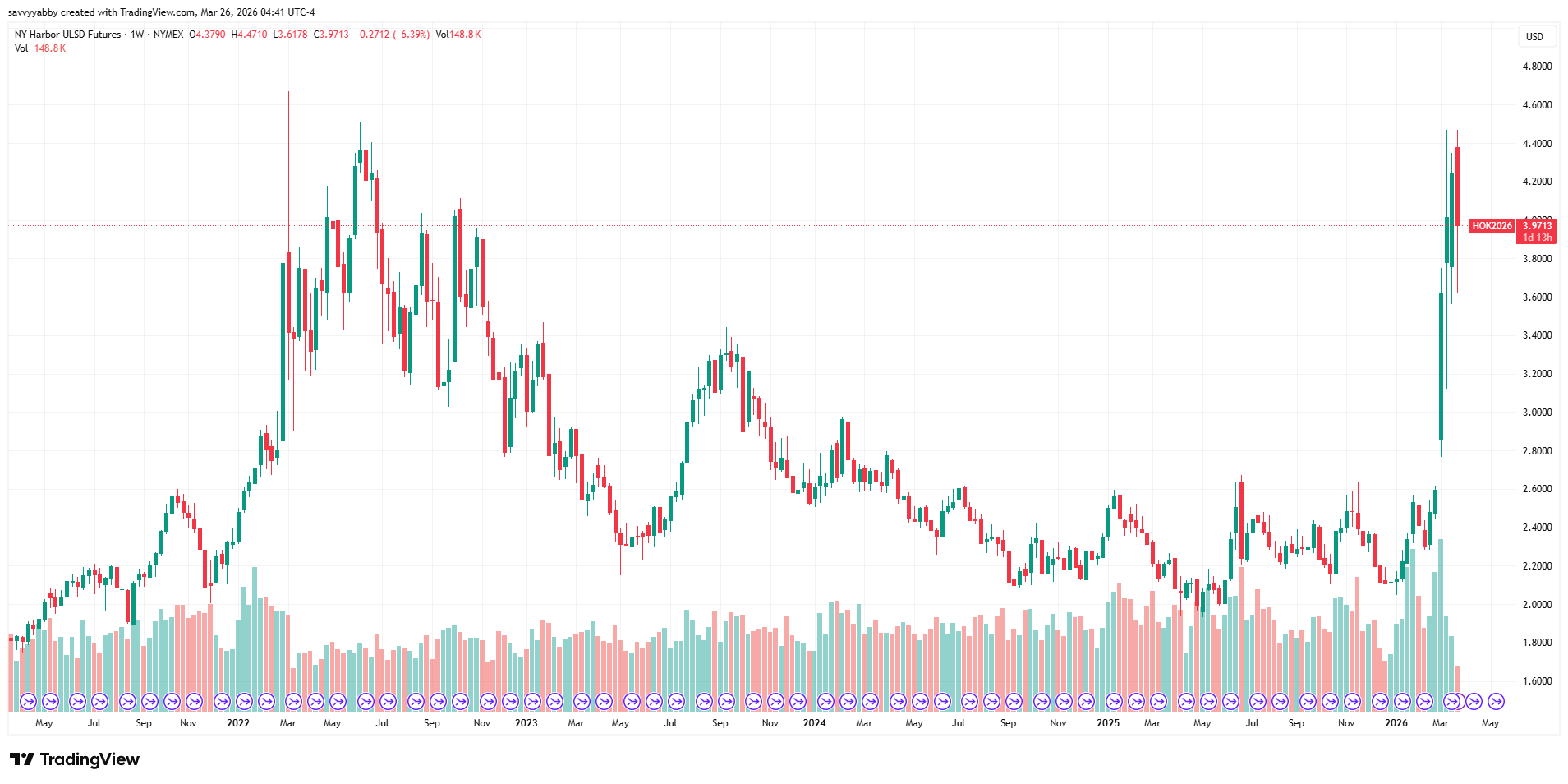

The supposed immunity of the USA to this energy shock applies even less to diesel.

