USA Twenty Stock Portfolio: Feb 2026 Strategic Move to a Stagflation Barbell

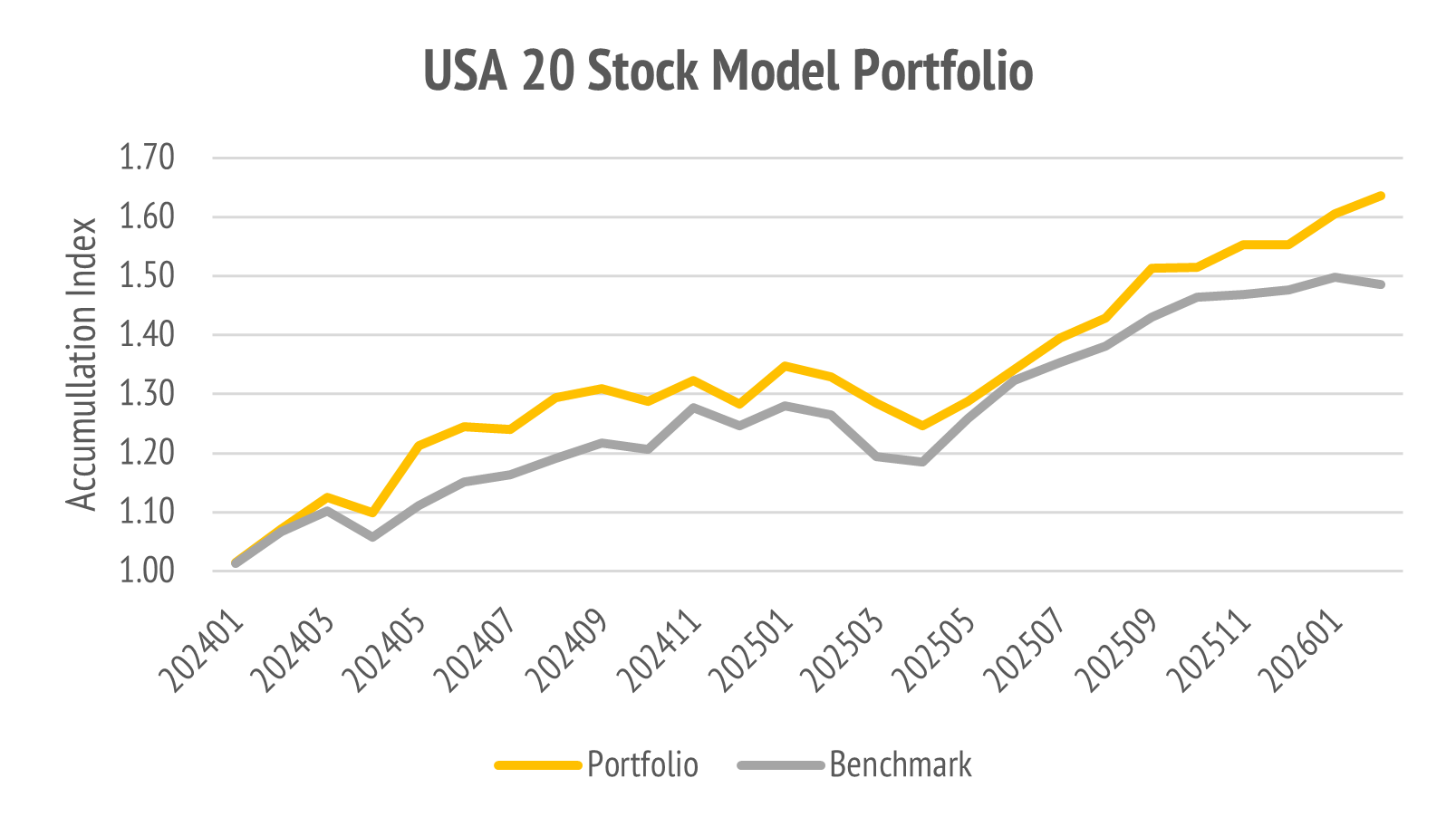

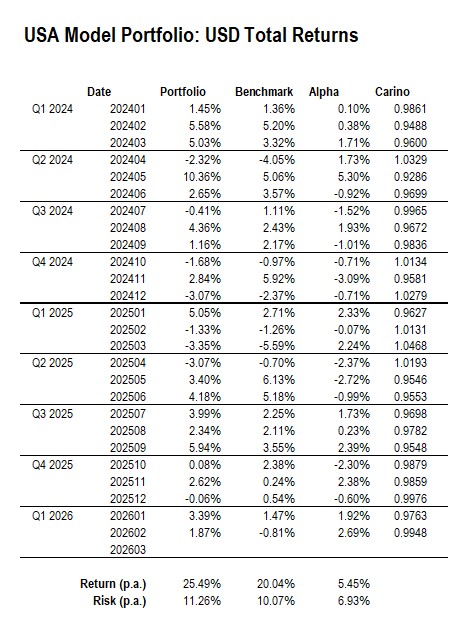

February continued our run of positive performance. The US 20 Model was up 1.87% while the S&P 500 was down -0.81% for a +2.69% Alpha. YTD our alpha is +4.68%

Stagflation Risk is Rising

With the unexpected ferocity of the US-Israel vs. Iran war in the Middle East, we are making a strategic move to hedge stagflation risk. For those who were not alive in the 1970s this may seem like a brave or foolhardy call.

Not to me.

I first sounded the warning back in May-2024, three months after gold first broke out to the upside and I turned bullish on the yellow metal.

I wrote on the gold bull market to come on 8-Jan-2024 for the Market Online.

There I recalled the Wizard of Id comic strip:

Remember the Golden Rule! Whoever has the gold makes the rules.

These conditions define for us a century scale investment theme:

We are now living through a major Global Power and Energy Transition.

The energy bit is obvious. The world is moving from fossil fuel powered combustion engines towards a future of ubiquitous electrification.

This supports themes like battery minerals and copper.

The power bit is less obvious. The world is moving from a global political and financial system ruled by the West to a more diverse multi-polar world.

Emerging economies are growing stronger.

The counter to this has been an “America First” geopolitical strategy.

We saw the tariff measures first. Now we see the sharp end of US military power.

This is total war, as evidenced by the US Navy electing to sink an Iranian frigate in international waters that was not in the theater of war.

If you a fan of propaganda, you might presume that this is the natural order in war. However, it is not proportionate, and a state of war remains undeclared.

This latest US action is demonstrative and signals the return to gunboat diplomacy.

There is no other plausible explanation for taking such extreme action.

You do not sink every ship on the high seas that belongs to a sovereign nation that you chose to attack, by surprise, in a war of choice, without ever declaring war.

There are precedents for such actions but none of them are good ones.

We must now assume that the US Department of War is at war.

