The Global Power and Energy Transition

The global outlook continues to deteriorate due to the Israel-USA war-of-choice in the Gulf. We discuss our new thematic framework for the geopolitics of investing.

This note provides background thinking to a general rebalance to tweak our fully invested model portfolios for a bias to yield and value to help ride out a likely volatile period in global markets. I will put these out over the weekend.

The Need for a Framework

In this note, I bring together a number of strands of thinking that inform our moves within the model portfolios. These are not major changes by turnover but establish consistency in positioning to match how we view the unfolding macro-outlook.

The markets remain relatively calm in spite of the sharp adjustments in commodity prices, with energy up, and precious metals down. We think this is calm before the storm. Orientation is important, and so it is worth recording how we think about:

The tactical decision on cash holdings

The likely impact of foreseeable disruption to the Australian economy

The Global Power and Energy Transition dynamic that is now in foreground

A Tri-Polar model of fading, rising and dominant global power centers

The purpose of model portfolio constructions is to make all of this concrete with a particular set of stock selections, and allocations, across stocks and regions.

The short version of this story is that we are becoming more defensive, with a tilt to value and yield, select commodities for inflation hedging, real asset-based business, and appropriate growth franchises that will likely maintain pricing power.

I never like to bet on a single outcome, so you can think of this background thinking as my attempt to start gathering a foundation for analysis of current events.

I am conscious that geopolitics is in the ascendant and so we need a way to reason about it which does not get caught up in foolish narratives on winners and losers.

There is latent potential for many bad financial outcomes in this setup.

The wise thing to do is to take stock of them and diversify our bets.

However, supply shortages, higher prices, and tighter money seem baked in.

Tactical Questions

In a private portfolio context, there is always the option to raise cash, or to position among different asset classes: equities, real estate, infrastructure, bonds and gold.

There is also cash which we treat as a liquidity pool and last resort.

In the present market conditions, some cash is good, and I would personally let the income from investments build up as cash, without deploying new cash to market.

Having some cash preserves optionality if opportunities present themselves.

This newsletter consists of general advice only and cannot take account of personal circumstances. I do not and cannot know your personal risk appetite, nor your stage of life, upcoming cashflow requirements, or anything of that nature.

You should seek help from a licensed advisor for personal financial advice.

This substack is designed to be informative, and educational, and we run our model portfolios in listed equities to provide concrete implementations of our thinking.

The thematic background to these strategies is also of value.

The outlook is clouded by a rising risk of stagflation. For this reason, we begin with a discussion of the Australian economy as a leveraged bet on commodities.

Australia has a Commodity Economy

It is important to appreciate that the Australian economy is nothing like that of the United States. We may share a lot in common, but the economic structure is very different, due to the dominance of commodity production in Australia.

Furthermore, while the bulk of Australian Foreign Direct Investment (FDI) may come from the United States, that impacts our capital account. In discussing the outlook for the domestic economy, we need to look at the income account.

It is customary for the Australian financial press to ignore this distinction in market commentary due to the penchant for reporting the view from Wall Street.

The view from Wall Street is very different to the view from Martin Place.

At times like this, it really is essential to understand and work with the difference.

Working against the intrinsic nature of your home economy is a bad idea.

We have seen this play out already with populist ideas that we should diversify our commodity trade away from China and towards the USA. This is not a sound idea because the American demand for minerals is a small fraction of that of China.

It suits US-funded think tanks to promote this idea but not Australia.

