USA Rebalance for End March 2026

Starting this month, we schedule rebalances for month-end and notify early. Boeing looks like a good play now given the run of damage and the likely widening of the war.

The Savvy Yabby Report distributes our institutional grade model portfolios to paying subscribers on a monthly basis. The current list includes these strategies.

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

The existing research notes and newsletter offer remains, but you will see some tighter integration between what we write there and the model portfolios.

The licensing and complaints procedure is outlined in our Financial Services Guide.

These portfolios follow the Jevons Global investment process.

1.19MB ∙ PDF file

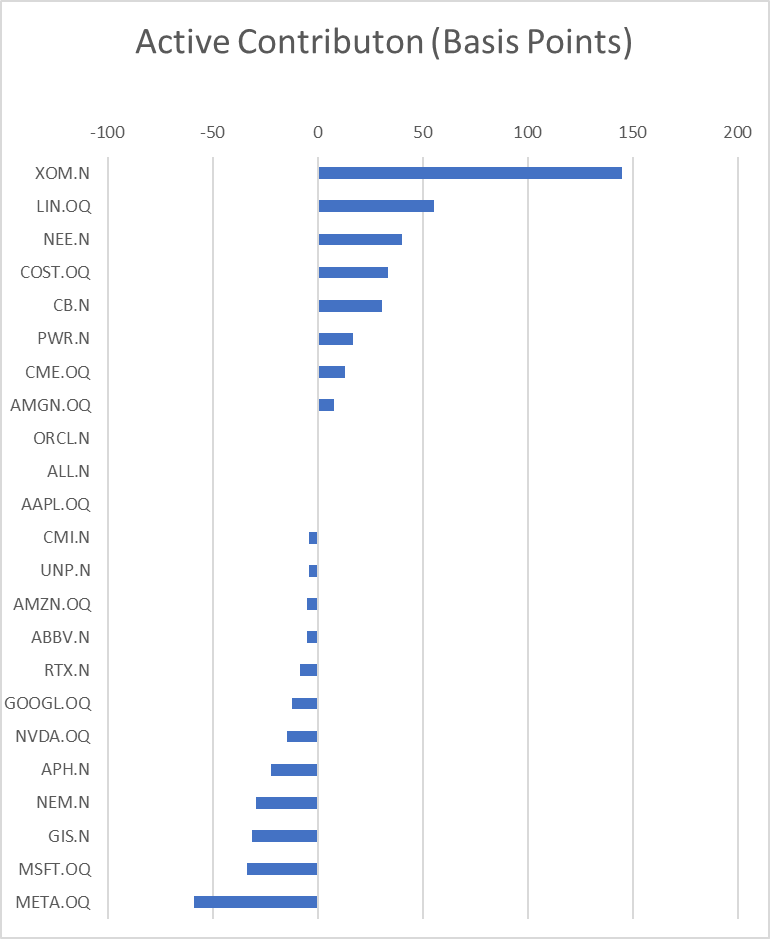

The last change to the model portfolio was effective at close 5-Mar-2026.

We exited Apple XNAS: AAPL, Oracle XNAS: ORCL, and Allstate XNYSE: ALL to hedge a possible energy crisis due to the US-Israel war on Iran. The new positions we added were oil major Exxon XNYS: XOM, industrial gas giant Linde XNAS: LIN, and insurer XNYSE: Chubb Inc. This on the outlook of rising interest rates and energy prices.

The investment thesis of a protracted war in the Middle East is playing out. While the gold sector and gold miners were initially weak, we think that was the first wave of selling to raise USD in affected central banks defending their currencies.

Our prospective outlook is that the USD will initially strengthen, on the natural view that the USA is less affected by an energy crisis. However, the pressure of war finance is likely to lead to further upward pressure on US interest rates, and globally.

In the near term, we are raising US asset exposure in our global model portfolios from 50% towards 60% by shedding more consumer-oriented names and energy exposed economies across Asia and Europe.

However, we think the US safe haven will prove temporary once bonds weaken.

The economies most affected by this war are those outside of the USA which are heavy importers of oil, like India, China and much of Asia.

There is also a problem with lost oil revenues impacting Persian Gulf states.

In the near term, that puts downward pressure on liquid precious metals. In the longer term it places acute risk on the US Treasury Bond market from foreign selling.

None of this is baked in, but it seems more likely now.

The updates for close-of-trade 31-Mar-2026 are below the paywall.

