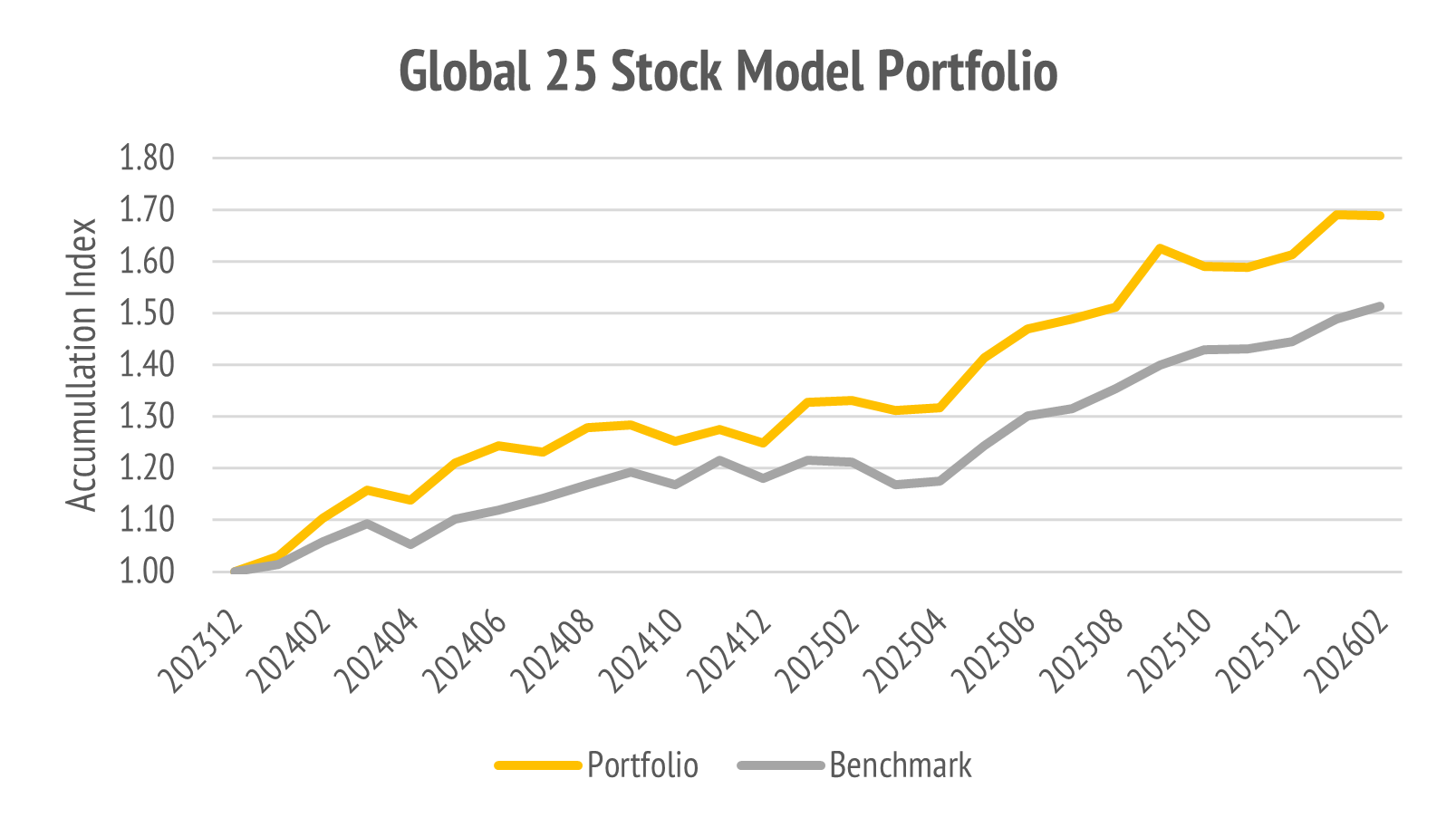

Global Twenty-Five Stock Portfolio: Feb 2026

The month was flat with a return of -0.04% versus the benchmark 1.64% for a negative alpha of -1.68%. The result was driven by corrections in technology and pharma.

US Stagflation Barbell Changes

The present markets are highly volatile, with the onset of the US-Israel war on Iran. The prior month did not span this period, and so this report does not cover any of the market action since. For major changes see the USA Twenty Stock Portfolio: Feb 2026 Strategic Move to a Stagflation Barbell. We made no changes in the International Twenty Stock Portfolio: Feb 2026 Global Power and Energy Transition.

For further detailed discussion of our strategy read those prior reports.

For a succinct summary, note the following point.

International markets ex-USA are largely being driven by the oil price factor.

This makes sense since the USA is the largest oil producer globally and is in the driving seat for this war. The pain of this war will not be equally shared.

