Hegel and Thematic Investing

Yesterday I had the temerity to suggest that I know how the USA vs. China story ends. This level of chutzpah seems absurd until you understand the philosophy of narrative thought.

I am often disparaging of what I term “Narrative Investing” with the implication that I think it is a dumb way to invest your capital. Why then tell the story of Hegel?

The markets run on mythology which is the full picture of human narrative.

Narratives are stories told as if they were true but always contain false premises. The higher level of mythology encompasses false narratives, which is all of them.

Mythology is neither true nor false at the level of character and storyline.

The art of making mythology is to invent dynamic narratives that breathe humanity into the story of all human lives as lived. They are imperfect and they change.

There is good and bad in everyone, and a never-ending search for the light.

I do not intend any mystical revelation by uttering such words.

Impermanence, fallibility, and fragility are simply the facts of life.

This is why I focus on the unfolding dialectic of stories as they are told in the financial market. Whenever the old story starts to wobble and waver, I look for the new ones.

Rest assured, the market will always invent new stories, new fads and new fashions.

The financial market is a human arena for public dreaming.

The Thematic Investment Philosophy that I proselytize is Hegel, both Pure and Applied.

In order to keep myself nice, I also actively and publicly disparage my own philosophy.

I have a pet name for this philosophy: Neologistic Nihilism.

Neologistic Nihilism is the philosophy that espouses inventing new words for nothing. It accurately describes the thought process of labelling themes.

The business of meta-thinking is about frameworks for thinking, which is not thinking.

The concept of meaning is absent for there is none.

The physics analogy is simple: at the center of meta-thinking is a Black Hole.

You see the Black Hole for its effect on the surrounding world.

You cannot see stuff enter the Black Hole, and nothing escapes from it.

However, all light is bent by the impact of the thinking going on inside that hole.

Think of mythology as the timeless metaphysics of the human mind.

Human mythology is the bones of old narratives that always repeat but are never the same twice. In the Western tradition they are pure Heraclitus:

The universal truth of the Neologistic Nihilist is that only myths are true.

Human affairs are not at all like the world of physics.

It is all metaphysics.

Every Story has a Beginning, Middle and End

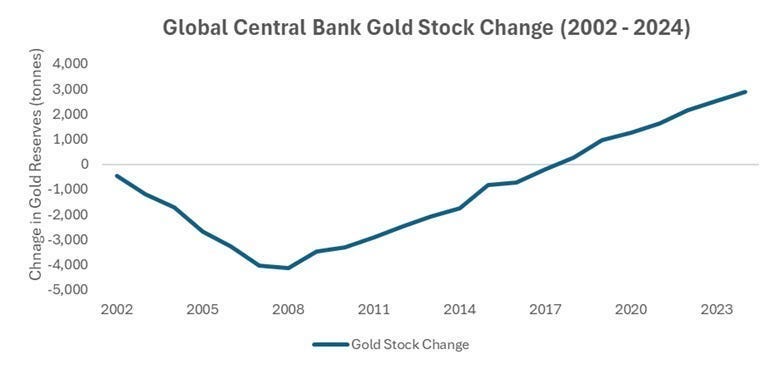

The thematic we just identified: The Market Schwerpunkt (Gold vs. Bonds), is a perfect example of Hegelian Dialectic in action. Every market story has origins in past schisms and ruptures that changed the thought patterns of market participants.

This gold bull market started with a clear schismatic moment in central bank thinking.

The task of the market analyst is to properly identify the signals that mark and define a general and widespread change in thinking. It is narratives that will move markets and they are none of them true as timeless absolutes.

Market stories are true myths because they always reverse.

It is not that anybody was telling fibs, although lies are the stock in trade of all those who aspire to rhetorical influence, it is just that the world changed and minds were forced to change, in order to change behavior, in order to survive.

Practical investment is the art of survival, by thinking, in a changing world.

If the world changes on us the sign will be a change in our profit and loss. The hard part is to tell which fluctuations herald persistent change and which are noise.

In relation to gold, we can see that the Global Financial Crisis (GFC) of 2008 marked the key global turning point in the revealed preferences of Global Central Banks.