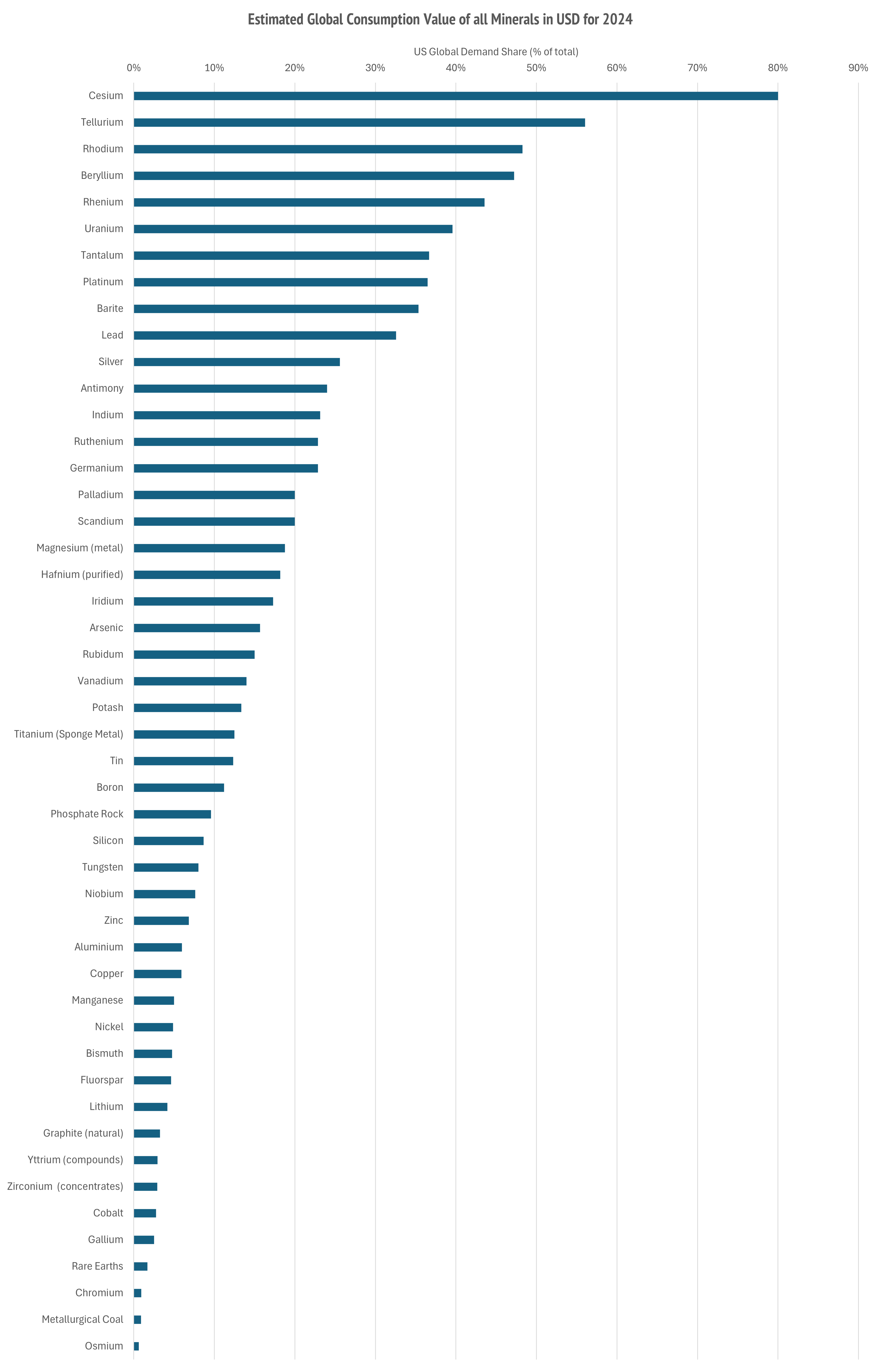

In our opening note Commodity Outlook 2026, I used US Geological Survey reports to dimension the share of global critical minerals demand represented by the USA.

On average, across 60 critical minerals nominated by the USGS, the dollar-weighted average of US demand is 6.7% of the global total. This is small.

China is the global market for critical minerals.

You can complain, but China has a monopsony position as the dominant buyer of minerals globally. To fix this you need new Western factories, not new mines.

The problem, for Australia, is that we are diversifying away from our key buyer, and are shunning FDI from China, in mines, whose output goes to China.

This will prove problematic down the track.

Our largest mineral commodity exports are bulk commodities like iron ore, thermal coal, coking coal, natural gas, copper and gold. That is how we make money to buy manufactured imported goods. Historically, the terms of trade for Australia, which measures the price level of what we export, versus what we import, was boosted by the entry of China into the global trading system. China demanded copious mineral exports from Australia, at elevated prices, and returned cheap manufactures.

