Gold in the Hand versus Gold in the Ground

Relative value trading changes the perspective on the impact of near-term production problems if you have large in ground resources to produce in the future.

The markets are moving off a Donald J. Trump tweet again.

It does not matter what it was. There will be a new one soon enough.

Let us blank out the Trumpian Dog Trumpet and think about price versus value.

Our challenge, whether we like it, want it, or need it, is to survive this mess.

The Theory of Financial Relativity is my chosen path.

This is a learn by doing newsletter.

Let’s do it!

What is price?

Superficially, this is a really stupid question.

The price of bananas is how much cash you hand over for them at Woolworths.

Of course, the time of year matters, the choice of currency, and a whole bunch, pardon the pun, of other matters. The price of bananas changes a lot.

If you measure the price of Banana in Bitcoin, two crypto, you get this.

Some lucky crypto-monkey got out of Banana on the spike.

Otherwise, it is a living Hell for those still holding Banana!

While it is easy to forget, the price of something is always an exchange value.

The Micronesian Island of Yap has money based on rocks with holes in them.

The exchange rate and values are determined by the cost of labor.

The issue was that Yap had no durable rock or precious metals with which to make coins. Instead, experienced Yapese sailors, commissioned mostly by wealthy high chiefs, would sail to Palau on bamboo rafts, and eventually, schooners, to load up with limestone from their quarries. - BBC on Rai Stone from Yap

Obviously, large heavy stones are more valuable than light ones.

They remain valuable even when the canoe sank and they are on the lagoon bottom.

Obviously, it would take some labor to get them from the sea floor to the shore.

The point I am making is that money is a proxy for effort.

If I want you to do something for me, I must pay you.

Price is an exchange ratio, and money is a convenient way to negotiate exchange.

I give you $0.81 Aussie Pesos.

Mr Woolworths Cavendish Banana Man, you give me one banana!

What is value?

If you were to shop around for bananas, you may find an agreeable deal, where the banana is good, but the price is better. You can get more for the same money.

In the same good, this is easy, especially if it is standardized.

Aside from shipping and storage costs a 99.99 fine gold bar should cost the same, but there will be differences due to inventory effects. It takes time to resolve imbalances between local demand and supply, and so the price changes.

Time is money, as they say, and financing inventory across any span of time, will cost money, representing the opportunity cost between selling today versus tomorrow.

Since prices are fluctuating all the time, including the cost of borrowing and lending money, there can be periods of value versus price. If you are prepared to be patient, value will often appear in a financial market, when securities are cheap in price.

Obviously, this happens between securities and cash, which is thought of as stable.

Cash is stable, within a single monetary system.

One Aussie Peso today is worth the same as another today, always.

However, the purchasing power of an Aussie Peso for a US Greenback changes all the time. That of both changes for their future cousins, being cash on deposit.

Recognizing that the unit of account is not the same as a yardstick of value is critical whenever relative prices are changing rapidly.

If I went from cash to oil, then to gold, and then back to cash, I have a circuit. This could leave me with more or less cash in the future. This is the key to trading.

What is the right discount rate?

The way we deal with this in finance is to compare the exchange value of a future cash amount, that may be the result of trade, with that we would earn passively via interest. This is an obvious equation for durable commodities that earn no interest. Gold today will still be gold tomorrow, if I leave it under the bed. This is not true of the cash in my broker account. That will be larger due to the earnings from accrued interest.

When other things are held equal, it would make sense to put cash on deposit, versus buying gold today, provided the price of gold was not higher tomorrow.

There is a lot written on Wall Street about how higher interest rates are bad for gold. This may be so in the time it takes an investment bank to call their clients and advise them to sell their gold. Once they have done that, we see what happens.

For five years gold, which makes no interest, has beaten US Treasury 10-to-20-year bonds with income reinvested, as measured by the AMEX: TLH/AMEX: GLD spread.

This can seem very counterintuitive, at first, but is due to a changing estimate of the future inflation environment in the USA. This form of relative value ratio has a key role in finance through the technique of discounting. When we divide the price of one security by another, and account for income, we are showing a through time comparison of value across time. This is what we care about, looking forward.

Buying bonds, via TLH, and then switching to cash, versus buying gold, via GLD, and then switching to cash would have left you with 67.21% less cash. It mattered.

What did cash do over that time?

A brokerage account deposit is typically in a short-term money market fund, which is proxied by US 3 Month Government Bonds, which bear 90-day interest.

