Australian Twenty Stock Portfolio: Significant Changes and Feb-2026 Performance Report

The surprising scale of the US-Israeli action against Iran, coupled with mixed messaging on the war aims has brought forward a strategic positioning for a time of conflict.

Following our usual regulatory boilerplate, we report on an outstanding performance in February 2026, and our thinking on how seismic shifts in geopolitics warrant a heightened emphasis on a long-standing theme: the war materiel bull market.

This is not the world I want, but a portfolio manager must respond to visible events and judge which changes warrant a change in relative portfolio weights.

Our strategy is to canvas a set of viable themes, in a balanced manner, but to reflect our conviction via relative portfolio weights. When this works well, winners can run and profits are made available to rebalance upwards other improving themes.

This note serves as an object lesson on how we implement this philosophy.

Model Portfolio Offering

The Savvy Yabby Report distributes our institutional grade model portfolios to paying subscribers on a monthly basis. The current list includes these strategies.

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

The existing research notes and newsletter offer remains, but you will see some tighter integration between what we write there and the model portfolios.

Regulatory Disclosures

This service is owned and operated by Jevons Global Pty Ltd.

The licensing and complaints procedure is outlined in our Financial Services Guide.

For legal reasons, I need to include this informational disclosure.

These portfolios follow the Jevons Global investment process.

The last change to the model portfolio was effective at close 8-Jan-2026.

The changes were described in the Australian Twenty Stock Portfolio as published on this substack on 7-Jan-2026. The performance published here is based on the total returns for the model portfolio, on a dynamic weight basis to capture movement.

Real portfolios will differ in terms of the costs of trade, which are not included and the timing of any stock switches. The trades are modeled at close, but that is not known ahead of time. Therefore, these records do not represent a real portfolio.

Nonetheless, they are a guide to the approximate performance of the model.

NB: Past performance is no guide to future results.

Model portfolios are not audited and are only approximate guides to real results.