Our major changes this month were to add natural gas and oil to the portfolio in the Australia Model, via Woodside Energy XASX: WDS, and in the US Model, via Exxon Mobil XNYS: XOM. There were other changes also that are listed below.

The positioning reflects the view that there is now elevated stagflation risk. The effects of this are somewhat asymmetric, and mostly dependent on oil intensity.

Europe could well experience a major slump, but we are underweighted anyway.

Japan imports much of its oil, and is at risk, but most of our exposure is in defense, banks and trading houses that are long copper. Once the dust settles, it will make sense to think further on our positions in Japan, but it looks okay for now.

China is the wild card, but our major exposures are electric vehicle stocks, that may well benefit from pressure on oil supplies. There are other exposures in Taiwan, to semiconductor equipment firm Taiwan Semiconductor XNYS: TSM.

Overall, I think it makes sense at this time, to make a positive bet on stocks we think can do well in the USA, given the extent to which this war elevates the importance of oil and defense. Implicitly, the first trading days of this month have been a negative bet, by the market, on everything else. This is not sustainable, for global economic growth. That provides some check on US war aims.

Paradoxically, this period discloses the limits of dominant military power.

Indeed, the US, along with its ally Israel, can cause a lot of destruction in Iran. On the surface, this looks like the ticket to dictate terms to all and sundry.

The problem with this war is at what cost do you continue.

The Iranian threat to send oil to $250 USD per barrel is not crazy when it moved to $120 USD per barrel in one trading session. This standoff is a ticking time bomb.

The belligerents seem destined to go on fighting, and we see a long conflict ahead, but neither side can afford to push the limits of global tolerance.

There is a real limit to what other nations will tolerate, and we are close to it. I do not simply mean Iran, as the proximate cause of the war was a surprise attack, and some dubious justification that does not pass muster outside the USA, as a legal war.

In some circles, this does not matter.

In the real world it does.

The Terminal High-Altitude Area Defense (THAAD) is an integrated ballistic missile defense system, which is considered vital to maintain the air defenses against the larger Iranian ballistic missiles. Several have been reported destroyed.

With the reported rate of Iranian missile firings reduced, and the US, Israel, and Gulf states that have been the subject of Iranian attacks, running low on interceptors, the pace of war may shift. The USA is more likely to rely on conventional gravity bombs, and less on missiles. Iran will likely modulate its own war effort for sustainment.

In simple terms, we expect a prolonged conflict, with oil in the range $80 to $90 USD versus the Armageddon scenario of $150 USD per barrel. In real terms, these prices are lower than they were in the period 2011-2014.

It may seem crazy to suggest an oil detente brokered by Donald Trump and Vladimir Putin, but that interpretation does fit the visible data.

This South China Morning Post report describes the background.

Does this mean an end to the Iran war?

Not likely.

It just means that how the USA and Israel go about the war will be modulated to a tempo and target list that leaves oil prices elevated but manageable.

How is this possible?

I am no diplomat, or military strategist, but I imagine Trump made a deal:

How about I temporarily lift oil sanctions on Russia to free up the market and you do not provide the latitude and longitude of remaining THAAD radars to Iran? Quid pro quo. I hold the leash on Israel. You hold the leash on Iran.

The war will go on but will have “finished” somehow.

The bombs will drop but the oil price will not rise.

This is what Balance of Power politics looks like.

It sounds nuts but let us see what happens.

Model Portfolios

The Savvy Yabby Report distributes our institutional grade model portfolios to paying subscribers on a monthly basis. The current list includes these strategies.

Australian 20 Stock Model Portfolio

USA 20 Stock Model Portfolio

International (non-USA) 20 Stock Model Portfolio

Global Best Ideas 25 Stock Model Portfolio

The existing research notes and newsletter offer remains, but you will see some tighter integration between what we write there and the model portfolios.

Regulatory Disclosures

This service is owned and operated by Jevons Global Pty Ltd.

The licensing and complaints procedure is outlined in our Financial Services Guide.

For legal reasons, I need to include this informational disclosure.

These portfolios follow the Jevons Global investment process.

The last change to the model portfolio was effective at close 30-Jan-2026.

These changes were described in our note Global Model Portfolios.

NB: Past performance is no guide to future results.

Model portfolios are not audited and are only approximate guides to real results.