Presently, the 3M Treasury Yield sits at about 3.72% and looks set to rise again. Note that gold has appreciated versus bonds since 2022, and the very recent drop.

The driver of this behavior is rising inflation expectations.

This is clear in the total nominal return chart for bonds.

Over that five-year period, the TLH lost -16.49% in nominal terms. That comparison is made worse in real terms due to the eroding effects of inflation.

Over the same period, non-interest bearing gold, in a rising interest rate, because of rising inflation expectations regime, appreciated +154.69% in nominal terms.

The reasons for this gold bull market have been discussed elsewhere. For me, the big one is central bank buying, as a hedge against sovereign risk holding US Treasuries, combined with an increasingly volatile geopolitical situation.

We are in uncharted territory now, but I remain focused on comparing the relative value over time between different securities. Discounting one choice by the other, accounting for income, in a common currency, offsets monetary effects.

It is the only way I know of to analyze markets without the confounding noise from investor sentiment, which skews each price wildly compared with cash whenever a market panics. On those days, all correlations go to one. It is pure noise.

Gold in the Hand versus Gold in the Ground

Let us now apply this thinking to an important recurring decision.

Which is better to own? Gold or Gold miners?

There are times when I have owned neither. There are other times when I have been very titled towards one over the other. The driver is the relative value chart.

The other thing to point out is the difference between gold in the hand, gold in the ground, and gold that might be in the ground. This is the difference between gold bullion, major gold producers, and gold developers and explorers.