Performance Summary for Feb-2026

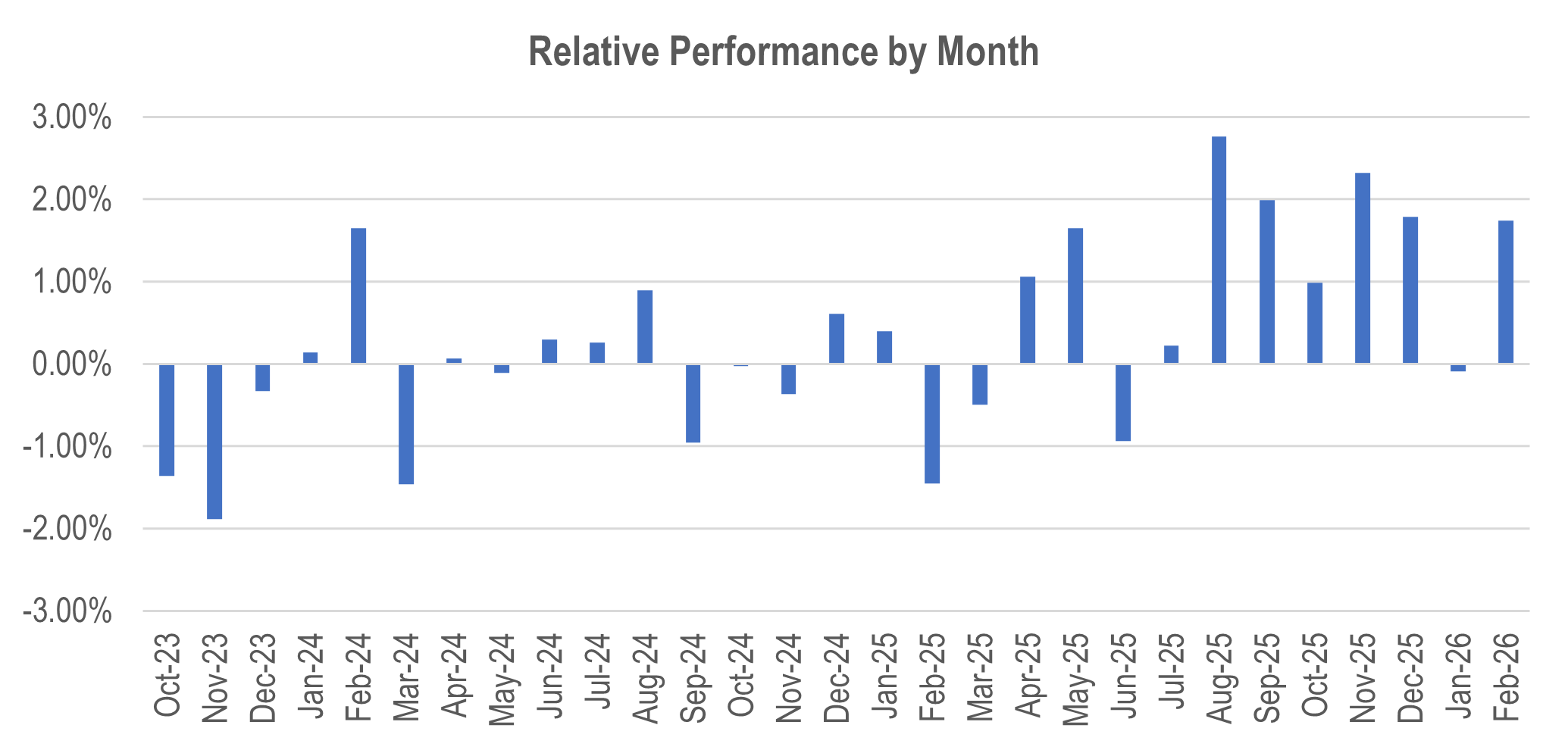

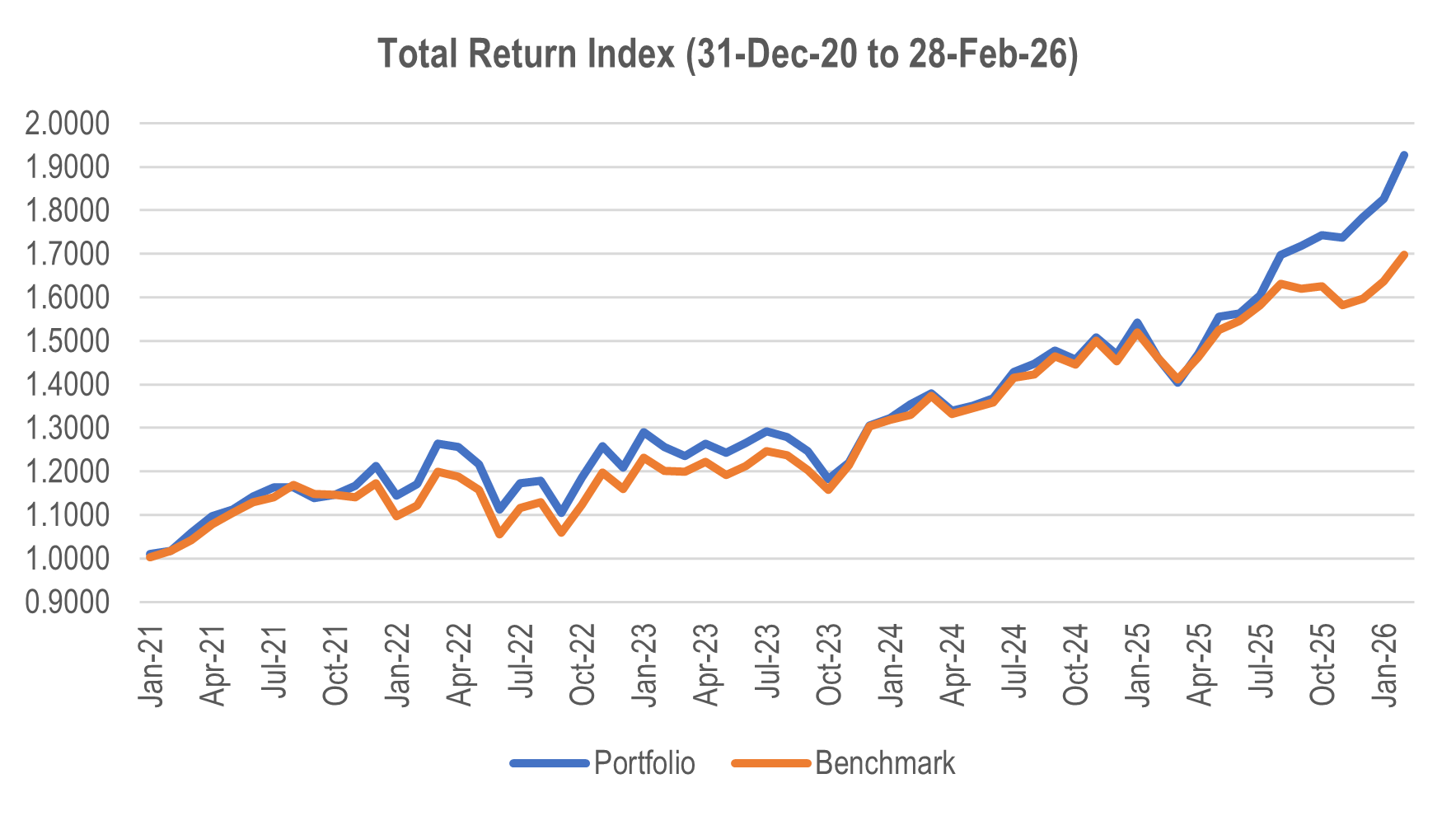

Overall, it was a terrific month for the benchmark S&P/ASX 200. Through the month the total return of the index (XJT), was 3.76%. The return for the model was 5.50%, which was 1.74% ahead of the benchmark, renewing our positive alpha trend.

The positioning in resources helped with that sector contributing 2.82% of positive performance, with Finance adding 1.34% and other sectors detracting.

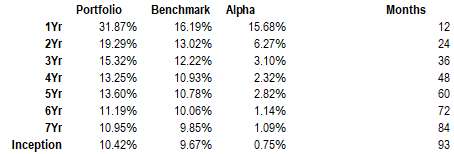

The recent episode of performance has lifted averages over all periods since inception.

Note that uplift in relative performance has been most noticeable in recent years and is reflective of a period where we avoided expensive stocks like Commonwealth Bank, CBA.AX, and much of the technology sector, except Technology One TNE.AX.

Around the middle of 2025 we judged that resources were undergoing a cyclical shift to higher commodity prices, and a broader and stronger demand outlook.

In July of 2025 we funded an overweight in gold miners and battery mineral stocks by selling our long-standing position in Technology One. That proved to be an excellent move and set the stage for a six-month strong run in performance.

Now we are adjusting that strategy once more with increased conviction on a broader recovery in base metals and uranium, alongside gold and energy transition metals. We are purposefully down weighting rare earths.

Our short in rare earths is a contrarian call, which is explained below the paywall.

The summary data continues.

Key Contributors

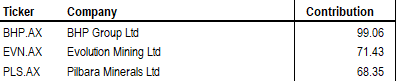

The top three positive contributors to performance in Feb-2026 were:

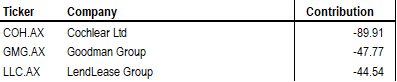

The top three negative contributors to performance in Feb-2026 were:

In a nutshell, it was a positive month for resources, despite the earlier correction in gold and other precious metals. It was a bad month for technology, real estate and health care. Cochlear reported a poor result and outlook and was punished.