This golden economic bargain is now breaking apart.

The fracturing of this model does not appear to have been driven by China. It is a deliberate policy decision of the Australian Federal Government.

I will not get into the why of this policy decision, but it is bipartisan.

With the rising temperature of geopolitical tensions, I do not expect any reversal of the policy is likely, or even possible. Chinese investment now shuns Australia.

As shown with the demand profile above, US FDI will not replace Chinese FDI in the growth of our minerals and energy industry. The US demand for minerals is small.

For whatever reason, Australia has chosen a deliberate policy to shrink our minerals and energy industry, with respect to the prospects for Chinese investment.

This is not everything, there is Japanese and South Korean minerals investment.

However, there is precious little US investment in minerals.

When looked at this way, the prospects for the Australian economy are less fulsome in potential growth than they were before. Western Australia and Queensland, and to a lesser extent South Australia and the Northern Territory, still have good prospects.

However, the states that do not depend on resources, but perform all the services that have historically recycled export earnings into a high domestic standard of living, face a potentially difficult and volatile period of adjustment.

The uncomfortable truth is that Australia benefited greatly from higher terms of trade, due to Chinese minerals and energy demand, which kept our currency higher than it otherwise would have been, and interest rates and inflation lower.

That magic circle of a firm currency and lower interest rates is now reversing.

Leave aside, for a moment, the fact that this was a deliberate bipartisan policy, pursued by both sides of politics, in the name of derisking our economy.

It falls to private investors to derisk their portfolios and survive this policy.

I have lived in Australia long enough to know that it is possible to survive Australian policy errors, no matter how egregious, and no matter how damaging and foolish.

I survived the 1970s stagflation and lived to write about it.

Do not get me wrong.

Australia is the Lucky Country in that we always have opportunity to invest, and when the dust has settled there look to be terrific inflation hedged opportunities across the agriculture sector, and the energy transition, along with minerals and energy.

Remember that all of our model equity portfolios are fully invested.

Derisking means repositioning the mix of stocks with an eye on what is coming.

For that, we need a framework for thinking about the future.

The Global Power and Energy Transition

Everybody understands that there is an energy transition in progress, from fossil fuels towards low carbon replacements: wind, solar and nuclear energy.

Due to the large role played by oil and gas in transportation, this transition has a natural focus on electrification, electric motors, generators and batteries.

Given the radical technology shift involved, there is a huge requirement for capital investment, to phase out the old, and bring in the new.

The political economy of this energy transition is fraught.

The old model of business activity is potentially obsolete, and yet there is enormous wealth and power tied up in the business-as-usual model.

Naturally, the politics of this momentous change becomes fractious.

What ought to be a technological transition, ruled by the principles of science and engineering, soon becomes a power transition and a global political bun fight.

There are many historic examples of a new choice of fuel having huge ramifications in the world of geopolitics and military power. In 1911, Winston Churchill became First Lord of the Admiralty, in Great Britain at a time when the Royal Navy had few ships powered by oil. They were almost all coal fired. Churchill observed that oil fired battleships were faster, had longer range and superior tactical flexibility.

In 1914, Britain had abundant Welsh coal, but no domestic oil. At that time, the only major British interest in oil production was the Anglo‑Persian Oil Company (APOC). The oilfields were located in south‑western Iran, in the Khuzestan province.

Khuzestan remains the heart of Iran’s oil industry today.

In 1914, Britain bought 51% of Anglo‑Persian Oil Company providing direct control of Persian oil. That enabled Winston Churchill to convert the Royal Navy to oil, which was a decisive move in cementing the dominance of British warships over Germany.

The choice of fuel for transportation can have a huge strategic impact.

These choices echo across history. From 1914 until 1933 APOC dominated the Iranian oil industry, paying only small royalties to Iran, and booking the rest as profit.

This exploitative practice, whose origins were military, created huge resentment in the state of Iran. You can read about the consequences of that period, which resonate in the modern theocratic state of Iran, the 1979 Islamic Revolution, and all that.