Thematic Positioning

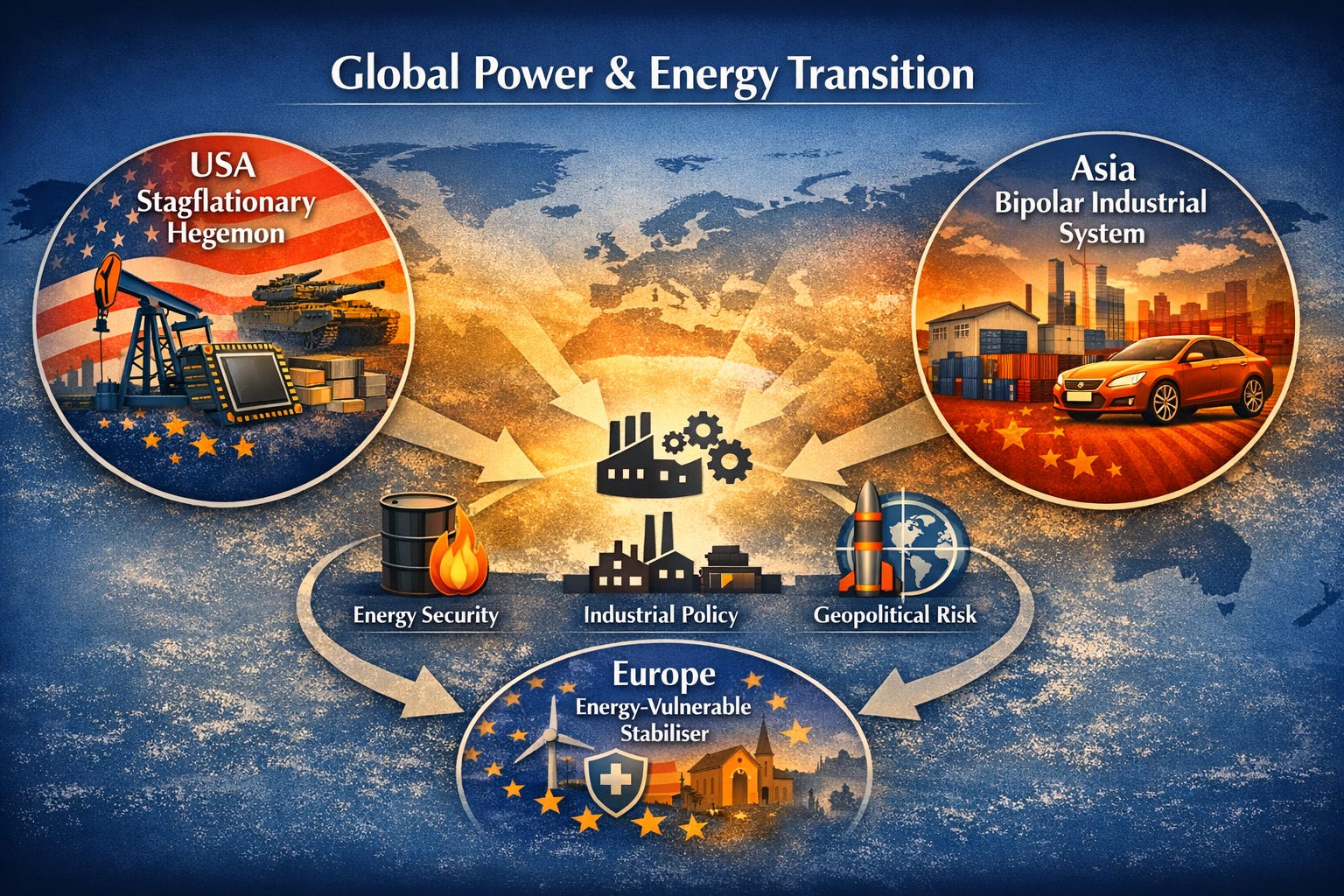

Our big picture revolves around the Global Power and Energy Transition. We have described this here, and here. The short version is that we see a tug-of-war between relative price-stability in Asia, driven by Japanese reflation and Chinese deflation.

This dynamic, and the security rivalry between China and Japan in their own backyard creates a recipe for trade detente and stability, since both nations benefit from rising global demand for their goods and services in the developing world. Europe is stable and low growth, but insecure over Russian intentions, and US hectoring.

The USA is running a new race for hegemonic global dominance. This may work, and we should not discount that possibility, but there is an acute risk of overreach. While the United States is the largest global economy, and very dynamic, it seems intent on playing to military strength and a weaponized financial market to secure its aims.

If this gambit should go awry, then a stagflationary slump is possible.

Earlier we displayed the S&P 500 Index, valued in ounces of gold.

This single chart should serve to remind us of the risks attending each downswing.

The US markets are not cheap, by historical standards. If the US Treasury Bond market were to sell off further, and the 10-year note reached the 5-6% range, a US recession is quite possible. With energy prices rising, this would portend a global recession.