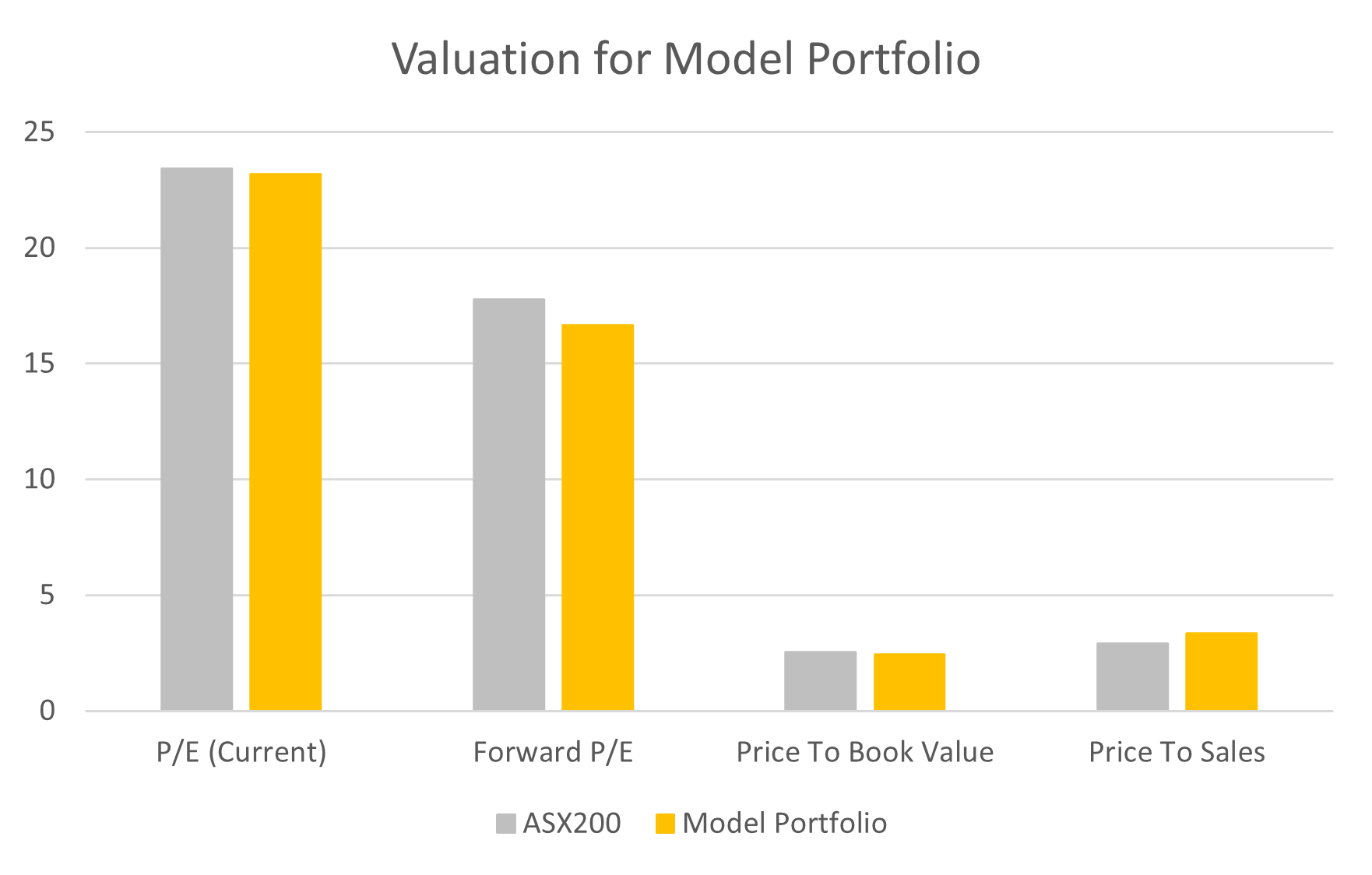

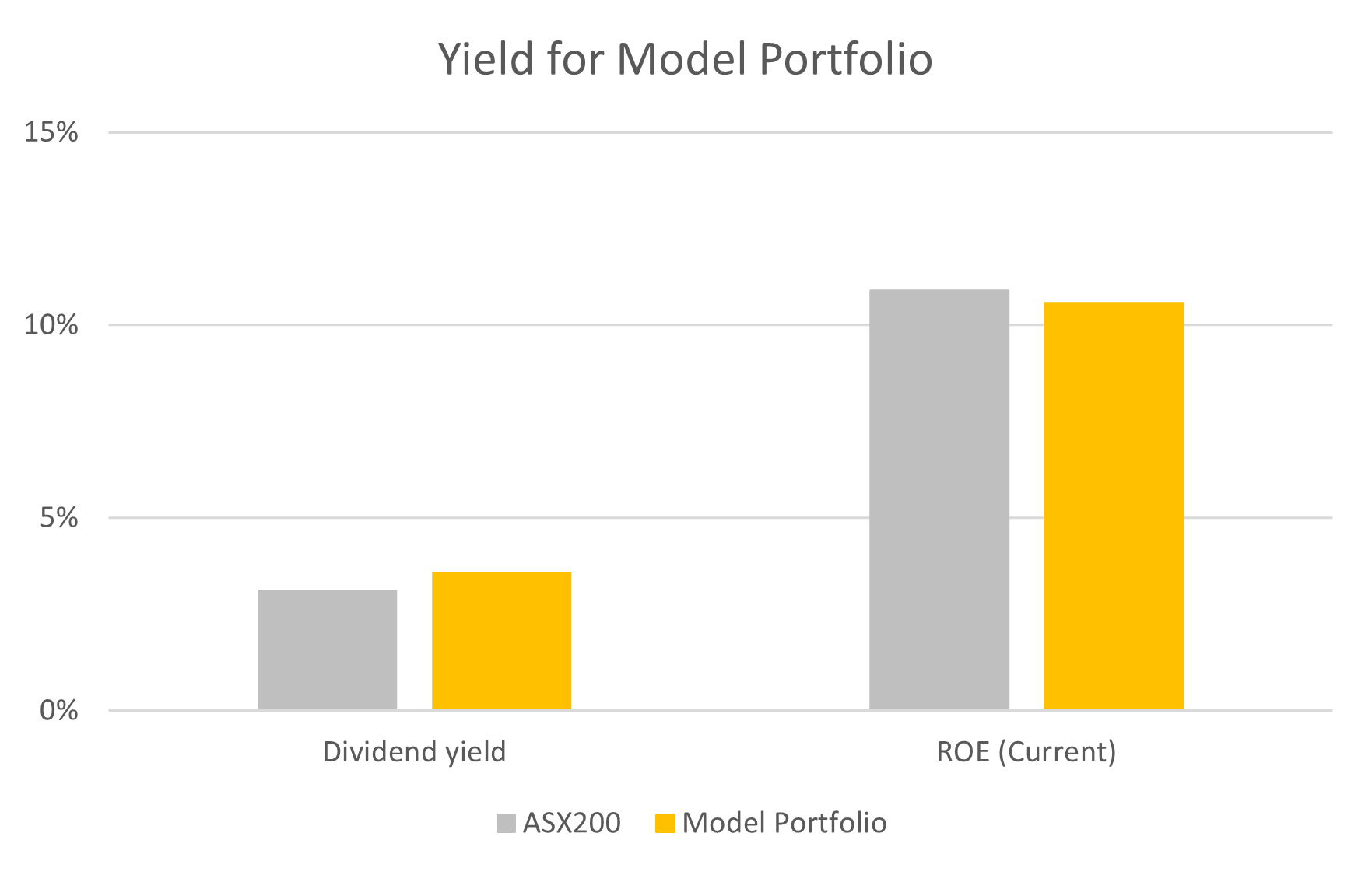

Portfolio Valuation Metrics

The portfolio is showing valuations generally in line with market.

The dividend yield and Return on Equity (ROE) are also in line with market.