Due to the global reach of this conflict, and US intent to widen it, there can be no doubt that this will be a long war, and that it will soon drag in the Europeans.

The Significance of the Strait of Hormuz

In the Market Schwerpunkt, I wrote about the Elbridge Colby Strategy of Denial in the context of blockades to trade, such as we now see playing out in the Gulf war. There we see how denial is used by Iran to punish its Gulf neighbors for assisting the war.

This active blockade will have secondary effects on all nations that depend on oil and gas that passes through the Strait of Hormuz, including India and China.

Australia adopted the strategic principles laid down by Elbridge Colby in the 2024 National Defence Strategy. The object is to maintain a favorable regional strategic balance by preventing any power from coercing others through force, particularly within the Indo-Pacific region.

That is all well and good, except that the source of coercion is not China!

The USA coerced the United Kingdom to allow the use of its airbases to facilitate the present war against Iran. The European allies, in NATO, are now pressured to follow.

It is entirely possible, that NATO will be mobilized, by such coercion, to prosecute this war of choice, in the Middle East, or suffer tariff and other punishments.

Paradoxically, the Colby Strategy was sold to Australia as a means to deter coercion.

I guess coercion is bad when it does not come from the USA!

I am no naive young fool intending to mimeograph pamphlets for the International Socialist down behind the old ANU Refectory. Nor was I ever in that camp.

I am an investor and a geopolitical realist.

Whatever may be said by US ally Benjamin Netanyahu, speaking for the State of Israel, it makes little sense to me that the USA would indulge this war with no objective.

The stated objective concerns Iran, but I view it as Act One in The Play of Denial. The real objective is to control oil trade as a coercive lever.

There will be strident denials of this motive.

I know that.

However, the task of a good intelligence analyst is to look behind the obvious efforts to shape the global information space and discern the wider plan in play.

Earlier this year, President Trump dropped the bombshell that he would seek a 50% rise in the Pentagon budget for 2027. That is a huge increase in peacetime.