Gold in the Hand is gold bullion or an ETF like AMEX: GLD

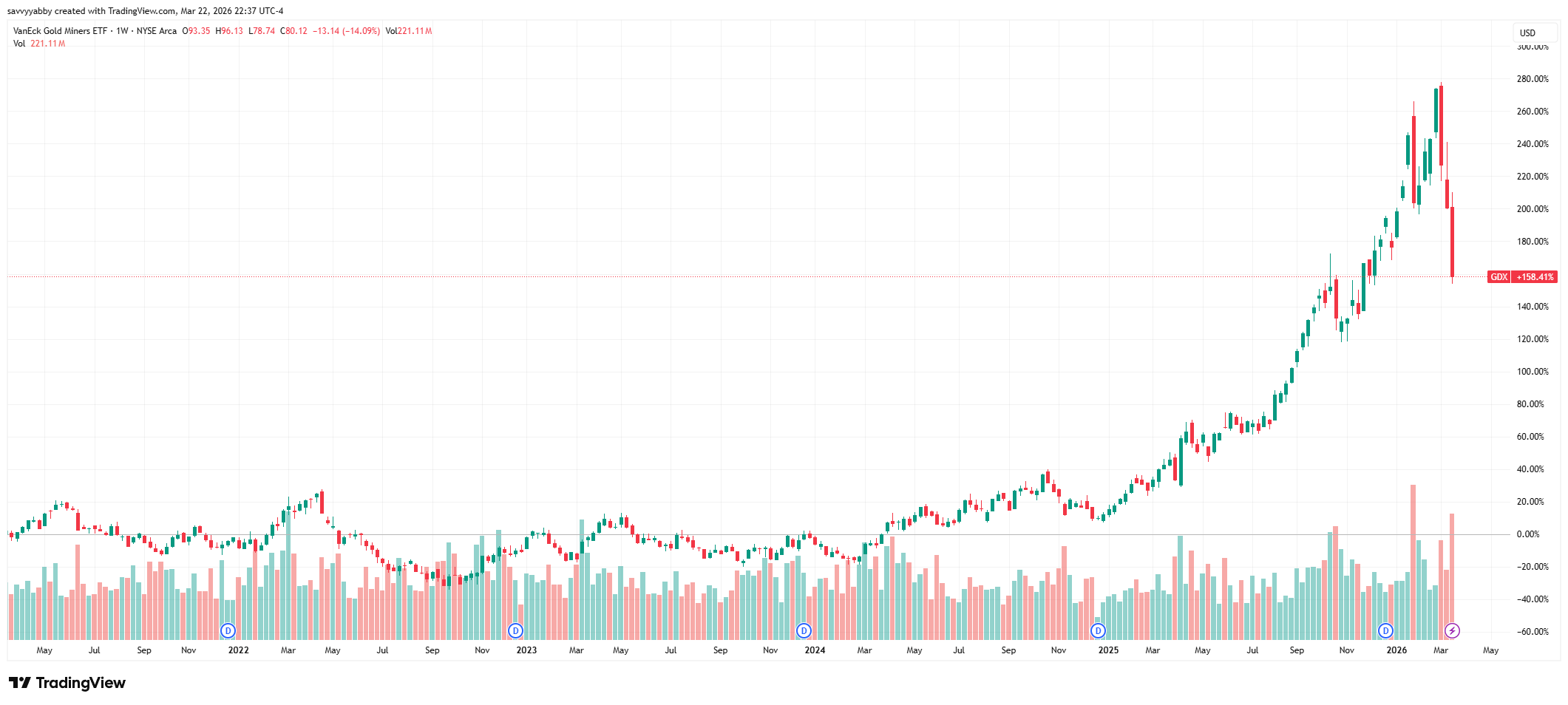

Gold in the Ground is major gold producers like AMEX: GDX ETF

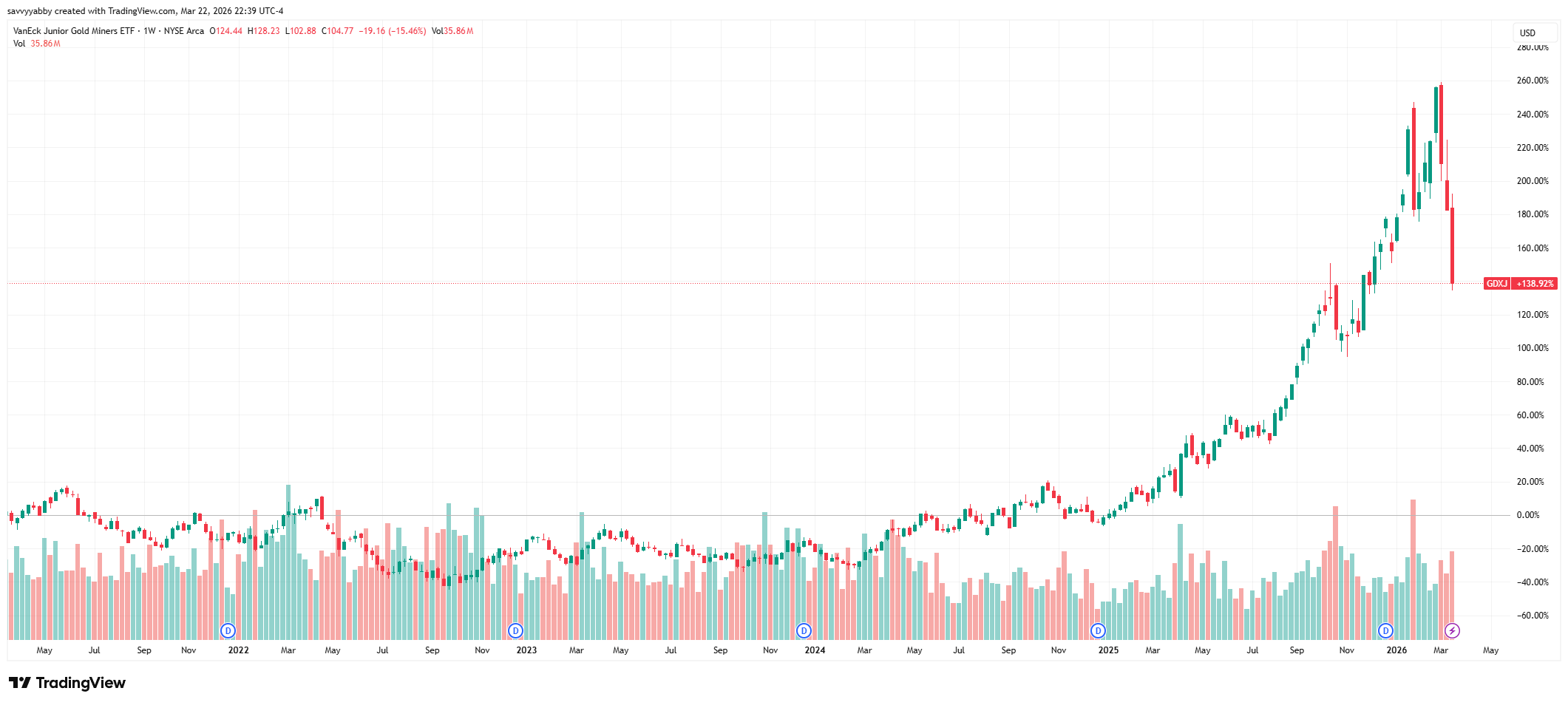

Gold in the Mind is gold juniors like AMEX: GDXJ ETF

Here is the Gold in the Hand total return chart.