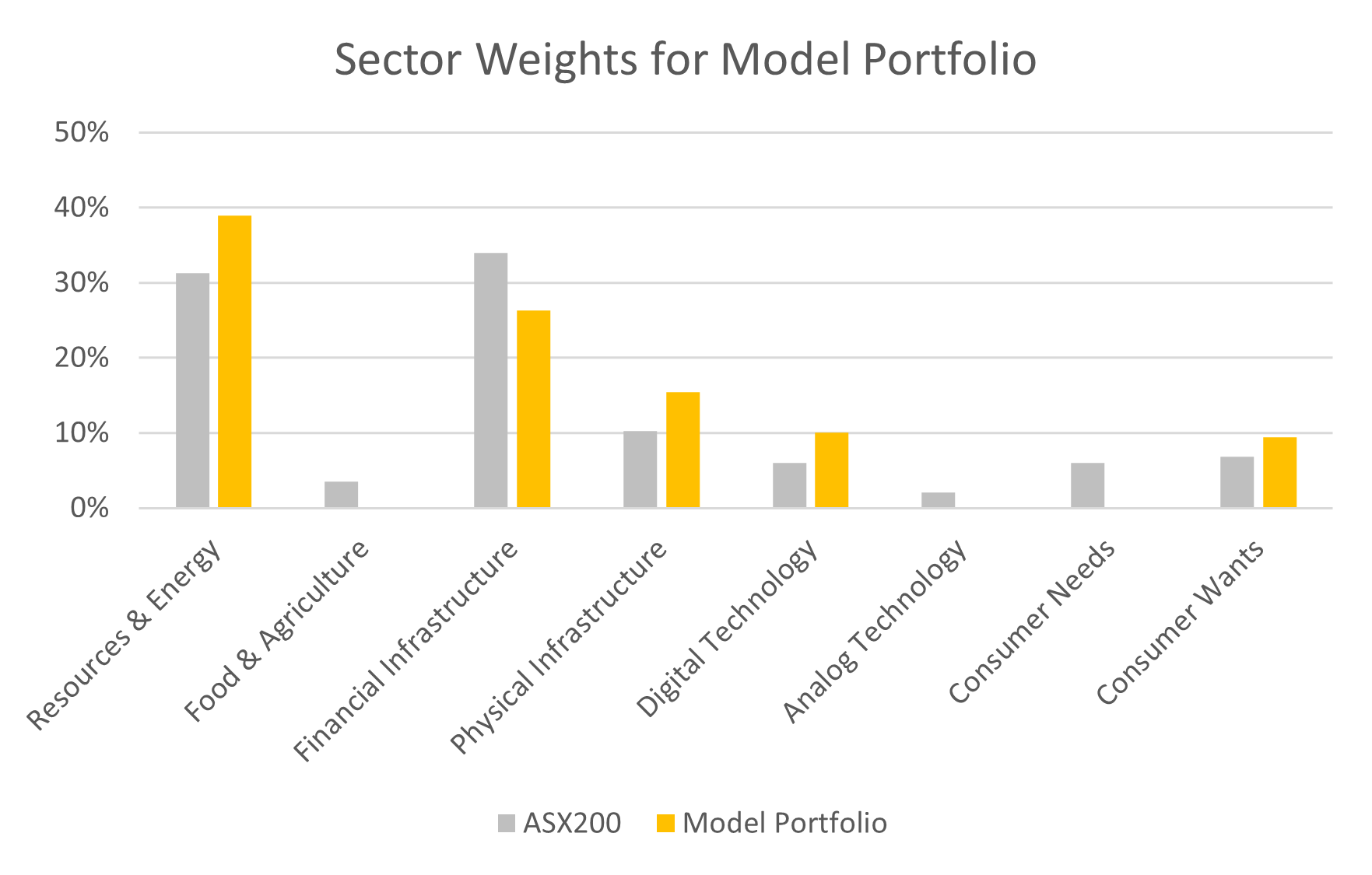

The portfolio is overweight resources, physical infrastructure, consumer wants and digital technology, and underweight in financials and consumer needs.

This positioning is driven by relative valuation and a thematic bias to those sectors which benefit from persistent above target inflation. In our view these are:

Commodities

Real Estate

Import-oriented Consumer Sectors

The first two are fairly clear. Provided that global demand holds up commodities are a clear beneficiary of slow supply response regulating demand via higher prices.

Real estate is less obvious, and was punished last month, on the view that is sensitive to interest rates. In the first-order, valuation is sensitive to higher interest rates, but Australia has a housing shortage, and rising prices lift replacement values.

In our studies of the 1970s, which included living through all of it, land values and real estate are a beneficiary of stagflation. The best of all assets is a long-life asset that can be funded with fixed-rate debt and has rising replacement values.

Railroads are a great example, which is why we are long Aurizon Holdings AZJ.AX.

Other great examples are housing developers with land banks, like Stockland Group SGP.AX, data centre owners and developers like Goodman Group GMG.AX and the major planned infrastructure groups like Lend Lease LLC.AX.

We had a bad month in these plays, with the exception of Aurizon, because the market has yet to assimilate the prospect of stagflation in Australia.

It is not necessary for this scenario to arise for our positions to make money.

The valuations are good.

However, if stagflation does arrive then it is better to have some hedges in place.

The current weights and portfolio changes are below.