Whether declared, or otherwise, the US Department of War is now in a war.

This could easily turn into a wider war because the Strait of Hormuz is blocked.

The poor analyst would note:

“Well, that is the fault of Iran.”

Indeed, it is Iran that is denying passage to ships through the Strait of Hormuz.

However, that was entirely predictable and telegraphed action in the event of war.

Why then did the USA proceed with the attack?

There are many possible reasons, most of which I discount as lacking credibility.

It has been commented by many that U.S. Intelligence assessments had discounted the possibility that Iran was actively trying to make a bomb.

Nobody doubts they had nuclear enrichment facilities, but these were bombed, and allegedly destroyed, to great fanfare in Operation Midnight Hammer.

Operation Epic Fury had Supreme Leader Ali Khamanei as the first target.

That individual was assassinated.

Khamanei was the Iranian leader who issued a fatwa against nuclear weapons.

The official story from the USA and Israel is murky at best and not proportionate.

“When you have eliminated the impossible, whatever remains, however improbable, must be the truth.”. - Sherlock Holmes

The above line from Sherlock Holmes offers an invitation to further contemplation.

Why undertake such a risky open-ended war of choice with no clear objective?

The answer surely lies in the hidden objectives which comport with the data.

We can only guess at such objectives and so must use plausible reasoning.

Ever since the time of the 1979 Islamic Revolution, the threat, from Iran, to close down all oil and gas traffic out of the Gulf has been on the table.

In earlier times, this served as a useful coercive deterrent to Western action aimed at the fall of the Iranian regime. The USA is now self-sufficient in oil and gas.

The USA is now a big exporter of oil and gas.

Deliberate US action, in Venezuela, has given the USA control of those reserves.

Actions, by forces unknown, to destroy the Nordstream pipeline, plus sanctions against Russian oil and gas have made Europe dependent on the Gulf and USA.

With Qatari gas offline, which is 20% of global supply, Europe will be desperate.

Much of Asia, including India, China and Japan, derive oil and gas supplies on the Middle East. The Iranian action will hurt the global non-US economy.

Since the cessation of hostilities is in the hands of the USA and Israel, other nations are now under the gun to help destroy the Iranian regime.

The US-Israel-Iran war will widen, and US coercive power is established.

This is a plausible motive for the USA to assume this war risk.

The energy supply risk is a lever on other states to line up behind the USA.

China is not such a state, and so will pay close attention to this display of power.

What is happening now is the Colby Doctrine to a “T”.

There is the public smokescreen to manufacture consent.

Then there is the active geopolitical strategy.

Stagflation Barbell

Perhaps it is in the blood to not wait for the sirens to take cover.

I am a contrarian investor. I have no need for the comfort of the crowd.

I exit before the theatre burns down and aim not be trampled in the rush.

The markets seem sanguine about all of this because they focus on current visibility.

Portfolios need not impound certainty but lend themselves to scenarios.

Below the paywall line, I lay out our remodeled portfolio.

This impounds a stagflation barbell, that has the bulk of capital in steady as she goes growth trends, some natural defensives, a minimum of interest rate sensitives, and a hard core of real asset exposure, and inflation pass-through businesses.

The turnover this month is high at 24% of the book.

I think that is warranted.

Model Portfolio Offering

The Savvy Yabby Report distributes our institutional grade model portfolios to paying subscribers on a monthly basis. The current list includes these strategies.

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

The existing research notes and newsletter offer remains, but you will see some tighter integration between what we write there and the model portfolios.

Regulatory Disclosures

This service is owned and operated by Jevons Global Pty Ltd.

The licensing and complaints procedure is outlined in our Financial Services Guide.

For legal reasons, I need to include this informational disclosure.

These portfolios follow the Jevons Global investment process.

The last change to the model portfolio was effective at close 8-Dec-2025.

These changes were described in our note USA 20 Stock Model Portfolio.

NB: Past performance is no guide to future results.

Model portfolios are not audited and are only approximate guides to real results.

Performance Summary for Feb-2026

The year opened positively for the benchmark S&P 500. Through the month the total return of the index was 1.47%. The return for the model was 3.39%, which was 1.92% ahead of the benchmark. These are total returns in USD.

Overall, the model performance since inception has been excellent.

The strategy has now posted two consecutive years of +5% alpha. The risk has been anomalously low in recent years. We expect that to rise going forward.