Now we are living through a war-of-choice that started with a surprise attack by Israel and the USA, on the state of Iran, which was ostensibly about nuclear weapons, now twice obliterated, but has since morphed into control of the Strait of Hormuz.

Cynics might suggest that this Gulf War is all about control of oil.

The year started when President Trump took control of Venezuela. Now he is talking about taking control of the Strait of Hormuz. Can you guess where this ends?

Pipelines that supply cheap natural gas to Europe, supplied by Russia, were blown up in mysterious circumstances. The USA then stepped in to supply gas to Europe.

Now 20% of Persian Gulf oil and gas is cutoff by war, and President Trump offers to form a coalition of states to “unblock” the Strait of Hormuz and to seize Iranian oil loading terminals on Kharg Island. The war aims of this crisis remain unclear.

The war aims are unclear, but the battle is for the Strait of Hormuz.

We started with obliterated nuclear facilities that needed to be re-obliterated, and have been, except for the possible need to go back, and the fight is over oil.

If the USA does succeed in wresting control of the Strait of Hormuz from Iran, and the oil assets of the country, then control of the global oil market falls to them.

Control of the global oil market is a just reward for the good guys.

They can then decide who gets the oil and who does not.

Imagine this was an airport novel.

Who are the bad guys in this noble effort to save the world from Iranians?

Of course, I do not know. The White House never handed me the script behind all the official noise that has flooded this war zone with random tweets and nonsense.

Just follow the trail of Persian Gulf Oil to locate the bad guy on the other end.

Roughly 80% of all Persian Gulf oil exported through the Strait of Hormuz goes to Asian markets. China is the top destination for these flows. Around 50% of Chinese imports ship from Saudi Arabia, Iraq, UAE, Oman and Qatar. Another 10-15% are estimated to originate from Iran, although that number is hard to pin down.

60–65% of China’s total crude imports come from the Persian Gulf.

I guess that is your bad guy. They will hurt a lot if this energy supply is cut off.

In this story, we see how the Global Power and Energy Transition has become the single investment thematic that rules them all. It is positively existential for some.

If Israel and the USA lose this war, the Gulf State oil capacity is likely destroyed and the bad guy in Asia will be in a pickle. If Israel and the USA win this war, they will presumably enjoy strategic control of the Strait of Hormuz.

Either way, it looks like the bad guy in Asia is in a pickle.

Lest folks get too excited by this prospect, China might have other ideas about how to end this war. This is potentially very worrying if you know your modern history.

This geopolitical Great Game is a minefield for investors to navigate.

When you are dealt these cards, you do not trust the dealer.

The overriding challenge is how to navigate a looming global crisis of trust.

Who do we trust and why?

Do we trust official reasons for action, or do we look at the market signals?

Obviously, we need to retain a healthy skepticism on news flow.

The wise thing to do is diversify.

The Emerging Multipolar World

The patterns of world trade in goods and services, financial flows, and geopolitical power and influence are changing rapidly. The rise of China is very clear when you examine data on trade flows, like the major trading partner, by country.

China dominates global manufacturing and so has an outsize role as the source of manufactured goods for most countries globally. This contrasts with dominance in financial markets for Western nations, particularly the United States.

, 2nd, 3rd, 4th, 5th, Not in top 5, and No data; shading intensity corresponds to the rank. Data source: International Monetary Fund (2025). License: CC BY.")