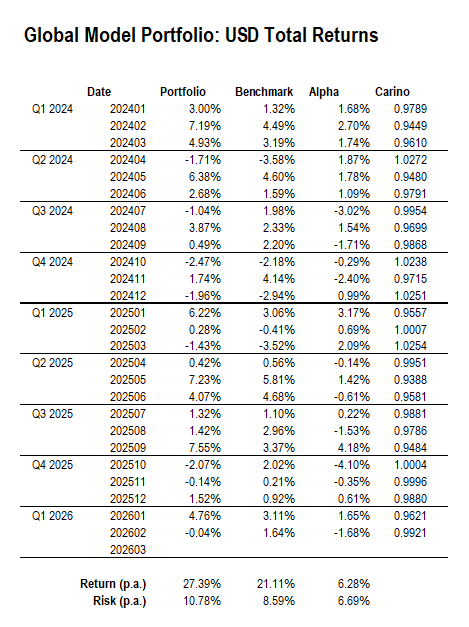

Performance Summary for Feb-2026

The month was positive for the FTSE Global All-Cap, which was up 1.64%, while the global portfolio was flat at -0.04%, for a negative alpha of -1.68%. This reversed the prior month positive alpha of +1.65%, so we are flattish on a year-to-date basis.

Overall, the model performance since inception has remained robust.

The month-on-month variability is not out of line with history.

Key Contributors

The top three positive contributors to performance in Feb-2026 were:

The top three negative contributors to performance in Feb-2026 were:

The drag was attributable to a retreat in technology and Novo Nordisk, the Danish pharmaceuticals firm that produces Ozempic. Competition with Ely Lilly, and the attempts by US Drug Regulator, the FDA, to cap pricing have hurt the outlook.

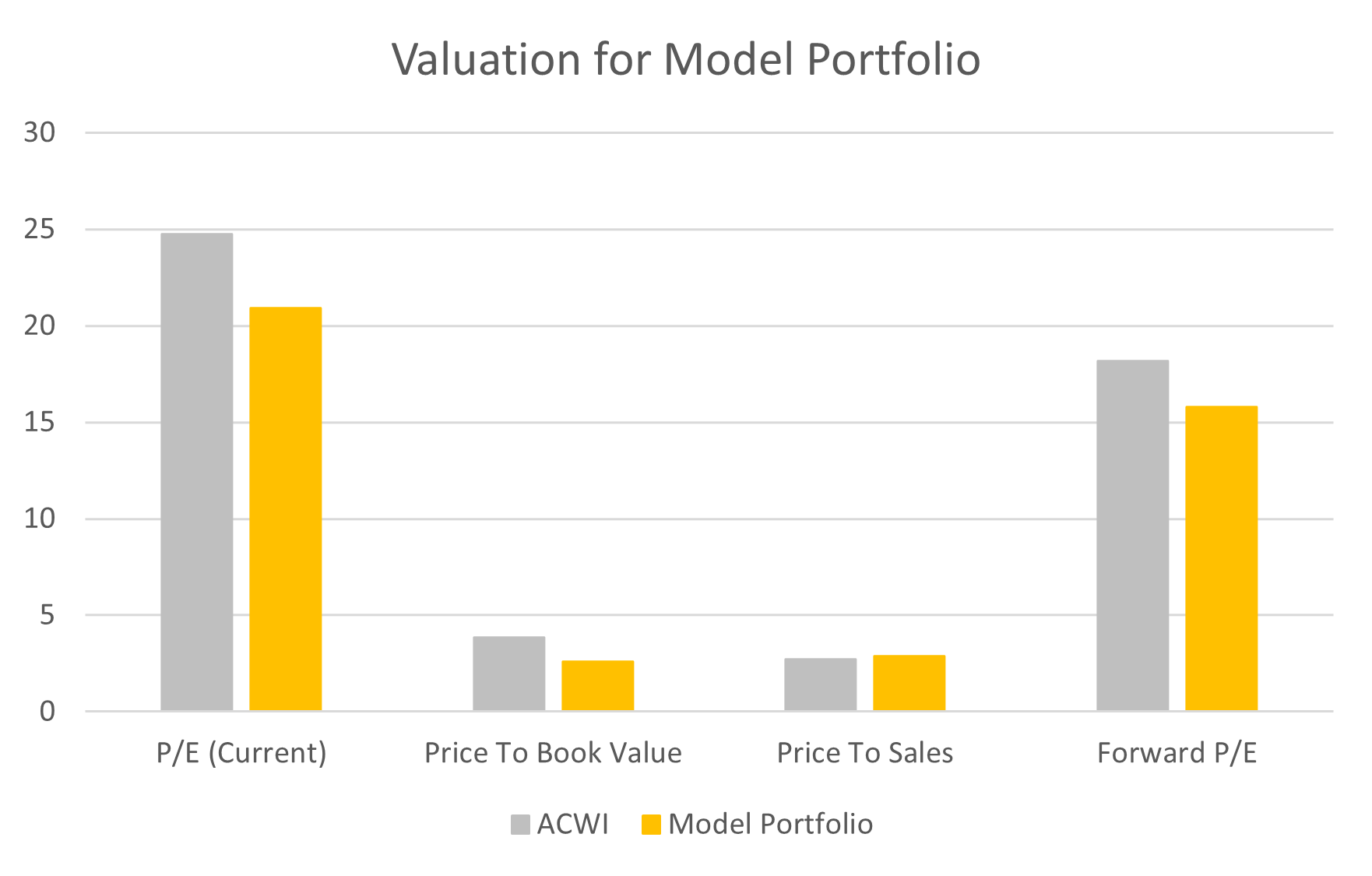

Portfolio Valuation Metrics

The portfolio valuation is cheaper than the market on both a trailing and forward Price-to-Earnings ratio basis, and also cheaper on book value.