Prior to the GFC, central banks collectively sold gold on a trend basis.

After the GFC, central banks collectively bought gold on a trend basis.

As much as I like to rhetorically sledge Central Banks, they are not run by fools.

There are many able women and men devoted to the cause of properly banking their respective governments and thereby ensuring financial stability for their nation.

You can disagree with their decisions, but central banks do have a purpose.

They are the bankers to their governments operating inside a myth of independence.

What changed, as result of the GFC, was the birth of Quantitative Easing.

Mythological purpose and intent is the glue for all social fabric.

U.S. Government is supposed to be of the people, by the people, and for the people.

The famous Eye of Providence is on the back of each US One Dollar Bill.

What changed in the Global Financial Crisis, is that the global shortage of dollars led the Federal Reserve of the USA to print a lot of new dollars. Some went direct into Wall Street coffers to rescue institutions that were otherwise worthless.

Other dollars sped across the globe, in the form of Swap Lines, that involve short term USD denominated loans needed to meet USD denominated debts in countries whose national currency is not USD, but which earn USD through international trade.

When this happened, and thank God it did happen, all the central banks on the planet found out who their banker really was. They thought they were King of the Hill as the banker to their own governments, but they were all on the hook to the US Fed.

The emergency swap lines, from the US Federal Reserve, the bailouts for all friends on Wall Street, and the helicopter money to shore up Main Street, were the beginning of this story we are living.

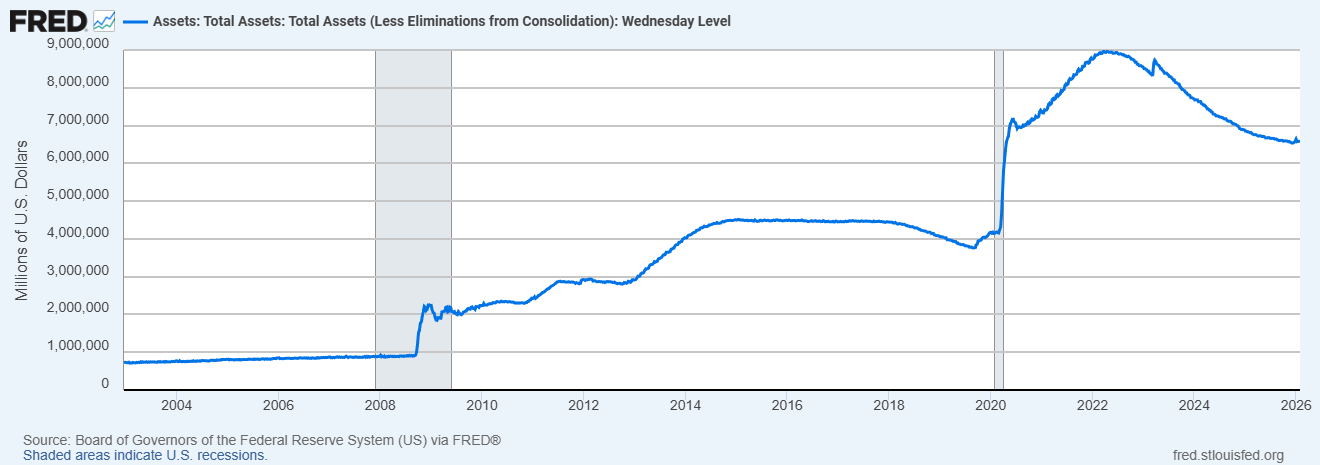

The middle part happened when Quantitative Easing became permanent.

You can see the schism in Federal Reserve behavior in this one famous chart.

The balance sheet line Total Assets (Less Eliminations from Consolidation) is no secret and is transparently published under the WACL moniker on FRED, the St Louis Federal Reserve website. When that line jumps up suddenly, the Federal Reserve just printed lots of money to buy US Treasury Bonds, some new, some old.

Quantitative Easing is a method to finance the government with new money.

In our monetary system, all money is credit, and it is backed by confidence.

What the Global Financial Crisis (re)taught every investor is that financial markets entirely depend on confidence. Debt monetary systems are a House of Cards.