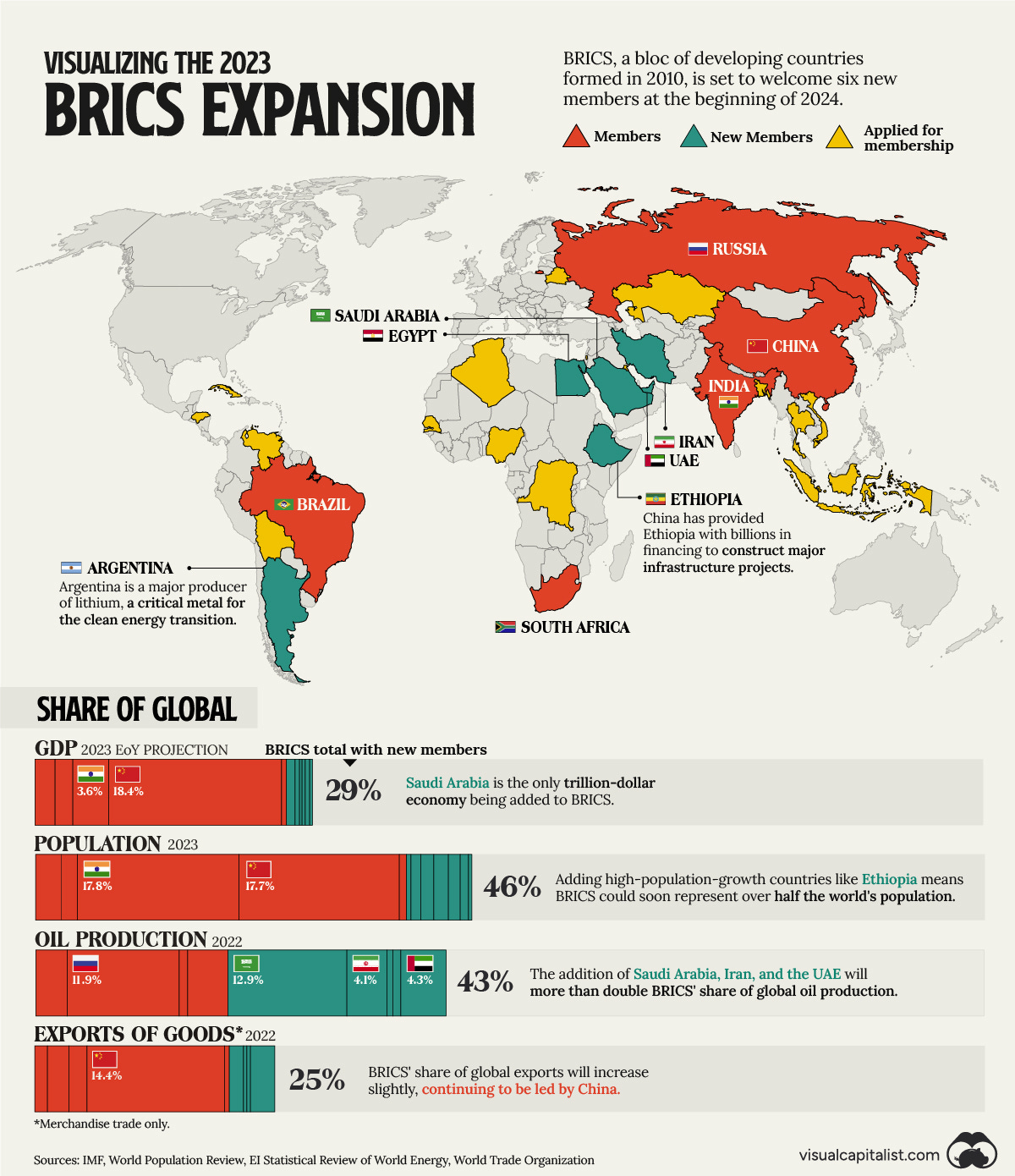

Once we consider the BRICS bloc of nations, and their expansion of membership, it is clear how the patterns of global power and trade are changing geographically.

This map from the Visual Capitalist helps understand the scale of the BRICS bloc.

Rhetoric in many Western capitals has pitched this grouping of nations as being an anti-Western project. I interpret it as a pro-development cooperative grouping.

The concept of developing versus developed markets seems to presume that the categories are fixed, and that there is some natural order to be preserved.

The engine of all human development is knowledge and ingenuity applied to those problems that limit growth and opportunity. This is no special preserve of the West. Indeed, China has successfully harnessed this model so effectively that the uplift in prosperity in that nation is now widely perceived as a threat to Western interests.

Understandably, the developing nations who perceive developed nations as actively trying to limit their growth and development, are suspicious of the motivations.

This has increased geopolitical tensions.

Whereas the old order typically involved a bipolar us vs. them dynamic, such as I recall during the Cold War, this period of tension is quite different.