Here is the Gold in the Ground total return chart.

Here is the Gold in the Mind total return chart.

Notice that Gold in the Hand has done about as well as Gold in the Ground.

Gold in the Mind is the smaller capitalization juniors that have a higher sensitivity to market sentiment and are therefore off more than the producing majors.

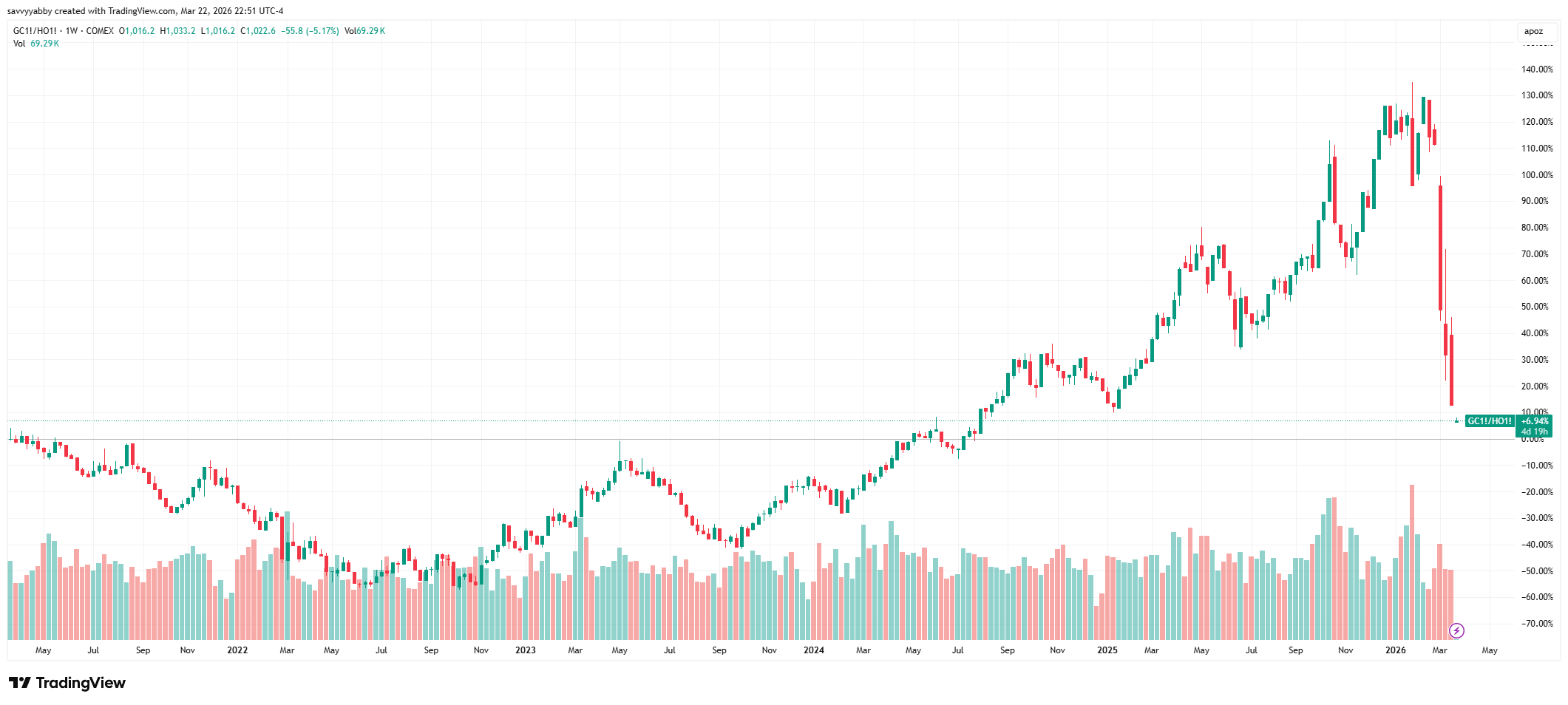

Now let us proxy the costs of gold mining with diesel NYMEX: HO.

The relevant spread is COMEX: GC/NYMEX: HO, measuring the relative purchasing power of gold, the product of gold mining, with diesel, the labor for mining.