This understanding, of money, government, and power is now popular culture:

The present moment in time represents the widely understood middle of the story, on the way to the inevitable end. I do not mean the “End” in the sense of cataclysm.

The End in Sight is the end of this monetary system.

It does not follow that this is the End of Time.

The End of Time only happens at the Event Horizon of a Black Hole.

Notice that I modulated the rhetoric for dramatic effect.

What we know is that the USA has a debt problem and is looking for new ways to share that problem with the world. One way that is actively being tried is tariffs on imports to the USA, in order to offset the trade deficit in goods.

Tariffs are a Trump Project to offset debt by raising new revenue.

You can see how we are past the middle of our story. We can see the outlines of how it might end, but we don’t know the details of how it ends.

We do not know who wins from the end of this story.

It could be China, it could be the USA, it could be you, I just hope I get through it.

The key message of this note is that I can tell you a specific timing tool to make your own judgement on when this story has ended.

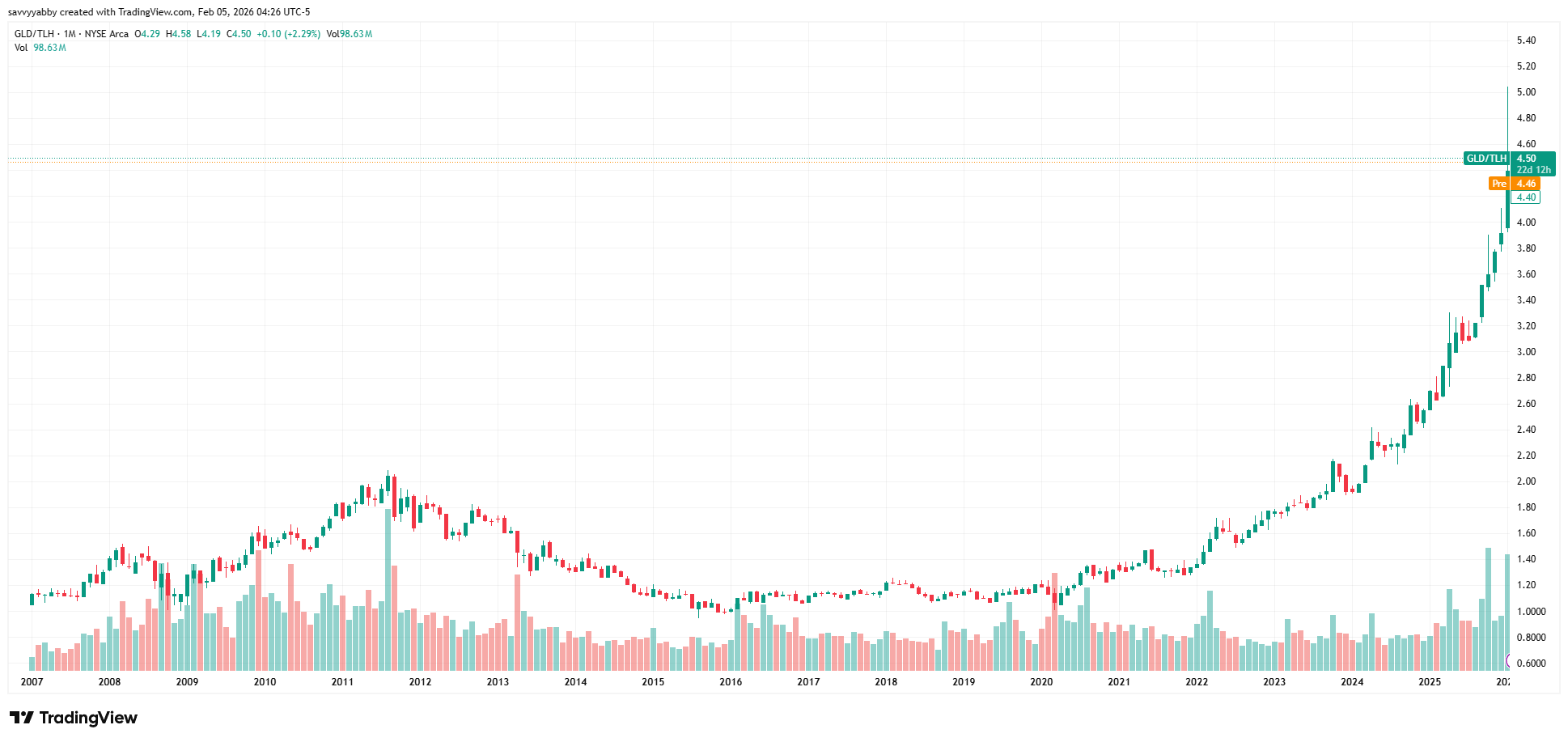

The pulse of this story is the relative return of Gold versus US Treasury Bonds.

I only need to say it in words, and you know that this is true.

Gold pays no monetary interest.

US Treasury Bonds pay regular interest and promise to return your principal.

Gold is no promise, but US Treasury Bonds are a promise.

The question to study is which leg is winning this sack race.

Yesterday I showed that 10-Year U.S. Treasury Bonds, in the form of the ETF ARCA: TLH have been losing consistently versus Gold, in the form of SPDR ETF ARCA: GLD, since around 2020, when the trade tensions between the USA and China first heated up.

One should understand that Wall Street has many stories to tell about gold, and many more that talk about interest rates and bonds. The only story I care about is here:

What drives investor behavior is a winning story, and the puzzle is whether the story is a new one, an old one, a young one, or a mature one. We cannot say which, for sure.

What we can say with confidence is that the above spread will reverse.

We do not know when it will reverse or why behavior will change when it does.

What I think I know, and this is the reason to be sharing it, is that I think we have the pulse of this narrative, and we have the anchoring mythology behind it.

What happens next is an unfolding story of trust in the US Government.

Gold will be there tomorrow if you hide it right, safe from grasping hands.

The purchasing power of U.S. Bonds may not be there tomorrow.

Presently it is eroding in very public fashion.

The end of this story is clear:

Does the USA restore global trust and confidence, or does it destroy it?

Notice that I answered this mythological conundrum with a new myth.

What animates real stories about real people is dynamic tension.

Identify the key opposites in play and you have your thematic dialectic.

Hegel and the Dialectic of Opposites

Georg Wilhelm Friedrich Hegel. according to my Bible, the Stanford Encyclopedia of Philosophy, was a German philosopher living in the period 1770 to 1832. This was a time of great turmoil in Europe, with the French Revolution and Napoleonic Wars.

It was also the time of nation building in the newly independent USA.

In Australia, it marked the birth of a British colony, that was an outpost of Empire that soon delivered gold and wool as tribute to its master. In this crucible, was forged this nation, and all of the baggage that goes with that, whether you like it or not.

Hegel is described as a German Idealist, who was very systematic in his thinking.

You will understand his appeal to this theoretical physicist.

Hegel believed in a teleological account of history.

Hegel posited that history unfolds as a dialectic between opposites.

In mathematical logic, truth is absolute, but relative to an axiomatic premise.

This is a different way of saying that many truths are possible, in a logical system, but that incompatible premises lead to different and disjoint mathematical systems. The miracle of mathematics is that some such systems accurately describe our world.

There is plurality of true mathematical systems which are contradictory in the assumptions they make, among each other, but not within any one system.

The Lofoten Islands of Norway are formed in an Archipelago.

You can cross from one island to another, by boat, or sometimes by a bridge.

The analogy to thought is that you must present a Passport of Premises for entry to each island. Logical thought is self-consistent on each island but may not be if you journey between them. Something changes in the presumed rules between them.

Once you have absorbed and pondered this metaphor, you will understand Hegel, the process of mathematical invention, the dialectic of history, and my philosophy.

When we pass from one island to another, metaphorically, or physically, the rules will change in subtle ways that reflect the natural tension between opposing ideas.

Some islands of thought are considered right wing.

Other islands of thought are considered left wing.

I escape this mental prison by choosing to survey the scene from the air.

If you need something to hold fast to, recognize that the Scientific Method will, on several occasions in history past, and that to come, make a radical reversal of some rules for life on Earth. These are the imagined absolute Laws of Nature, but they remain unknown, in complete depth. Our perception of them can change.