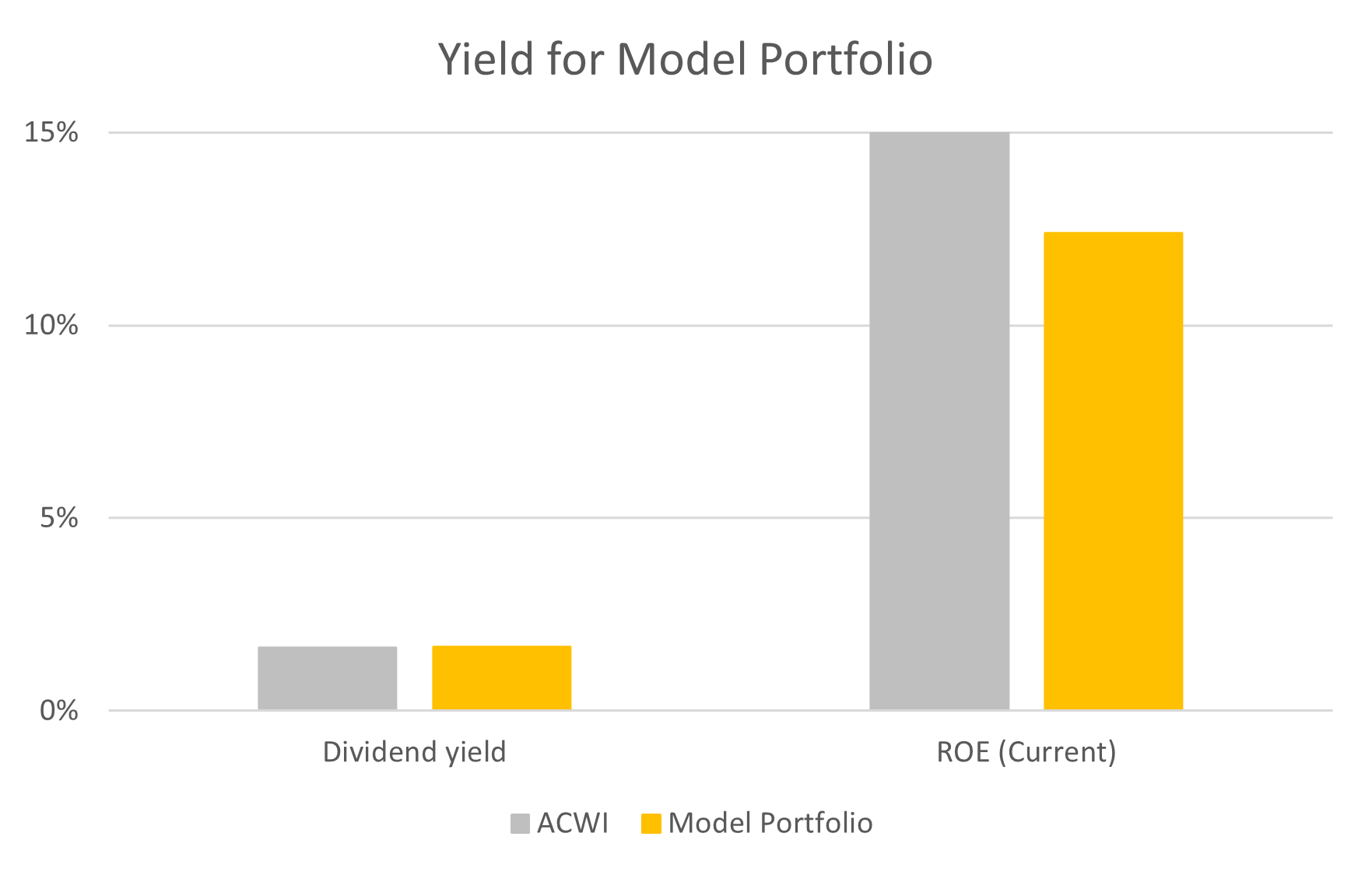

The dividend yield is in line with market and the Return on Equity (ROE) is lower.

The sector positioning is overweight resources, financial infrastructure, neutral digital technology, and underweight consumer needs, and consumer wants.

The regional weighting of the portfolio is skewed to Asia, via Japan and Hong Kong

The current weights for month-end are below, including recent US model changes.