Of course, the local human labor costs will also go up, but the price structure of food and minerals production is closely tied to the cost of diesel, explosives and chemical reagents. The feedstocks originate from the petrochemicals complex.

Donald J. Trump looks set to blow up those costs with his war of choice.

Reasoning this way, it is not hard to see why gold miners have taken it in the neck in recent trading sessions. However, higher costs mean the production frontier shrinks.

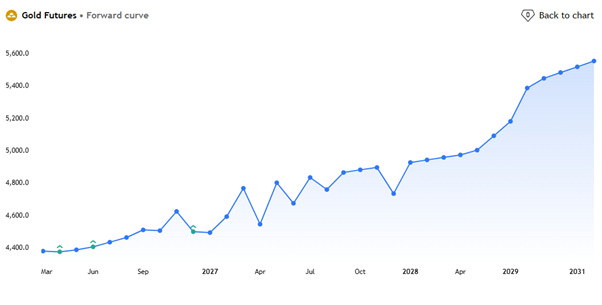

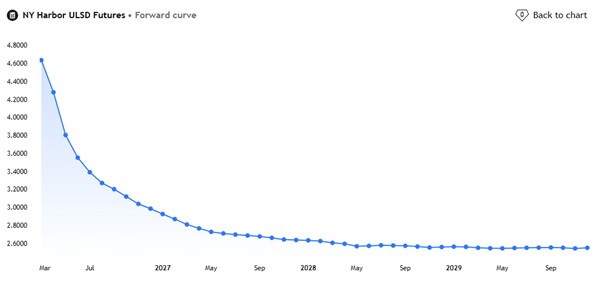

The forward strip of gold price for future delivery is still rising into 2031. The market is pricing contango, meaning adequate near-term supply, and higher future prices to account for storage and shipping costs. This has not changed, except for the level.

The opposite condition of backwardation applies to Heating Oil (Diesel), showing that the market views this supply disruption as acute but not permanent.

These dynamics are consistent with near term higher costs for gold producers, that will negatively impact their cost structure, but not on a permanent basis.

We should expect gold producers to reprice downwards when measured in gold.

To see this let us compare Gold in the Ground versus Gold in the Hand.

Notice that for the first four years of this five-year period gold was doing better than the miners, and that it reversed around the start of 2025 when equity investors began looking for more leverage to future gold prices through the mining sector.

The same is true for Gold in the Mind versus Gold in the Hand.

I would expect this retreat to continue until gold stabilizes and the cost position of the gold producers becomes clearer. However, in my piece Best Global Idea: ASX Gold Stocks, from April-2025, I called attention to the central bank buying trend. This war in the Middle East has only confirmed the suspicion of many that US Treasuries were fraught as a store of value. They are a geopolitical tool of coercion.

The USA now has to fund a ballooning budget deficit with new issuance to finance an ever-expanding war of choice whose aims seem to be a moveable feast.

There is no doubt that the US Military can wreak enormous damage on Iran but at the cost of its international reputation in global affairs.

The world required no persuasion that the US Military is powerful.

We knew that already.

The persuasion required is one of commonsense in knowing when to stop.

Iran will keep on fighting because it is a sovereign nation subjected to attacks on its own people, assets, and territory, with no warning, during active negotiations.

It is going to be difficult for any nation to trust what the USA says and will do.

This elementary point, and the connection between it and the purchasing power, of the US dollar, which only the USA has the power to print, seems lost in the noise.

This war can only accelerate the move towards dedollarization.

In our view, the fundamental reasons for this bull market, namely better financial return, and security to holding gold over US bonds, have not changed.

There is a great deal of market volatility to navigate in coming sessions, with the likely move upwards in US bond yields, bringing the spread gold vs. bonds into sharp focus. I wrote The Market Schwerpunkt (Gold vs. Bonds), three weeks before the first attack by Israel and the USA on Iran. I think that story is only made sharper now.

We cannot predict the outcome, but we do know what to watch.

The way to action this is to look for relative value trades between:

Gold in the Hand

Gold in the Ground

Gold in the Mind

I will look at a single stock examples below, but it is important to first look at Gold in the Ground versus Gold in the Mind. I expect the juniors to get whacked more.

Generally speaking, smaller capitalization stocks are more susceptible to major selloffs than the larger capitalization stocks. The above chart suggests there is more of that to come as investors get more nervous about the continuation of this gold bull.

An in illustrative single stock idea is shown below