The History of Mathematical Invention

The history of recorded mathematics is almost as old as the written language records which attest to mathematical thinking. The Ancient Babylonians used cuneiform script to write down accounting records of commerce.

The word “Algebra” originates from Persia in 820AD with the Al-kitāb al-mukhtaṣar fī ḥisāb al-ğabr wa’l-muqābala (The Compendious Book on Calculation by Completion and Balancing), which became known as the Al-Jabr (AL-GEBRA), for short.

The Renaissance reinvention of artistic expression brought us perspective.

In each innovation, from number systems, through the algebra of unknowns, zero as the absence of counting numbers, negative number, and so on, new rules became abstracted from the apparent underlying order to become mathematics.

When understood this way, mathematics is a system of thought, which is capable of infinite extension through the processes of mathematical invention and discovery.

The relationship of this to Hegel, is that the meta-mathematics of describing how we fit together these different and (often) mutually incompatible logical systems, is the analogous process to the unfolding of a dialectic of opposites.

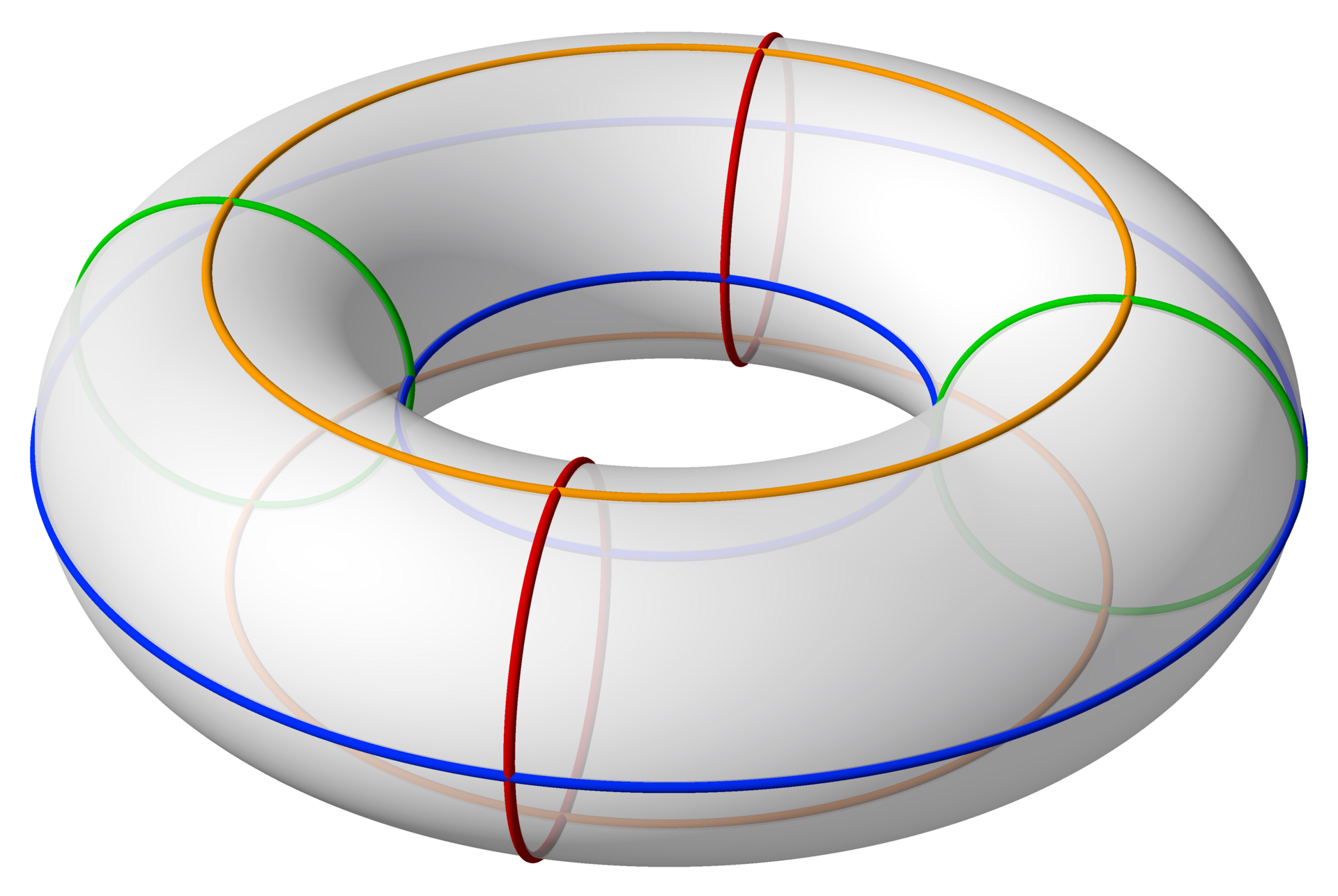

Euclidean geometry (parallel lines do not meet) and non-Euclidean geometry (parallel lines meet), became capable of unification once Gauss, and others, perfected the idea of intrinsic curvature of a surface, to nail the difference between a flat sheet of paper, the round surface of an orange, or the curved, but not round, surface of a saddle.

Notice that intrinsic curvature is a non-trivial concept that requires care in definition.

The torus, or doughnut, is curved when embedded in 3D, but flat in 4D, since it is nothing but a rectangle, with opposite sides identified.

Mathematical invention is subtle, because our definitions must make sense of a real situation in geometry, like that of a flat rolled-up sheet of paper, a tube.

This process continues today. Einstein found that non-Euclidean geometry was key to understanding gravitation and made it a central tenet of General Relativity.

The necessary conceptual leap to negate a prior axiom (parallel lines never meet), with the opposite (parallel lines always meet), requires a certain flexibility of mind.

“The test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time, and still retain the ability to function.”

― F. Scott Fitzgerald, The Crack-Up

I contend that this flexibility of mind is the essential skill for human adaptation.

In times of great change, the alternative is to stay mentally rigid, and to get angry.

The Uproar of the Boeotians