The model of bipolarity retains some significance, whenever there is a clear regional balance of power, such as between Europe and Russia, or China and Japan.

However, this model does not work at all well when considering the global map of competing interests. There is much mineral wealth in Latin America and Africa, but Western demand is insufficient to develop that. It is a simple matter of per-capita mathematics. Chile produces around 30% of copper globally, but the USA only consumes 6% of global copper supply. It cannot absorb that supply.

For an even starker example, Australia produces about 35% by iron content of global iron ore but the USA only consumes about 1.5% of that supply.

This is population and demographics.

The commodity intensive phase of national development is the infrastructure build that takes a low-income nation to a middle-income nation.

The West is only about 15% of global population, and that infrastructure build is done.

Geopolitical stratagems based on coercive economic control and throttling of access to commodities will not promote global growth.

These policies of restriction will cause global stagnation.

We can see this playing out now, where the USA has elected to attack Iran, the Strait of Hormuz is blocked, global supplies of vital energy and industrial commodities are interrupted, and the prevailing attitude on Wall Street is that no harm will come.

This multipolar world demands that we view each action holistically.

This world will not tolerate 5% of the population, who live in one nation, telling the rest of the planet what to do, when to jump, and how high.

The present situation is intrinsically unstable.

Attempting to roll back the clock, to a past unipolar world, cannot end well.

Nonetheless, some nations seem to think this is a good idea.

In order to better manage this volatile time, we choose a tripolar model.

There are three structural drivers at the heart of the transition:

🔥 Energy Security

🏭 Industrial Policy

🎯 Geopolitical Risk

Earlier, I alluded to the importance of the energy transition underway and gave an example of how past transitions interacted with industrial policy and geopolitics.

The energy system and global industry is moving towards electrification.

This trend works hand in hand with a new industrial revolution involving intelligent machines that make decisions autonomously and respond to a changing world.

The mental model of unipolarity elevates conflict over cooperation.

In this view, there must be winners and losers in this transition.

This is fine at the local level of industrial competition, and the innovation race, but is profoundly risky on a global scale. Humanity has had nuclear weapons for eighty years now. Positioning for one large group of humans to lose is a bad idea.

The Win-Lose contest of unbridled competition will degenerate to Lose-Lose.

That conclusion seems self-evident to this global investor.

There is no fancy philosophy of good-will to all men in this equation.

It is pure hard-bitten pragmatism born of living on this planet for sixty-two years.

Pressing advantage on others, in the popular language of the “chokehold”, can only degenerate into a collapsing global system of international trade and finance.

The United States is pursuing a Lose-Lose strategy for itself and this world.

Given that the three structural drivers are happening in a world whose industrial structure is split across three regions, it is useful to construct a trichotomy.

The transition of power naturally has three psychological perspectives:

The perspective of the dominant center which has that dominance to lose.

The perspective of the rising center which has much to gain just by rising.

The perspective of the faded center which cannot decide who to back.

One force is vital, that of the rise. One force is anti-vital and seeks to contain the vital force. The third force is one of vacillation and indecision.

Who to back, when, why?

Reflection on this structure, in relation to world history, explains much of what we see happening. It makes psychological sense. Identification with one or other attitude is revealed in the daily discussion of global opinion makers and politicians.

Geographically, there are three main centers of change, the United States, Europe and East Asia. West Asia, Africa, Latin America, Russia and Oceania also matter, but they are not the prime centers of industrial transformation.

The fact that there are three centers is not that surprising.

America is the dominant hegemon which appears focused on what it has to lose.

Europe is the former center of world power that is anxious about its own future.

East Asia is the returning superpower of past centuries focused on what to gain.

What is interesting about this dynamic is that Europe claims cultural cohesion, as the cradle of Western civilization, but is internally a fractious political union of states that often pull in different directions. East Asia, by contrast, is many civilizations, that are used to coexisting, competing, and cooperating, because none was on top.

The United States is on top, objectively, in many aspects of comparison. Measured on nominal currency values it is the largest global economy. It has the largest financial markets, that are also the deepest and most liquid. It also has a superb innovation system based on a solid scientific and engineering base.