To find some relative peace and quiet you have to go the US bond market.

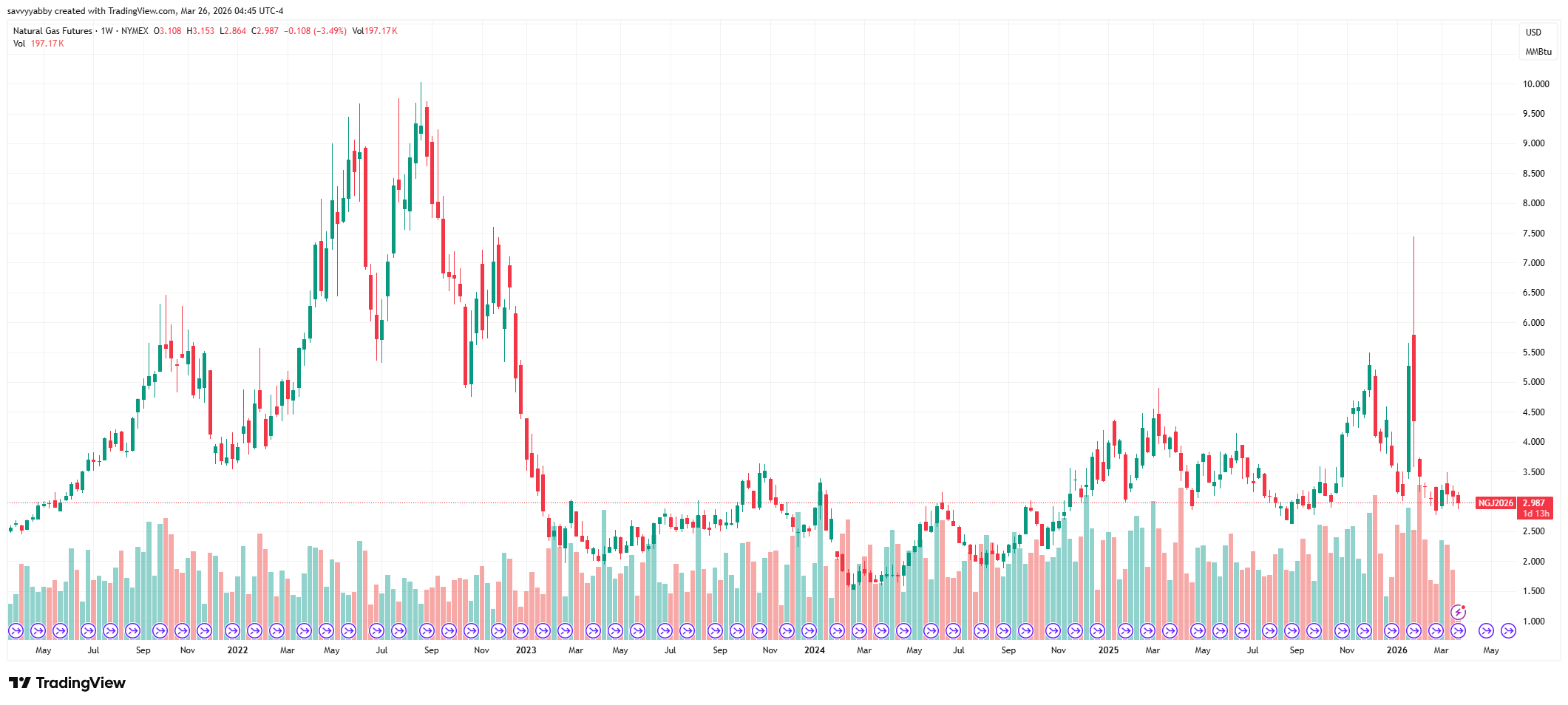

The other quiet place has been New York Henry Hub gas futures.