Key Contributors

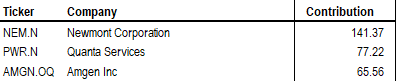

The top three positive contributors to performance in Feb-2026 were:

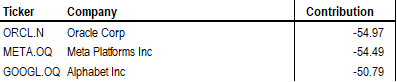

The top three negative contributors to performance in Jan-2026 were:

Notice that our gold exposure, via Newmont NEM, did very well in February, despite the late correction to gold and gold stocks in January. Year to date, Newmont is the top contributor, having added 232 bps of 468 bps total.

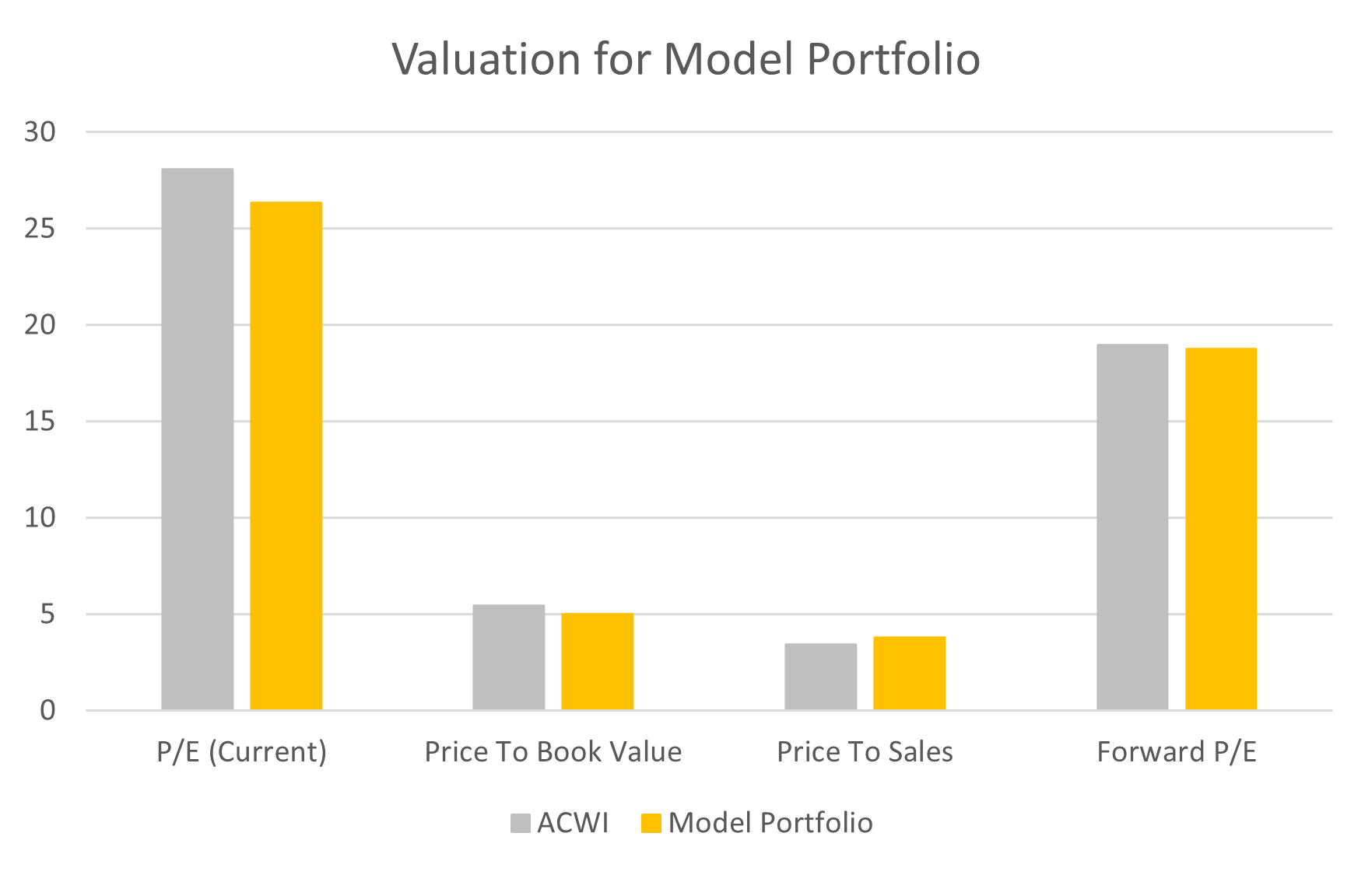

Portfolio Valuation Metrics

The portfolio valuation is significantly cheaper than the market.