However, success can breed instability, and the great one in the USA stems from the rise in wealth inequality, combined with a retreat from manufacturing, declining or decaying infrastructure and fractured political and social institutions.

Recent moves by the USA have been restrictive and coercive towards the interests of other nations. Rather than facilitating global growth and development, it appears that the common thread behind all foreign policy is to frustrate global development.

Increasingly, it looks like the USA stives to win by making others lose.

This not a pro-growth attitude to take for the leading global economy.

In contrast, China is committed to its own path of development, which emphasizes industrial development and technology deepening. The per-capita GDP of China is around $12,000 USD, which is right around the World average. In many ways, this economy is a proxy for the average global consumer.

The development strategy for China is focused on developing Global South nations as consumers of manufactured product, suppliers of commodities, and clients for the development of infrastructure. Japan did the same thing in the 1970s.

Increasingly, it looks like China wants to keep others afloat, so it does not lose.

Strategically, this approach to foreign policy makes perfect sense. War is risky at any time, and more so when you are an emerging challenger. There is much to lose.

Japan is a willing partner in this game simply because it is the last great capital goods provider outside of China. New factories need precision machine tools and elaborately manufactured items, plus advanced materials, to support modern technology.

Japan has not weaponized trade and is globally trusted.

The position for Europe is murkier. While it started this century as a leader in green energy that competitive position was lost to China. The Ukraine-Russia war focused minds in Europe on remilitarization against a backdrop of energy insecurity. Tariffs imposed by the USA have reminded Europeans that all is not fair in love and war.

The tripolar configuration of societal attitudes fits well with the geopolitics.

It is this model that informs my thinking on global markets.

The Tripolar Model

Pulling this together, we can summarize our thinking in this one diagram.

In this new system, each major region plays a distinct role.

The United States is the stagflationary hegemon: the only major economy that benefits from higher oil prices, armed with energy dominance, fiscal dominance, and a defence‑industrial complex expanding at the fastest pace in decades.

Europe is the energy‑vulnerable stabiliser: a region forced into strategic re‑militarisation while relying on healthcare, utilities, insurance, and high‑quality cashflows to buffer the shocks of imported energy and slow growth.

China is the industrial deflation engine: the world’s producer of electrification hardware, operating under deflationary pressure and energy insecurity, and doubling down on the sectors it considers strategically indispensable—EVs, batteries, energy security, telecoms, and financial stability.

Japan is the industrial reflation engine: the mirror image of China, with rising wages, rising capex, defense expansion, and a once‑in‑a‑generation industrial renaissance driven by supply‑chain rewiring and BOJ normalization.

Around these four pillars sit the essential minor players in Asia:

Taiwan anchoring semiconductor sovereignty

Singapore anchoring Asian financial stability

South Korea for semiconductor and smartphone diversity

Australia anchoring hard‑asset supply

Together, these roles form the architecture of our portfolios.

Outside of these major areas, we have non-aligned nations like India, the northern bloc of Russia, and a great diversity of other nations in West Asia, Africa, and Latin America, alongside ASEAN, the United Kingdom, and Canada.

I do not mean to pretend that the world is as simple as sketched above.

However, this tripolar dynamic is the governing principle.

Notice that Asia is not a unified bloc in any political sense, but the trade flows are very integrated. The most likely reason we can see for the continued rise of Asia, is that it has trade and economic development as the primary focus, not conflict.

The USA may benefit from higher oil prices and restricting technology access.

Europe may find itself united militarily by an external threat.

Asia is united by common interests in prosperity not civilizational homogeneity.

Personally, I hesitate to call one player a winner and another a loser in the game of life.

Who am I to say who won and who lost?

However, I am an investor, and I think the Asian model is the one with hybrid vigor.

With this fact in mind, we are underweight Europe, and the USA, and overweight Asia. The relativity of that will change over time, but this is how I see the world today.

In this rebalance, it is important to share the long-term big picture as the Asian region is very sensitive to the unfolding energy shock. We need to be mindful of this in the selection of stocks to ride out this period of volatility.

The updated portfolios will be out over the weekend.

We have at least ten days on our hands before the troops arrive.