Is this the calm before the storm?

Certainly, the USA is self-sufficient in energy, so it appears immune from this global energy crisis. Certainly, the Trump Administration is behaving as though it has total impunity to do whatever it pleases with this war on Iran, in the Gulf.

However, the supply shock looks huge by any measure.

Oil share from Persian Gulf

~20% of global oil supply comes from the Persian Gulf.

~21–25% of global seaborne oil trade transits the Strait of Hormuz.

Current disruption

At least 10 million b/d of Gulf production shut in, per IEA—over half of normal Hormuz‑transiting crude.

Effective global supply loss: ~10–12% of world supply.

Natural gas share from Persian Gulf

~20% of global LNG supply passes through Hormuz.

Qatar alone supplies ~20–21% of global LNG.

Current disruption

Global LNG supply down ~20% since the conflict began.

Qatar’s Ras Laffan and Mesaieed facilities suffered missile damage; multi‑year recovery expected for some trains.

Urea share from Persian Gulf

The Middle East (Qatar, Saudi Arabia, Oman, UAE, Bahrain) accounts for ~30–35% of globally traded urea.

Current disruption

Qatar Energy halted LNG and associated products, shutting QAFCO’s 5.6 Mt/yr urea plant—one of the world’s largest.

If disruptions persist beyond two weeks, CRU warns of meaningful regional supply loss for March and potentially beyond.

Sulfur share from Persian Gulf

The Gulf is one of the world’s largest sulfur exporters, contributing ~35–40% of global elemental sulfur trade (industry consensus; IEA notes it as a “vital artery”).

Current disruption

IEA confirms sulfur trade is “interrupted” due to damaged energy and petrochemical infrastructure and halted shipping.

Helium share from Persian Gulf

Qatar supplies ~30% of global helium (Helium 1, 2, 3 plants at Ras Laffan).

Nearly all Qatari helium exports must transit Hormuz.

Current disruption

IEA confirms helium trade is “interrupted”.

Damage to Qatar’s LNG infrastructure directly affects helium extraction (helium is a by‑product of LNG processing).

Other petrochemicals share from Persian Gulf

The Gulf is a major global exporter of:

Ammonia (Saudi Arabia, Qatar, Oman)

Methanol (Saudi Arabia, Iran)

NGLs & condensate (Qatar, UAE)

These collectively represent 20–30% of global seaborne petrochemical feedstocks.

Current disruption

IEA: Petrochemical trade flows are interrupted, with >40 regional energy assets “severely damaged.”

The Gulf States Budget Hole

Numerous analysts and strategists are adding this up with the petrodollar equation.

The petrodollar circuit refers to the money-go-round mechanism by which oil is sold for US dollars, under an arrangement negotiated between Saudi Arabia and the USA after the first OPEC Oil Embargo and the savage bear market of 1974-1975.

In return, Saudi Arabia recycled dollars from oil into purchases of US Treasury Bonds and defense equipment under a security guarantee from the United States.

This arrangement has been under increasing pressure due to the rise of BRICS, and the move for dedollarization that accelerated following the Western seizure of gold and foreign currency reserves ($300 - 355B USD), from Russia’s foreign central bank holdings in the aftermath of the Russian invasion of Ukraine.

This event kicked off the current gold bull market.

Lately, precious metals have been coming under immense pressure, but the US bond market has been comparatively quiet. There is doubtless some liquidity driven sales of gold by hedge funds, Commodity Trading Advisors (CTA), and other speculators.

However, the market is beginning to (quietly) discuss another reason.

With 10 million barrels a day of Gulf crude oil production shut in that is around $600 to $700 million a day of collective lost revenue. This directly impacts revenues that fund governments in the Middle East.

This is the revenue that would have been earned under normal conditions.