It is not a coincidence that Hegel lived in Germany at the same time as Gauss, so far as their contributions to human thought. Hegel was the philosopher espousing the dialectic of opposites: thesis, antithesis, and synthesis. Gauss was the prodigy of mathematics, who contemporaneously discovered hyperbolic geometry.

Gauss knew about perspective and could see that the geometry of Euclid, which was based on the axiom that parallel lines never meet, was objectively false.

You could easily imagine a world where the parallel lines postulate was false.

If you are a mathematician, and you can imagine a new world, there is a possibility you can locate a self-consistent set of premises that support that world.

Really great mathematicians like Gauss open whole new worlds. The tricky part for such people is that their ideas might offend the conventional thinkers of the time.

The mirror of our time is to fear the Boeoetian Uproar of Populism. You can see this uproar playing out across societies the world over. There is no need to explain it.

Politics is based on rhetoric, which is the representation of “facts” in the form of active myths that have emotive, and therefore motivative emotional content.

If you want to be a politician, master rhetoric, and emotive language.

If you want to be an investor, master the Hegelian dialectic of opposites.

That is my philosophy of thematic investing in a nutshell.

I accept that any attempt to accurately forecast the meanderings of asset prices will be flawed at best, and downright misleading at worst. However, what I am trying to understand is how investors are thinking, and what flaws in thinking are clear.

Those who are mentally uncomfortable with retaining two opposing ideas in their head at one and the same time, will choose certainty in their narratives.

The story is considered right and true until it is not.

This is the essence of how trends in human action are made and perpetuated.

However, all stories, of the humankind, are mythologies.

They all turn at some point.

Conclusion

Your challenge, should you choose to accept it, is analytical with purpose.

The teleology of your portfolio is in your hands.

Construct your diagnostic instruments, by forming financial spreads, which are the ratios of accumulated investment returns. Note which of these are trending.

Divine which side of the given trend you want to be positioned.

Construct and deconstruct the narratives that will form to justify that position.

Do not ever be fooled that such narratives will prove permanent.

They never are, and they will reverse.

However, you have your target spreads and so you know when the story needs to be changed, and some inkling of why. Follow that path, and you will succeed.

Investing is no science, because it is all mythology, both pure and applied.

Happy mythologizing!