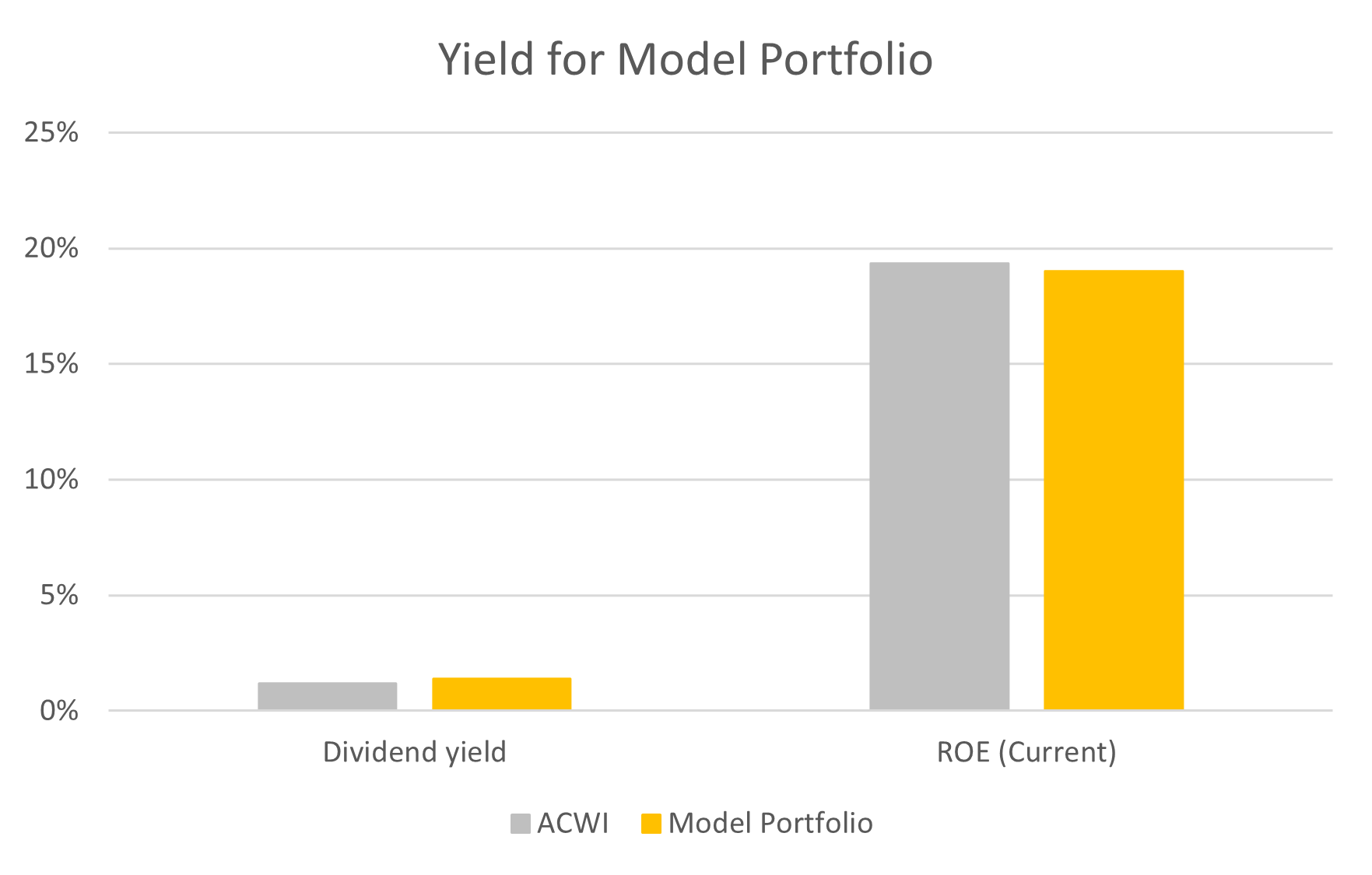

The dividend yield and Return on Equity (ROE) are in line with the market.

The sector positioning is more overweight resources, and underweight digital technology, but remains well diversified across the other sectors.

The big tilt in this rebalance is evident in the resources and energy sector. The shifts are not blind bets on all commodities, as we explain in the stock selection below.