The counter-factual revenue foregone (which would have been there normally) is:

10 million barrels/day × $60–70 Brent (pre‑war)

= $600–700 million/day of foregone revenue

= $18–21 billion/month

= $220–255 billion/year if the outage persists

This is a lot of cash to find in a crisis, some private, some public.

The Gulf states are not just losing barrels — they are losing:

Budgetary stability

Forward‑sold hedges

Long‑term contracts

Market share

Refinery utilisation alignment

Downstream integration flows

Petrochemical feedstock continuity

These are not offset by higher spot prices.

This is why the IEA, OPEC+, and sovereign wealth funds treat volume loss as more damaging than price volatility.

The curious feature of this crisis is the volume loss may be made up for by the rise in prices for what production remains. The 10 million b/d of Gulf oil production shut in amounts to about half of the total, now sold at $100/barrel. That is about $400m per day of extra revenue to plug some of the gap of $600-700m per day that was lost.

This would convert the Gulf budget hole to:

$100–300 million per day

≈ $36–110 billion per year

This is the number governments actually need to plug with:

Sovereign Wealth Fund (SWF) drawdowns

New government borrowing

Funding gold swaps

Infrastructure project deferrals

Not the full $600–700m/day.

The Gulf Sovereign Wealth Funds

Gulf governments have:

Saudi PIF: $900B+

UAE ADIA/ADQ/Mubadala: $1.5T+

Qatar QIA: $500B+

Kuwait KIA: $800B+

Short‑term revenue losses do not immediately impair fiscal capacity.

This rainy-day fund, along with central bank holdings of gold and foreign currency assets like US Treasury bonds could sustain the GCC states for some time.

Realistically, they might last 2-5 years under pressure, although the knock-on effects of this war on tourism, finance, and real estate, would multiply the damage.

The position for Iran is unknown, but they have been sanctioned for many decades and likely have reserves of their own that they can access.

Petrodollar Liquidation Unlikely

At this stage of the war, it seems unlikely we will see a large scale forced liquidation of common reserve assets like gold and US Treasuries. However, the lack of fresh dollars earned from trade is likely to diminish buying power at the margin.

We may already have witnessed this effect, at the margin, in the gold market.

There are two data sources to monitor globally:

Treasury International Capital (TIC) System

World Gold Council Central Bank Gold Statistics

The first shows month foreign holdings of US Treasury Securities by country.

The second has data on central bank purchases and sales of gold.

Monthly reported central banks activity, tonnes*

Note that the pace of central bank net buying dipped in the last part of 2025, likely due to the run in gold in the last quarter. The data for this month may well show a negative dip, like the period around April 2023.

At this stage, we think the liquidity call on gold is temporary and likely related to too much leveraged positioning in precious metals going into the recent blow off.

Nonetheless, we should monitor the situation closely.

For a timely discussion of this point see What Iran means for the dollar: a perfect storm for the petrodollar, by Deutsche Bank strategist Mallika Sachdeva.

Conclusion

It is noteworthy that major investment banks, like Deutsche Bank, are beginning to consider the possibility of a petrodollar crisis resulting from the Iranian de-facto blockade of the Strait-of-Hormuz through threats to sink unfriendly ships.

There is significant geopolitical leverage to offer unimpeded passage to ships that declare their cargoes to be destined for “friendly” nations paid for in yuan.

This could be an inversion of the deal the USA and Saudi Arabia struck to end the first oil crisis. The irony would not be lost on anyone if a petroyuan market were to rise from the ashes of this crisis, with the implied security guarantees.

This war began on the premise that it was about an alleged Iranian nuclear program.

It may end with a new monetary system bifurcated on US dollars versus Chinese yuan and a divided trade community centered on a Western and an Asian Hemisphere.

Australia will need to manage this passage carefully, as we are de-facto part of the Asian Hemisphere on trade and the Western Hemisphere on defense.

US security guarantees to the Gulf States do not look that valuable today.

The big question is whether this collapse in faith leads to volatility in asset markets.

It will be a close-run thing.